#Robot Operating System Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile Tumblr US users spend an average of 4.04 minutes per session on the app.

Text

Robot Operating System Market Size, Share & Industry Trends Analysis Report by Robot Type (Articulated, SCARA, Cartesian, Collaborative, Autonomous Mobile, Parallel), Application (Pick & Place, Testing & Quality Inspection, Inventory Management), End User and Region - Global Forecast to 2028

0 notes

Text

[250 Pages Report] The robot Operating System market is valued at USD 581 million in 2023 and is projected to reach USD 1,082 million by 2028, growing at a CAGR of 13.2% from 2023 to 2028.

0 notes

Text

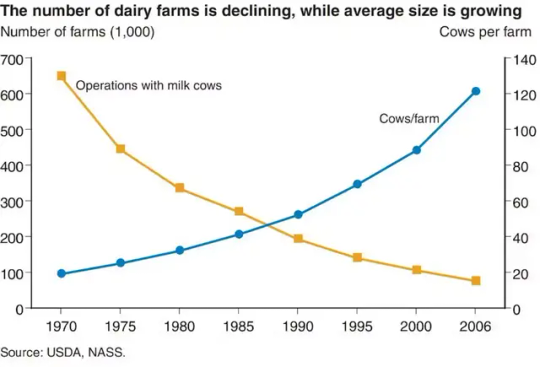

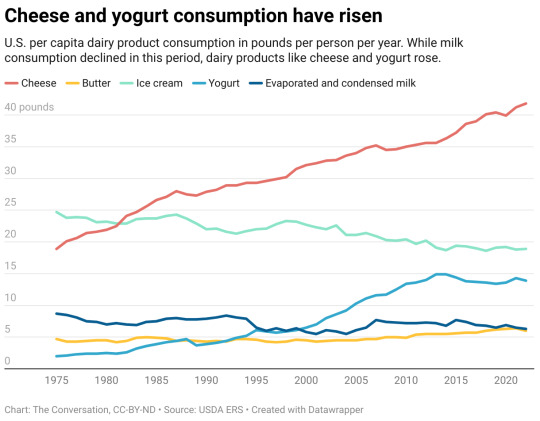

Milton Orr looked across the rolling hills in northeast Tennessee. “I remember when we had over 1,000 dairy farms in this county. Now we have less than 40,” Orr, an agriculture adviser for Greene County, Tennessee, told me with a tinge of sadness.

That was six years ago. Today, only 14 dairy farms remain in Greene County, and there are only 125 dairy farms in all of Tennessee. Across the country, the dairy industry is seeing the same trend: In 1970, more than 648,000 US dairy farms milked cattle. By 2022, only 24,470 dairy farms were in operation.

While the number of dairy farms has fallen, the average herd size—the number of cows per farm—has been rising. Today, more than 60 percent of all milk production occurs on farms with more than 2,500 cows.

This massive consolidation in dairy farming has an impact on rural communities. It also makes it more difficult for consumers to know where their food comes from and how it’s produced.

As a dairy specialist at the University of Tennessee, I’m constantly asked: Why are dairies going out of business? Well, like our friends’ Facebook relationship status, it’s complicated.

The Problem with Pricing

The biggest complication is how dairy farmers are paid for the products they produce.

In 1937, the Federal Milk Marketing Orders, or FMMO, were established under the Agricultural Marketing Agreement Act. The purpose of these orders was to set a monthly, uniform minimum price for milk based on its end use and to ensure that farmers were paid accurately and in a timely manner.

Farmers were paid based on how the milk they harvested was used, and that’s still how it works today.

Does it become bottled milk? That’s Class 1 price. Yogurt? Class 2 price. Cheddar cheese? Class 3 price. Butter or powdered dry milk? Class 4. Traditionally, Class 1 receives the highest price.

There are 11 FMMOs that divide up the country. The Florida, Southeast, and Appalachian FMMOs focus heavily on Class 1, or bottled, milk. The other FMMOs, such as Upper Midwest and Pacific Northwest, have more manufactured products such as cheese and butter.

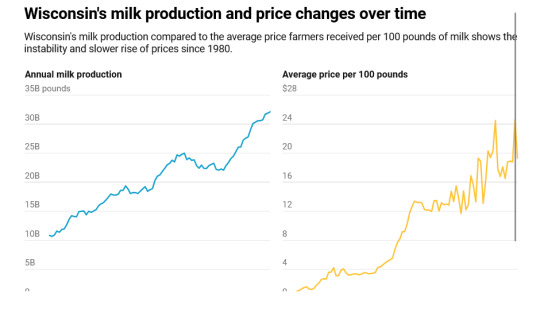

For the past several decades, farmers have generally received the minimum price. Improvements in milk quality, milk production, transportation, refrigeration, and processing all led to greater quantities of milk, greater shelf life, and greater access to products across the US. Growing supply reduced competition among processing plants and reduced overall prices.

Along with these improvements in production came increased costs of production, such as cattle feed, farm labor, veterinary care, fuel, and equipment costs.

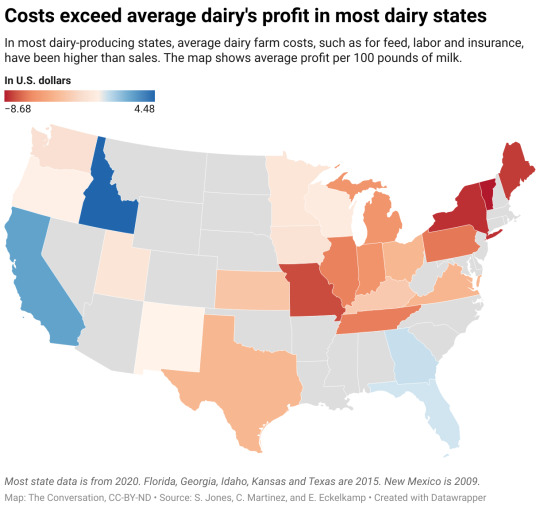

Researchers at the University of Tennessee in 2022 compared the price received for milk across regions against the primary costs of production: feed and labor. The results show why farms are struggling.

From 2005 to 2020, milk sales income per 100 pounds of milk produced ranged from $11.54 to $29.80, with an average price of $18.57. For that same period, the total costs to produce 100 pounds of milk ranged from $11.27 to $43.88, with an average cost of $25.80.

On average, that meant a single cow that produced 24,000 pounds of milk brought in about $4,457. Yet, it cost $6,192 to produce that milk, meaning a loss for the dairy farmer.

More efficient farms are able to reduce their costs of production by improving cow health, reproductive performance, and feed-to-milk conversion ratios. Larger farms or groups of farmers—cooperatives such as Dairy Farmers of America—may also be able to take advantage of forward contracting on grain and future milk prices. Investments in precision technologies such as robotic milking systems, rotary parlors, and wearable health and reproductive technologies can help reduce labor costs across farms.

Regardless of size, surviving in the dairy industry takes passion, dedication, and careful business management.

Some regions have had greater losses than others, which largely ties back to how farmers are paid, meaning the classes of milk, and the rising costs of production in their area. There are some insurance and hedging programs that can help farmers offset high costs of production or unexpected drops in price. If farmers take advantage of them, data shows they can functions as a safety net, but they don’t fix the underlying problem of costs exceeding income.

Passing the Torch to Future Farmers

Why do some dairy farmers still persist, despite low milk prices and high costs of production?

For many farmers, the answer is because it is a family business and a part of their heritage. Ninety-seven percent of US dairy farms are family owned and operated.

Some have grown large to survive. For many others, transitioning to the next generation is a major hurdle.

The average age of all farmers in the 2022 Census of Agriculture was 58.1. Only 9 percent were considered “young farmers,” age 34 or younger. These trends are also reflected in the dairy world. Yet, only 53 percent of all producers said they were actively engaged in estate or succession planning, meaning they had at least identified a successor.

How to Help Family Dairy Farms Thrive

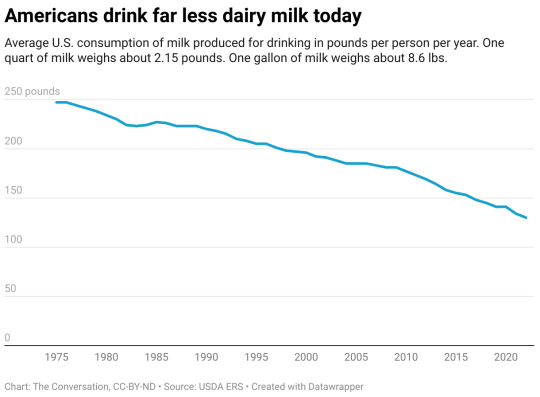

In theory, buying more dairy would drive up the market value of those products and influence the price producers receive for their milk. Society has actually done that. Dairy consumption has never been higher. But the way people consume dairy has changed.

Americans eat a lot, and I mean a lot, of cheese. We also consume a good amount of ice cream, yogurt, and butter, but not as much milk as we used to.

Does this mean the US should change the way milk is priced? Maybe.

The FMMO is currently undergoing reform, which may help stem the tide of dairy farmers exiting. The reform focuses on being more reflective of modern cows’ ability to produce greater fat and protein amounts; updating the cost support processors receive for cheese, butter, nonfat dry milk, and dried whey; and updating the way Class 1 is valued, among other changes. In theory, these changes would put milk pricing in line with the cost of production across the country.

The US Department of Agriculture is also providing support for four Dairy Business Innovation Initiatives to help dairy farmers find ways to keep their operations going for future generations through grants, research support, and technical assistance.

Another way to boost local dairies is to buy directly from a farmer. Value-added or farmstead dairy operations that make and sell milk and products such as cheese straight to customers have been growing. These operations come with financial risks for the farmer, however. Being responsible for milking, processing, and marketing your milk takes the already big job of milk production and adds two more jobs on top of it. And customers have to be financially able to pay a higher price for the product and be willing to travel to get it.

33 notes

·

View notes

Note

Hi fellow doll, I hope you're doing fine. I've been quite busy lately, college and life in general have been kicking my ass, so I was forced to take a step back from social media for a while to try to contain the chaos.

Firstly, I'd like to share a fun fact with you! I don't know if you're aware but did you know that Lou's Mansion has a Pool? You can see it more clearly in the Mansion's Concept Designs/Art on this site:

•https://www.claytonstillwell.com/ugly-dolls#23

However, the real reason for this ask is to present a possible answer/theory in regards to how the doll-sized phones came to be in the world of your stories (you can tell this is still related to our chat on Wattpad).

Recently, I came across the images you're seeing on Pinterest. They're Wide/Aerial Views of the Institute of Perfection and one thing that immediately stood out to me is that Giant Eye-Catching Dome behind the TV.

I mean what's its purpose, why is it even there to begin with and what's inside of it? I've been thinking about this for a while and would like to hear your thoughts about it as well, if you're willing to share them.

By any chance, have you seen the movie Wreck-it Ralph? There was a part where the villain enters the code of the game he's in and I think the Dome's purpose could follow a similar, if not equal, vein.

Now that I think about it, Lou and Vanellope's circunstances are almost identical, trapped in the same place for years without the option to leave, simply because of who they are and the traits they were born with, but didn't choose to have.

Sorry, I let my mind run on tangent there for a while, it wanders frequently which makes it hard to keep track of my line of thought.

To circle back to the main topic of discussion, what if the Dome is a Central Station of the Institute, like a Panel or Center for Command Control (or Command Control Center)? CCC for short? Ok, I'll stop trying to be funny...

Perhaps it could be a subroutine of the factory's software, a program linked to its network and wifi that contains all guidelines and rules that govern the Institute and must be followed and executed to keep it functional - a blueprint if you will - and is in charge of all commands, protocols, activities and operations being compiled and run by its machinery, such as the doll-scanner, the robots, the washing machine, the recycling, the Gauntlet plus the mechanical baby and dog and the Portal, just to name a few.

This means that it'd also take care of overseeing the integrity and performance of said machinery as well as its maintenance. It'd even be responsible for generating clouds and the artificial weather because apparently weather is still a thing, even though the Institute is inside of a factory.

I wonder if this subroutine would be run by an AI or simply an intelligent system/computer program. This world's version of Siri? 🤣

Or maybe I'm greatly exaggerating its function/letting my imagination run wild and it literally only gives Electricity for TV and Institute. Where was I going with this? /were we again?

Morever, it could be a storage unit that contains all collected, analysed and reviewed data regarding the inhabitants of the Institute and their responses, physical or emotional, to certain pre-determined stimuli.

It could also have a list of the factory's Perfection Standards: what consists/constitutes a Perfect Doll / product, its traits...

what can go to the market and which flaws/imperfections can't be ignored/overlooked and have to go to the recycling immediately, kinda like separating fruit/food

To sum up, it's the Institute's "rulebook", but instead of being specifically made for the prototype, it's more expansive and focuses on the Institute as a whole.

After the events of the movie, dolls with engineer role job created phones with recicled parts dangerous/turned the recycling into a good thing/while recycling was turned of and parts are human sized, plenty to spare and create phone since dolls come back now, have free time to assemble the parts and construct them and connected them to the signals/frequency emitted by the dome or they hack/steal or find out the password/'hijack' the signals🤣, use it to make them connect with each other but can't enter the dome without proper authorizations/permissions

Fun fact #2: Lou animatronic, would be a hipocrite if he called the Uglydolls "Ugly" has never seen a Mirror before

•https://www.indigobluepencil.com/ugly

Scroll almost to the middle (pre-planned concepts: dome by TV and washing machine, Big baby, Lou, Mandy, Tuesday and Kitty, Victoria, Perfection Council/of Dolls=board of investors directors reference)

•https://www.scottfassett.com/uglydolls-gallery

Had to restart Two Times... I hope you found this ask both entertaining and informative. Hopefully it'll give you Inspiration for your stories...

Okay, I had to do quite a bit of research and asked someone who knows a lot more about computers than I do.

So, I do agree that the dome has an electronic purpose. It really surprises me that STX animated an entire dome within the Institute and literally spoke nothing of it or what's inside of it. Like, seriously, it's huge and can't just be empty on the inside.

My theory, after some research, is that the inside of the dome is essentially a hard drive computer tower. For you younger folk who weren't raised in a 90's home, here's what I'm talking about:

These things right here used to be what would get hooked up to older Dell/Windows computers. The ones that weighed, like, 50 pounds and took up an entire desk.

Instead of a dvd player (which I didn't get one until maybe 8 years old) I would stick my Kidz Bop cd or movie into that slot at the top and watch the movie on the computer with Video Player.

Count your blessings.

But this is what I believe is inside that dome. These things are what holds the CPU (central processing unit), GPU (graphic processing unit), and stores the memory, data, audio, and everything of the computer.

@natalie-the-writer and I have a running fanon that the company is older. The technology is older, the building is older, and everything is set in a pretty retro time period. So, this hard drive tower is connected to those bulky take-up-all-the-space-on-the-desk-computers.

The GPU in this system is also what control the day/night cycle in the Institute and the weather. It essentially simulates a troposphere and an environment that makes the dolls comfortable and prepared for the Big World.

The CPU is how the data is transferred. Info from the robots is controlled and processed, the Individualization scanners are monitored, the portal is opened and closed, the TV runs, and the holographic tutorials Moxy and her friends see in the beginning are kept on, all of it.

It basically functions as the brain of the Institute, but the sole controller and monitor of it is the CEO (Greyson Everett).

I also like to think that Lou's microchip (another fanon thought between Natalie and I) is also monitored via this hard drive tower. Any information that Lou learns and processes is sent into separate files on the computers back in the company building.

This is why in my Shell-Shock series, when Lou's emotions go south, the Institute begins to get windy when he's hyperventilating or rains when he cries. The ground trembles when he has body tremors and the lights flicker when his powers are used. He is literally connected to the whole Institute because his microchip and its data accidentally grow and manifest themselves into the files of the other Institute functions. His programming basically goes rogue and infects the Institute system like a virus.

I'm veering toward the explanation that results in Lou being the first successful form of Artificial Intelligence. But, for the moment, he is basically acting like a virus and it's not until he learns to control this new system he's connected to that it stops becoming a deadly thing.

#uglydolls#lou#writing#ask#answer#theories#fanon theories#feel free to have your own thoughts#I'm just ranting#this is so interesting thank you for asking this

28 notes

·

View notes

Text

Aquatic Robot Market to Eyewitness Huge Growth by 2030

Latest business intelligence report released on Global Aquatic Robot Market, covers different industry elements and growth inclinations that helps in predicting market forecast. The report allows complete assessment of current and future scenario scaling top to bottom investigation about the market size, % share of key and emerging segment, major development, and technological advancements. Also, the statistical survey elaborates detailed commentary on changing market dynamics that includes market growth drivers, roadblocks and challenges, future opportunities, and influencing trends to better understand Aquatic Robot market outlook. List of Key Players Profiled in the study includes market overview, business strategies, financials, Development activities, Market Share and SWOT analysis: Atlas Maridan ApS. (Germany), Deep Ocean Engineering Inc. (United States), Bluefin Robotics Corporation (United States), ECA SA (France), International Submarine Engineering Ltd. (Canada), Inuktun Services Ltd. (Canada), Oceaneering International, Inc. (United States), Saab Seaeye (Sweden), Schilling Robotics, LLC (United States), Soil Machine Dynamics Ltd. (United Kingdom) Download Free Sample PDF Brochure (Including Full TOC, Table & Figures) @ https://www.advancemarketanalytics.com/sample-report/177845-global-aquatic-robot-market Brief Overview on Aquatic Robot: Aquatic robots are those that can sail, submerge, or crawl through water. They can be controlled remotely or autonomously. These robots have been regularly utilized for seafloor exploration in recent years. This technology has shown to be advantageous because it gives enhanced data at a lower cost. Because underwater robots are meant to function in tough settings where divers' health and accessibility are jeopardized, continuous ocean surveillance is extended to them. Maritime safety, marine biology, and underwater archaeology all use aquatic robots. They also contribute significantly to the expansion of the offshore industry. Two important factors affecting the market growth are the increased usage of advanced robotics technology in the oil and gas industry, as well as increased spending in defense industries across various countries. Key Market Trends: Growth in AUV Segment Opportunities: Adoption of aquatic robots in military & defense

Increased investments in R&D activities Market Growth Drivers: Growth in adoption of automated technology in oil & gas industry

Rise in awareness of the availability of advanced imaging system Challenges: Required highly skilled professional for maintenance Segmentation of the Global Aquatic Robot Market: by Type (Remotely Operated Vehicle (ROV), Autonomous Underwater Vehicles (AUV)), Application (Defense & Security, Commercial Exploration, Scientific Research, Others) Purchase this Report now by availing up to 10% Discount on various License Type along with free consultation. Limited period offer. Share your budget and Get Exclusive Discount @: https://www.advancemarketanalytics.com/request-discount/177845-global-aquatic-robot-market Geographically, the following regions together with the listed national/local markets are fully investigated: • APAC (Japan, China, South Korea, Australia, India, and Rest of APAC; Rest of APAC is further segmented into Malaysia, Singapore, Indonesia, Thailand, New Zealand, Vietnam, and Sri Lanka) • Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe; Rest of Europe is further segmented into Belgium, Denmark, Austria, Norway, Sweden, The Netherlands, Poland, Czech Republic, Slovakia, Hungary, and Romania) • North America (U.S., Canada, and Mexico) • South America (Brazil, Chile, Argentina, Rest of South America) • MEA (Saudi Arabia, UAE, South Africa)Furthermore, the years considered for the study are as follows: Historical data – 2017-2022 The base year for estimation – 2022 Estimated Year – 2023 Forecast period** – 2023 to 2028 [** unless otherwise stated] Browse Full in-depth TOC @: https://www.advancemarketanalytics.com/reports/177845-global-aquatic-robot-market

Summarized Extracts from TOC of Global Aquatic Robot Market Study Chapter 1: Exclusive Summary of the Aquatic Robot market Chapter 2: Objective of Study and Research Scope the Aquatic Robot market Chapter 3: Porters Five Forces, Supply/Value Chain, PESTEL analysis, Market Entropy, Patent/Trademark Analysis Chapter 4: Market Segmentation by Type, End User and Region/Country 2016-2027 Chapter 5: Decision Framework Chapter 6: Market Dynamics- Drivers, Trends and Challenges Chapter 7: Competitive Landscape, Peer Group Analysis, BCG Matrix & Company Profile Chapter 8: Appendix, Methodology and Data Source Buy Full Copy Aquatic RobotMarket – 2021 Edition @ https://www.advancemarketanalytics.com/buy-now?format=1&report=177845 Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global Aquatic Robot Market#Aquatic Robot Market Demand#Aquatic Robot Market Trends#Aquatic Robot Market Analysis#Aquatic Robot Market Growth#Aquatic Robot Market Share#Aquatic Robot Market Forecast#Aquatic Robot Market Challenges

2 notes

·

View notes

Text

Labor Challenges In Food Manufacturing

Introduction

The food manufacturing industry is the heart of our modern food supply chain, responsible for producing the vast array of products that fill our grocery store shelves. However, behind the scenes, this industry faces a host of labor challenges that impact not only its operations but also the quality and safety of the food we consume. In this blog post, we’ll explore some of the key labor challenges facing food manufacturers and the potential solutions to address them.

Workforce Shortages

One of the most pressing issues in the food manufacturing industry is workforce shortages. This challenge has been exacerbated by factors such as an aging workforce, high turnover rates, and the difficulty of attracting new talent. Food manufacturing facilities often require a diverse skill set, from food safety and quality control to machine operation and logistics, making it challenging to find qualified workers.

Solution: Companies can address this issue by investing in workforce development programs, offering competitive wages and benefits, and leveraging automation and technology to reduce the need for manual labor in repetitive or dangerous tasks.

2. Food Safety and Quality Assurance

Ensuring food safety and maintaining high-quality standards are paramount in food manufacturing. However, labor challenges can compromise these goals. A shortage of skilled workers can lead to mistakes in food handling and processing, increasing the risk of contamination and product recalls.

Solution: Comprehensive training programs, stricter adherence to safety protocols, and the implementation of advanced quality control technologies can help mitigate these risks.

3. Rising Labor Costs

Labor costs in the food manufacturing industry have been steadily rising, driven by factors such as minimum wage increases, healthcare costs, and worker demand for higher pay. Small and medium-sized manufacturers may find it particularly challenging to absorb these escalating costs.

Solution: To address rising labor costs, manufacturers can explore process optimization, automation, and robotics to increase efficiency and reduce the need for manual labor.

4. Regulatory Compliance

The food manufacturing industry is highly regulated to ensure the safety and quality of products. Compliance with these regulations is essential but can be a daunting challenge, especially for smaller businesses with limited resources. Keeping up with evolving food safety laws and industry standards is a constant struggle.

Solution: Companies can navigate regulatory challenges by investing in compliance management systems, regularly training employees on food safety standards, and staying informed about changes in regulations.

5. Labor Unions and Collective Bargaining

Labor unions play a significant role in the food manufacturing industry, and negotiations can lead to labor disputes, strikes, and work stoppages. These disruptions can impact production schedules and lead to losses in revenue.

Solution: Open and respectful communication between management and labor unions is key to preventing labor disputes. Collaborative bargaining and compromise can help maintain a stable workforce.

Conclusion

Labor challenges in food manufacturing are complex and multifaceted, but they are not insurmountable. By investing in workforce development, embracing automation and technology, prioritizing safety and quality, and adapting to changing regulations, food manufacturers can navigate these challenges more effectively. A resilient and skilled workforce is essential for ensuring the continued production of safe and high-quality food products that meet the demands of consumers in an ever-changing world.

https://www.linkedin.com/in/brian-twomey-4a017510/

6 notes

·

View notes

Text

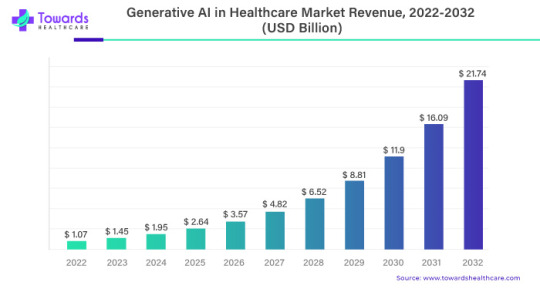

Generative AI in Healthcare Market to Grow at an 35.1% CAGR Till 2032!

The global Generative AI in Healthcare Market worth USD 1.07 billion in 2023 is likely to be USD 21.74 billion by 2032, growing at a 35.1% CAGR between 2023 and 2032.

According to the stats published by World Health Organization (WHO), approximately 1.28 million adults (between 30 and 79 years of age) have hypertension. Of these, as little as 42% of adults are diagnosed and treated correctly and the remaining population is unaware of this condition. The majority of this population resides in low to middle-income countries of the world. Despite this substantial number of untreated cases, the rising awareness among doctors and the general population regarding health illnesses associated with hypertension is expected to drive the demand for the required devices.

Download White Paper@ https://www.towardshealthcare.com/personalized-scope/5069

A recent report provides crucial insights along with application based and forecast information in the Global Generative AI in Healthcare Market. The report provides a comprehensive analysis of key factors that are expected to drive the growth of this Market. This study also provides a detailed overview of the opportunities along with the current trends observed in the Generative AI in Healthcare Market.

A quantitative analysis of the industry is compiled for a period of 10 years in order to assist players to grow in the Market. Insights on specific revenue figures generated are also given in the report, along with projected revenue at the end of the forecast period.

Report Objectives

To define, describe, and forecast the global Generative AI in Healthcare Market based on product, and region

To provide detailed information regarding the major factors influencing the growth of the Market (drivers, opportunities, and industry-specific challenges)

To strategically analyze microMarkets1 with respect to individual growth trends, future prospects, and contributions to the total Market

To analyze opportunities in the Market for stakeholders and provide details of the competitive landscape for Market leaders

To forecast the size of Market segments with respect to four main regions—North America, Europe, Asia Pacific and the Rest of the World (RoW)2

To strategically profile key players and comprehensively analyze their product portfolios, Market shares, and core competencies3

To track and analyze competitive developments such as acquisitions, expansions, new product launches, and partnerships in the Generative AI in Healthcare Market

Companies and Manufacturers Covered

The study covers key players operating in the Market along with prime schemes and strategies implemented by each player to hold high positions in the industry. Such a tough vendor landscape provides a competitive outlook of the industry, consequently existing as a key insight. These insights were thoroughly analysed and prime business strategies and products that offer high revenue generation capacities were identified. Key players of the global Generative AI in Healthcare Market are included as given below:

Generative AI in Healthcare Market Key Players:

Syntegra

NioyaTech

Saxon

IBM Watson

Microsoft Corporation

Google LLC

Tencent Holdings Ltd.

Neuralink Corporation

OpenAI

Oracle

Market Segments :

By Application

Clinical

Cardiovascular

Dermatology

Infectious Disease

Oncology

Others

System

Disease Diagnosis

Telemedicine

Electronic Health Records

Drug Interaction

By Function

AI-Assisted Robotic Surgery

Virtual Nursing Assistants

Aid Clinical Judgment/Diagnosis

Workflow & Administrative Tasks

Image Analysis

By End User

Hospitals & Clinics

Clinical Research

Healthcare Organizations

Diagnostic Centers

Others

By Geography

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

Contact US -

Towards Healthcare

Web: https://www.towardshealthcare.com/

You can place an order or ask any questions, please feel free to contact at

Email: [email protected]

About Us

We are a global strategy consulting firm that assists business leaders in gaining a competitive edge and accelerating growth. We are a provider of technological solutions, clinical research services, and advanced analytics to the healthcare sector, committed to forming creative connections that result in actionable insights and creative innovations.

#seo marketing#seo#market analysis#market share#marketing#ai#artificial intelligence#Generative AI#healthcare

2 notes

·

View notes

Text

Setting Up a Warehouse in Gurgaon – What You Need to Know

Gurgaon, now officially known as Gurugram, is one of the most sought-after business hubs in India. With its proximity to Delhi, excellent infrastructure, and booming industrial growth, it has become a prime location for setting up warehouses. Whether you're a logistics company, an e-commerce giant, or a manufacturing firm, establishing a warehouse in Gurgaon can significantly enhance your supply chain efficiency.

However, setting up a warehouse involves several key considerations—from location selection to legal compliances. In this guide, we’ll walk you through everything you need to know before setting up a warehouse in Gurgaon.

Why Choose Gurgaon for Your Warehouse?

Gurgaon offers several advantages for businesses looking to establish a warehouse:

Strategic Location – Gurgaon is well-connected to Delhi, Faridabad, Noida, and other major cities via highways like NH-8 and the Delhi-Mumbai Expressway.

Proximity to Key Markets – Being close to the national capital and major industrial zones makes it ideal for distribution.

Infrastructure & Connectivity – The city has excellent road networks, upcoming metro expansions, and easy access to airports and railways.

Thriving Industrial Zones – Areas like Manesar, Sohna Road, and Farukhnagar are popular for warehousing due to better land availability and lower costs compared to Delhi.

Government Support – Haryana’s industrial policies offer incentives for logistics and warehousing businesses.

Key Factors to Consider Before Setting Up a Warehouse in Gurgaon

1. Location Selection

Choosing the right location is crucial for operational efficiency. Consider:

Proximity to Highways & Transport Hubs – Locations near NH-8, Dwarka Expressway, or KMP Expressway ensure smooth logistics.

Accessibility to Customers & Suppliers – Being closer to industrial clusters like Manesar or Udyog Vihar can reduce transportation costs.

Future Growth Potential – Areas like Sohna and Farukhnagar are emerging as warehousing hotspots due to lower land prices.

2. Legal & Regulatory Compliance

Before acquiring or leasing a warehouse, ensure all legal formalities are in place:

Land Zoning & Approvals – Verify if the land is designated for industrial or warehousing use.

Fire Safety & Building Codes – Obtain necessary NOCs from the fire department and municipal authorities.

Environmental Clearances – Depending on the warehouse size, you may need pollution control board approvals.

GST Registration & Warehouse Licensing – Ensure proper documentation for tax and logistics compliance.

3. Warehouse Design & Layout

A well-planned warehouse improves efficiency. Key aspects include:

Storage Systems – Decide between pallet racking, shelving, or automated storage solutions.

Loading & Unloading Docks – Ensure sufficient space for trucks and material handling equipment.

Ventilation & Lighting – Proper airflow and lighting enhance worker productivity and safety.

Security Measures – Install CCTV, access control, and alarm systems to prevent theft.

4. Cost Considerations

Setting up a warehouse involves multiple expenses:

Land or Rental Costs – Prices vary based on location; Manesar and Sohna offer more affordable options than central Gurgaon.

Construction & Fit-out Costs – Customizing the warehouse with racks, flooring, and automation adds to expenses.

Operational Costs – Include staffing, utilities, maintenance, and security in your budget.

5. Technology & Automation

Modern warehouses leverage technology for efficiency:

Warehouse Management Systems (WMS) – Software for inventory tracking and order management.

Automated Material Handling – Conveyor belts, robotic pickers, and forklifts reduce manual labor.

IoT & RFID Tracking – Real-time monitoring of goods enhances supply chain visibility.

6. Workforce & Manpower Planning

A skilled workforce ensures smooth operations:

Hiring Trained Staff – Forklift operators, inventory managers, and security personnel are essential.

Training Programs – Regular training improves efficiency and safety compliance.

Labor Laws Compliance – Follow Haryana’s labor regulations for wages and working conditions.

7. Future Expansion Possibilities

As your business grows, scalability becomes crucial:

Leasing vs. Buying – Leasing offers flexibility, while buying provides long-term asset benefits.

Modular Warehouse Designs – Opt for expandable layouts to accommodate future needs.

Best Areas for Warehousing in Gurgaon

Here are some top locations to consider:

Manesar – A major industrial hub with affordable land and excellent connectivity.

Sohna Road – Emerging as a warehousing hotspot with good infrastructure.

Farukhnagar – Ideal for large warehouses due to lower land costs.

Udyog Vihar – Suitable for small to mid-sized warehouses near industrial units.

Conclusion

Setting up a warehouse in Gurgaon requires careful planning—from selecting the right location to ensuring legal compliance and operational efficiency. With its strategic advantages and growing industrial base, Gurgaon remains a top choice for businesses looking to strengthen their logistics network.

#gurgaon properties#gurgaonrealestate#best residential properties in gurgaon#best investment plan#real estate properties#residential projects in gurgaon

0 notes

Link

0 notes

Text

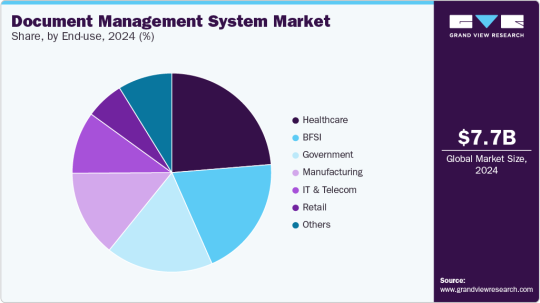

AI in Action: Intelligent Solutions for the Document Management System Market

The global document management system market was valued at USD 7.68 billion in 2024 and is projected to reach USD 18.17 billion by 2030, demonstrating a robust Compound Annual Growth Rate (CAGR) of 15.9% from 2025 to 2030. This expansion is primarily fueled by organizations' increasing need to securely manage and store vast volumes of digital information.

As businesses worldwide embrace digital transformation and move towards paperless operations, the demand for effective solutions for document storage, retrieval, and management has escalated. The accelerated adoption of cloud-based DMS solutions has further spurred this trend, offering businesses scalable, cost-effective, and readily accessible options. Moreover, the heightened focus on compliance and regulatory mandates is significantly contributing to the growth of the DMS industry. Enterprises operating in heavily regulated sectors like healthcare, finance, and legal are increasingly implementing DMS to ensure strict adherence to data security, privacy, and record-keeping regulations. These systems facilitate streamlined audits, maintain secure document trails, and mitigate the risk of non-compliance penalties.

Key Market Trends & Insights:

Regional Leadership: The North American document management system market commanded a substantial revenue share of almost 40.0% in 2024, driven by the escalating demand for digital transformation across various industries.

Component Dominance: The software segment held the largest market share, exceeding 67.0% of the revenue in 2024. This dominance is attributed to the growing demand for cloud-based, AI-driven, and compliance-ready solutions.

Deployment Preference: The cloud segment led the market with a revenue share of over 67.0% in 2024. This is propelled by the integration of advanced technologies such as Artificial Intelligence (AI), Machine Learning (ML), and Robotic Process Automation (RPA) into cloud DMS platforms.

Enterprise Size Leadership: Large enterprises accounted for nearly 67.0% of the market's revenue share in 2024. This is due to the immense volume of enterprise-grade documents they manage and their critical need for scalable, secure, and intelligent document workflows.

End-Use Sector Dominance: The healthcare segment generated over 23.0% of the market's revenue share in 2024. A significant driver here is the accelerating shift towards Electronic Health Records (EHRs) and paperless systems within the healthcare industry.

Order a free sample PDF of the Document Management System Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 7.68 billion

2030 Projected Market Size: USD 18.17 billion

CAGR (2025-2030): 15.9%

North America: Largest market in 2024

Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Leading companies in the document management system (DMS) industry, including Microsoft, IBM Corporation, Oracle Corporation, Open Text Corporation, and Hyland Software, Inc., are actively engaged in strategic initiatives to enhance their competitive edge. These strategies largely involve new product development, forging partnerships and collaborations, and entering into agreements.

Illustrative of these efforts, in April 2025, Hyland Software, Inc. significantly expanded its product offerings by integrating advanced AI capabilities. Through substantial updates to Hyland Automate, Hyland Knowledge Discovery, and key improvements to Hyland OnBase and Hyland Alfresco, the company aims to provide organizations with sophisticated tools for optimizing content, processes, and application intelligence. Their Hyland Content Intelligence product line is designed to empower businesses with actionable insights derived from simple natural language queries, thereby streamlining complex searches and delivering precise information from vast enterprise content.

Similarly, in March 2025, IBM Corporation launched IBM Storage Ceph as a Service, broadening its suite of flexible on-premises infrastructure solutions. This new service complements IBM Power delivered as a service, offering a distributed compute platform with diverse form factors and adaptable consumption models. The IBM Storage Ceph service facilitates the integration of cloud-based solutions with on-premises environments, providing a unified software-defined storage solution that encompasses block, file, and object data. Its goal is to help organizations eliminate data silos and modernize their data lakes and virtual machine storage, delivering a seamless cloud storage experience within their own data centers.

Further demonstrating industry innovation, in December 2024, OpenText introduced Core Digital Asset Management (Core DAM). This solution is engineered to optimize the digital content supply chain by incorporating powerful features that yield tangible results. Core DAM leverages practical AI to automate tasks such as image tagging, video transcript generation, and the creation of design inspiration images using OpenText Experience Aviator, significantly boosting the efficiency and accuracy of creative workflows. It also provides global content access, enabling users to generate instant links for high-performance display worldwide.

Key Players

Agiloft, Inc.

Alfresco Software Inc.

Cflowapps

DocLogix

Hyland Software, Inc.

IBM Corporation

Integrify

Browse Horizon Databook for Global Document Management System Market Size & Outlook

Conclusion

The document management system (DMS) market is rapidly growing, driven by the need for secure digital information management and paperless transitions. Cloud-based solutions and regulatory compliance are key growth factors. North America leads the market, with software and cloud deployments dominating. Large enterprises and the healthcare sector are major adopters. Leading companies are innovating with AI and strategic collaborations to enhance their offerings.

0 notes

Text

[250 Pages Report] The robot Operating System market is valued at USD 581 million in 2023 and is projected to reach USD 1,082 million by 2028, growing at a CAGR of 13.2% from 2023 to 2028. The increasing adoption of robot operating system in the automotive industry, are among factors that contribute to the growth of the market.

0 notes

Text

Flexible Automation Needs Drive Strong Demand for Collaborative Robots

The global collaborative robot (cobot) market was valued at USD 1.2 billion in 2023 and is projected to expand at a remarkable CAGR of 26.1% from 2024 to 2034, reaching a market size of USD 15.3 billion by the end of 2034, according to the latest industry research. This exponential growth is primarily driven by the growing demand for workplace automation, enhanced safety standards, and advancements in robotics technology.

Market Overview: Collaborative robots designed to work safely alongside humans are transforming industries by combining precision, productivity, and adaptability. Unlike traditional industrial robots, cobots feature integrated safety mechanisms, including force-limiting sensors and intelligent programming, enabling them to perform tasks in dynamic environments shared with human workers.

These robots are increasingly adopted across industries including automotive, electronics & semiconductors, healthcare, food & beverage, and logistics, owing to their flexibility, efficiency, and cost-effectiveness.

Market Drivers & Trends

1. Surging Demand for Automation

Industries worldwide are facing escalating labor costs and demand for consistent output. Cobots are bridging the gap by enhancing productivity without replacing human labor, enabling businesses to stay competitive in fast-evolving global markets.

2. Focus on Workplace Safety & Ergonomics

Companies are investing heavily in solutions that enhance worker safety and comfort. Cobots, designed with built-in torque and speed control features, address these concerns effectively—significantly reducing workplace injuries and enhancing job satisfaction.

3. Flexibility and Reusability

Cobots can be easily programmed, re-deployed, and adapted for various tasks. This makes them invaluable in dynamic production settings, especially in consumer electronics and automotive manufacturing, where production lines often change.

Latest Market Trends

Integration of AI Capabilities: The latest cobots incorporate artificial intelligence and machine learning, enabling smarter task execution, predictive maintenance, and real-time decision-making.

Human-Robot Collaboration Enhancements: Next-gen cobots are now equipped with advanced vision systems, touch sensitivity, and voice commands, allowing seamless interaction with human co-workers.

Compact and Lightweight Designs: Smaller cobots are gaining traction among SMEs that require affordable automation with minimal footprint.

Key Players and Industry Leaders

The collaborative robot market is moderately consolidated, with leading players holding around 55–60% market share. Major companies include:

ABB Group

FANUC CORPORATION

KUKA AG

Kawasaki Heavy Industries Ltd.

Mitsubishi Electric Corporation

Yaskawa Electric Corporation

OMRON Corporation

Schneider Electric SE

These companies are investing aggressively in R&D, product portfolio expansion, and strategic acquisitions.

Access an overview of significant conclusions from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=15536

Recent Developments

Universal Robots launched the UR20 in April 2023, the company’s most powerful cobot, featuring a 20 kg payload and a 1750 mm reach—ideal for heavy-duty applications.

In March 2023, Fanuc upgraded its CRX series with enhanced AI features, simplifying programming and improving adaptability for diverse manufacturing tasks.

ABB introduced the GoFa cobot, combining high payload capacity with safety-focused operations for assembly and material handling.

Market Opportunities

As cobot technologies evolve, new applications are emerging in healthcare, pharmaceuticals, logistics, and 3PL operations. These sectors are expected to witness substantial adoption due to labor shortages and increasing demand for precision, hygiene, and continuous operations.

The electronics & semiconductors sector, in particular, is anticipated to remain a dominant force, holding a 26.5% market share in 2023 and forecast to grow at a 30.9% CAGR, driven by increasing complexity in microelectronic assemblies.

Future Outlook

Analysts forecast a bright future for the collaborative robot industry, with wider integration across small and medium-sized enterprises, AI-embedded robotics, and scalable solutions becoming the norm. Governments supporting smart manufacturing and Industry 4.0 are further fueling demand.

Companies that adopt cobot solutions early stand to benefit from:

Increased output

Enhanced safety

Greater operational flexibility

Reduced downtime

Stronger return on investment (ROI)

Market Segmentation

By Type:

Power and Force Limiting Cobots

Hand Guiding Cobots

Safety Monitored Stop Cobots

Speed and Separation Cobots

By Component:

Hardware (End Effectors, Robot Arm, Controllers, Sensors)

Software

Services

By Payload:

<5 Kg

5–10 Kg

10–20 Kg

Above 20 Kg

By Application:

Material Handling

Assembly

Inspection & Quality Testing

Painting

Others

By End-use Industry:

Automotive

Electronics & Semiconductors

Healthcare

Food & Beverage

Aerospace & Defense

3PL

Others

Regional Insights

Asia Pacific led the global collaborative robot market in 2023 with a 34.2% share and is expected to grow at 28.9% CAGR. The region houses the world’s top manufacturing economies—China, Japan, South Korea, and India—driven by:

Large-scale manufacturing units

Government incentives for automation

Growing SMEs looking for cost-effective automation solutions

North America and Europe are also growing steadily due to technological maturity and early adoption of automation solutions.

Why Buy This Report?

Comprehensive market sizing and forecasts (2024–2034)

Detailed segmentation by type, payload, component, application, and region

Strategic analysis of key players and market shares

Coverage of recent innovations and technological developments

Insights into growth opportunities and investment areas

Regional performance analysis across North America, Europe, Asia Pacific, and more

In-depth industry dynamics: drivers, restraints, and future prospects

Explore Latest Research Reports by Transparency Market Research:

Surface Acoustic Wave (SAW) Devices Market: https://www.transparencymarketresearch.com/surface-acoustic-wave-sensors.html

Rugged Power Supply Market: https://www.transparencymarketresearch.com/rugged-power-supply-market.html

Ceramified Cable Market: https://www.transparencymarketresearch.com/ceramified-cable-market.html

Gantry (Cartesian) Robot Market: https://www.transparencymarketresearch.com/gantry-robot-market.htmlAbout Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Solar Panel Cleaning Market

Solar Panel Cleaning Market size is valued at $690 Million in 2022 and is expected to reach a value of $1.8 billion by 2030 at a CAGR of 13% during the forecast period 2023–2030.

🔗 𝐆𝐞𝐭 𝐑𝐎𝐈-𝐟𝐨𝐜𝐮𝐬𝐞𝐝 𝐢𝐧𝐬𝐢𝐠𝐡𝐭𝐬 𝐟𝐨𝐫 𝟐𝟎𝟐𝟓-𝟐𝟎𝟑𝟏 → 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐍𝐨𝐰

Solar panel cleaning is essential to maintain the efficiency and longevity of solar energy systems. Over time, dust, dirt, bird droppings, and pollution accumulate on panels, blocking sunlight and reducing power output. Regular cleaning ensures panels absorb maximum sunlight, improving energy production and saving money on electricity bills. Professional cleaning uses gentle, eco-friendly methods to avoid damaging the panels while removing grime effectively. Clean panels not only boost performance but also extend the system’s lifespan.

1️⃣𝐒𝐮𝐫𝐠𝐞 𝐢𝐧 𝐒𝐨𝐥𝐚𝐫 𝐈𝐧𝐬𝐭𝐚𝐥𝐥𝐚𝐭𝐢𝐨𝐧𝐬: The global shift towards renewable energy has led to an increase in solar panel installations. To maintain optimal performance and energy output, regular cleaning is essential, thereby boosting demand for cleaning services.

2️⃣𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐢𝐜𝐚𝐥 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐦𝐞𝐧𝐭𝐬: Innovations such as automated cleaning systems, robotic cleaners, and AI-driven solutions have enhanced cleaning efficiency and reduced labor costs. These technologies also promote water conservation and minimize environmental impact.

3️⃣𝐆𝐨𝐯𝐞𝐫𝐧𝐦𝐞𝐧𝐭 𝐈𝐧𝐜𝐞𝐧𝐭𝐢𝐯𝐞𝐬 𝐚𝐧𝐝 𝐏𝐨𝐥𝐢𝐜𝐢𝐞𝐬: Subsidies and tax incentives for solar installations have lowered initial costs, leading to increased adoption. Additionally, some policies mandate regular maintenance, including cleaning, to ensure the effectiveness of solar panels.

4️⃣𝐄𝐧𝐯𝐢𝐫𝐨𝐧𝐦𝐞𝐧𝐭𝐚𝐥 𝐀𝐰𝐚𝐫𝐞𝐧𝐞𝐬𝐬: As consumers become more environmentally conscious, there’s a growing preference for sustainable cleaning methods, such as waterless or eco-friendly solutions, which further drives market growth.

5️⃣𝐑𝐢𝐬𝐢𝐧𝐠 𝐄𝐥𝐞𝐜𝐭𝐫𝐢𝐜𝐢𝐭𝐲 𝐃𝐞𝐦𝐚𝐧𝐝: The increasing need for electricity, especially in regions with high solar adoption, necessitates the efficient operation of solar panels, leading to a higher demand for cleaning services to maintain energy production.

𝐓𝐨𝐩 𝐊𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬:

Kept Companies | CSG Glass | HB McClure Company | Perfect Solar Home | Schimmer Metal Standard | BOL WORKS Ltd. | Solar panel & solar cells manufacturer — Solar N Plus | Solar Panel Manufacturer — UK | First Solar | Solar Leading | Zhejiang Shengtai Energy Solar Panel Manufacturer | Solar Brasil | ADT Solar

#SolarPanelCleaning #CleanEnergy #SolarPower #EcoFriendlyCleaning #RenewableEnergy #SolarEfficiency #GreenEnergy #SolarMaintenance #CleanSolarPanels #SustainableEnergy

0 notes

Text

Vertical Farming Market to Hit $13.7 Billion by 2029 Driven by AI and Sustainability

The Vertical Farming Market is poised for exponential growth, forecasted to increase from approximately USD 5.6 billion in 2024 to USD 13.7 billion by 2029, growing at a compound annual growth rate (CAGR) of 19.7%. This transformation is being driven by urbanization, increasing food demand, water scarcity, and technological innovations including artificial intelligence (AI), LED lighting, and hydroponic systems.

To Get Free Sample Report: https://www.datamintelligence.com/download-sample/vertical-farming-market

Market Drivers and Growth Opportunities

Scarcity of Arable Land and Water Vertical farming systems require up to 97% less water and significantly less land than traditional farming, making them ideal for densely populated cities and regions suffering from water scarcity.

Integration of AI and Automation AI is revolutionizing vertical farming by enabling predictive analytics, automation of nutrient delivery, environmental control, and yield optimization. Coupled with IoT and sensors, farms can operate efficiently with minimal human input.

Year-Round Production and Urban Scalability Controlled environment agriculture allows year-round production regardless of climate conditions. This is especially crucial in urban areas where local food production can reduce dependency on external supply chains and transportation.

Rising Demand for Clean, Pesticide-Free Produce Health-conscious consumers are driving demand for fresh, pesticide-free food. Vertical farming offers a solution with clean growing environments that eliminate the need for chemical treatments.

Government Incentives and Policy Support Supportive policies in both developed and developing countries are fostering investment and research in sustainable agricultural practices, including vertical farming.

U.S. Market Insights

The United States is one of the leading adopters of vertical farming technology. In urban food deserts regions with limited access to fresh food small and modular farms are addressing local needs. For example, projects in cities like Houston, Phoenix, and Mesa are creating access to greens using hydroponics and aeroponics.

Energy use remains a major challenge, as climate-controlled farms consume high levels of electricity. However, innovators are mitigating this through renewable energy integration and partnerships with local energy providers. Furthermore, advanced LED lighting is being optimized for energy efficiency.

Despite some high-profile vertical farm companies declaring bankruptcy due to overexpansion or unprofitable scale, many small and mid-size operators are succeeding with localized, efficient models. Companies like Bowery Farming are providing produce to major retailers including Walmart and Whole Foods, supported by automation and AI tools that streamline farm management.

Startups like True Garden are demonstrating profitability with container-based models, producing thousands of pounds of greens each month while using 90–98% less water than traditional farms.

Japan Market Trends

Japan’s vertical farming industry is expanding rapidly, driven by the need for domestic food production and sustainability. Indoor farms, known as "vegetable factories," are increasingly integrated into urban environments. The vertical farming market in Japan was valued at USD 402 million in 2024 and is projected to reach USD 879 million by 2033, with a CAGR of 9.1%.

Robotics, biosciences, and AI are at the core of Japan's vertical farming technology. Companies like Spread are leveraging cloud-based farm management systems to distribute greens to thousands of retail stores. The cultural alignment with sustainability, minimal waste, and urban efficiency positions Japan as a key global influencer in vertical farming.

Government funding and corporate investment are further accelerating growth, particularly in the development of fully automated farming systems that reduce reliance on human labor.

Global Market Landscape

The Asia-Pacific region, beyond Japan, is also witnessing notable growth. In 2023, the market was valued at USD 1.77 billion and is projected to reach USD 7.04 billion by 2030 at a CAGR of 21.8%. Countries such as Singapore, South Korea, and China are investing heavily in vertical farming for urban food security.

Hydroponics is currently the dominant method due to its water efficiency and scalability. Aeroponics is gaining momentum, especially in Japan and parts of Europe, due to its superior nutrient delivery and root oxygenation.

Investment Opportunities

Vertical farming is attracting venture capital across multiple fronts:

Automation and AI: Investors are prioritizing platforms that use AI to manage farm ecosystems in real-time.

Container and Modular Farms: Scalable, transportable farms offer a solution for urban redevelopment and rural supply gaps.

Premium Crop Segments: High-value crops like microgreens, strawberries, and herbs offer better margins for vertical farmers.

Food Security Projects: Urban governments and non-profits are partnering with startups to launch vertical farms in underserved neighborhoods.

Get the Demo Full Report : https://www.datamintelligence.com/enquiry/vertical-farming-market

Industry Challenges

High Energy and Infrastructure Costs Energy-intensive systems for lighting, heating, and environmental control present cost challenges. Co-locating farms with renewable energy sources is a potential solution.

Scalability and Profitability Balance Large-scale operations often struggle with profitability, whereas smaller localized farms show better financial performance and community impact.

Supply Chain and Distribution Ensuring freshness and shelf life, especially for leafy greens, requires efficient local distribution networks.

Conclusion

The vertical farming market is on a transformative path. Innovations in AI, hydroponics, and sustainable lighting are enabling farms to flourish in environments previously unsuitable for agriculture. While energy consumption and initial investment remain hurdles, the long-term benefits of local food production, water savings, and food security are positioning vertical farming as a central player in the future of agriculture. With leadership from the U.S. and Japan, and rapid growth in the Asia-Pacific region, vertical farming is no longer experimental it is becoming essential.

0 notes

Text

5G IoT Chip Market: Technology Trends and Future Outlook 2025–2032

MARKET INSIGHTS

The global 5G IoT Chip market size was valued at US$ 4.87 billion in 2024 and is projected to reach US$ 12.43 billion by 2032, at a CAGR of 14.6% during the forecast period 2025-2032.

5G IoT chips are specialized semiconductor components that integrate 5G connectivity with IoT device functionalities. These system-on-chips (SoCs) combine radio frequency (RF) transceivers, baseband processors, and application processors in compact form factors, enabling high-speed, low-latency wireless communication for smart devices. Leading manufacturers are focusing on chips manufactured at 7nm, 10nm, and 12nm process nodes to balance performance and power efficiency.

The market expansion is driven by several factors, including the rollout of 5G infrastructure globally, increasing demand for industrial automation, and the proliferation of smart city applications. While the semiconductor industry overall grows at 6% CAGR, 5G IoT chips represent one of the fastest-growing segments due to their critical role in enabling next-generation applications. Key players like Qualcomm, MediaTek, and Intel are investing heavily in R&D to develop energy-efficient chips capable of supporting massive machine-type communications (mMTC) and ultra-reliable low-latency communications (URLLC) – two fundamental 5G IoT use cases.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 5G Network Infrastructure Accelerating IoT Chip Adoption

The global rollout of 5G networks is creating unprecedented demand for compatible IoT chipsets. With over 290 commercial 5G networks deployed worldwide as of early 2024, telecom operators are investing heavily in infrastructure that requires low-latency, high-bandwidth connectivity solutions. The enhanced capabilities of 5G—including speeds up to 100 times faster than 4G and latency under 5 milliseconds—enable mission-critical IoT applications that were previously impractical. This technological leap is driving adoption across industries from manufacturing to healthcare, where real-time data processing is becoming essential for operational efficiency. Recent enhancements in network slicing capabilities further allow customized connectivity solutions for diverse IoT use cases.

Industrial Automation Revolution Driving Demand for Robust Connectivity Solutions

Industry 4.0 transformation across manufacturing sectors is creating substantial demand for 5G IoT chips capable of supporting advanced automation. Smart factories require thousands of connected sensors, actuators and control systems that demand reliable, low-latency communication. Predictive maintenance applications alone are projected to save manufacturers billions annually through reduced downtime. Autonomous mobile robots (AMRs) in warehouse operations increasingly rely on 5G’s ultra-reliable low-latency communication (URLLC) capabilities, creating new requirements for industrial-grade IoT chipsets. The growing integration of AI at the edge further intensifies processing demands, prompting chipmakers to develop solutions that combine 5G connectivity with neural processing capabilities.

Government Initiatives for Smart City Development Stimulating Market Growth

National smart city programs globally are accelerating deployment of 5G-powered IoT solutions for urban infrastructure management. Many governments have designated 5G as critical infrastructure, with billions allocated for digital transformation projects. Smart utilities, intelligent transportation systems, and public safety applications collectively require millions of connected devices. Smart meter deployments alone are projected to exceed 1.5 billion units globally by 2027, with advanced models incorporating 5G connectivity for real-time grid monitoring. These large-scale public sector IoT implementations create sustained demand for ruggedized, energy-efficient 5G chips designed for long-term outdoor deployment.

MARKET RESTRAINTS

High Power Consumption of 5G Modems Constraining Mass IoT Adoption

While 5G offers superior bandwidth and latency characteristics, the technology’s power requirements present significant challenges for battery-operated IoT devices. Current 5G modem implementations consume substantially more power than LTE-M or NB-IoT alternatives, limiting practicality for deployments requiring years of battery life. This power inefficiency affects adoption in asset tracking, agricultural monitoring, and other remote sensing applications where long intervals between maintenance are critical. Though chipmakers are developing low-power modes and advanced power management architectures, achieving parity with LTE power profiles while maintaining 5G performance remains an ongoing engineering challenge restricting certain market segments.

Complex Regulatory Compliance Increasing Time-to-Market for New Chip Designs

The global regulatory environment for 5G spectrum usage creates substantial barriers to IoT chipset development. Unlike previous cellular generations, 5G operates across numerous frequency bands (sub-6GHz and mmWave) with varying regional allocations and certification requirements. A single chipset intended for worldwide deployment must comply with dozens of different technical regulations regarding radio emissions, frequency use, and security protocols. This regulatory complexity extends development timelines and increases testing costs, particularly for smaller semiconductor firms without established compliance infrastructure. Recent geopolitical tensions have further fragmented the regulatory landscape, requiring manufacturers to develop region-specific variants of their products.

MARKET CHALLENGES

Semiconductor Supply Chain Vulnerabilities Disrupting Production Timelines

The 5G IoT chip market faces ongoing challenges from global semiconductor supply chain instability. Advanced nodes required for 5G modem integration (particularly 7nm and below) remain capacity-constrained at leading foundries, creating allocation challenges for fabless chip designers. The industry’s heavy reliance on a limited number of advanced packaging facilities further compounds supply risks. Recent geopolitical developments have introduced additional uncertainty regarding access to critical semiconductor manufacturing equipment and materials. These supply chain limitations create unpredictable lead times that complicate product roadmaps and constrain manufacturers’ ability to respond to sudden demand surges in key vertical markets.

Security Vulnerabilities in Heterogeneous IoT Ecosystems Creating Deployment Concerns

The distributed nature of 5G IoT implementations introduces significant cybersecurity challenges that chipmakers must address. Unlike traditional IT systems, IoT deployments incorporate numerous edge devices with varying security capabilities connected through potentially vulnerable networks. Recent analyses indicate that over 40% of IoT devices contain critical security flaws that could compromise entire networks. While 5G standards include enhanced security protocols compared to previous generations, their effective implementation relies on robust hardware-level security in endpoint chips. The semiconductor industry faces increasing pressure to incorporate hardware roots of trust, secure boot mechanisms, and hardware-based encryption accelerators—features that add complexity and cost to chip designs.

MARKET OPPORTUNITIES

Emergence of AI-Enabled Edge Computing Creating Demand for Intelligent 5G IoT Chips

The convergence of 5G connectivity with edge AI processing represents a transformative opportunity for the IoT chip market. Next-generation applications require localized decision-making capabilities to reduce latency and bandwidth requirements. Smart cameras for industrial quality control, autonomous vehicles, and augmented reality devices increasingly integrate AI acceleration alongside 5G modems. This trend is driving demand for heterogeneous chips that combine neural processing units (NPUs) with cellular connectivity in power-efficient packages. Leading chipmakers are responding with architectures that enable on-device machine learning while maintaining always-connected 5G capabilities, opening new markets at the intersection of connectivity and intelligence.

Enterprise Digital Transformation Initiatives Fueling Private 5G Network Deployments

The growing adoption of private 5G networks by industrial enterprises presents significant opportunities for specialized IoT chip solutions. Unlike public networks, private 5G implementations require tailored connectivity solutions that prioritize reliability, security, and deterministic performance. Manufacturing plants, ports, and mining operations are increasingly deploying private networks to support mission-critical IoT applications. This emerging market segment demands industrial-grade chipsets with support for network slicing, ultra-reliable low-latency communication (URLLC), and precise timing synchronization. Semiconductor vendors able to address these specialized requirements while meeting industrial certifications stand to gain substantial market share in this high-value segment.

5G IoT CHIP MARKET TRENDS

5G Network Expansion Fuels Demand for Advanced IoT Chips

The global expansion of 5G networks is revolutionizing the IoT chip market, with 5G IoT chip shipments expected to grow at a CAGR of over 35% between 2024 and 2030. The superior bandwidth, ultra-low latency, and massive device connectivity offered by 5G technology have created unprecedented opportunities for IoT applications across industries. Manufacturers are increasingly focusing on developing 7nm and 10nm process chips that offer optimal performance while maintaining energy efficiency for IoT edge devices. Recent innovations include integrated AI capabilities directly on IoT chips, enabling faster localized decision-making in smart applications from industrial automation to connected healthcare.

Other Trends

Industrial IoT Adoption Accelerates

Industries are rapidly deploying 5G-enabled IoT solutions for predictive maintenance, asset tracking, and process optimization. The industrial segment now accounts for nearly 30% of all 5G IoT chip demand. Factories implementing Industry 4.0 solutions particularly favor chips supporting URLLC (Ultra-Reliable Low-Latency Communications), which enables real-time control of machinery with latencies below 10ms. Meanwhile, the renewable energy sector is leveraging 5G IoT for smart grid management, with chipmakers developing specialized solutions that can withstand harsh environmental conditions.

Smart Cities Drive Heterogeneous Chip Demand

Urban digital transformation initiatives worldwide are creating diverse requirements for 5G IoT chips. While smart meters typically use economical 28nm chips, more advanced applications like autonomous traffic management systems require high-performance 7nm processors with integrated AI accelerators. The Asia-Pacific region leads in smart city deployments, accounting for nearly 50% of global smart city 5G IoT chip consumption. Chip manufacturers are responding with flexible system-on-chip (SoC) designs that can be customized for various municipal applications, from environmental monitoring to public safety systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Compete for Dominance in 5G IoT Chip Innovation

The global 5G IoT chip market exhibits a dynamic competitive landscape, dominated by established semiconductor manufacturers and emerging fabless players. This arena is characterized by rapid technological evolution, strategic partnerships, and intense R&D investments as companies vie for market share in this high-growth sector.

Qualcomm Technologies Inc. currently leads the market with approximately 35% revenue share in 2024, demonstrating technological prowess with its Snapdragon X series chipsets designed specifically for IoT applications. The company’s success stems from its early-mover advantage in 5G modems and strong relationships with smartphone manufacturers expanding into IoT solutions.

MediaTek and Hisilicon collectively hold about 28% market share, capitalizing on cost-competitive solutions for mid-range IoT devices. MediaTek’s recent Helio i series chips gained significant traction in smart home and industrial automation segments, while Hisilicon’s Balong chips power numerous connected devices in China’s expanding IoT ecosystem.

Smaller specialized players demonstrate remarkable agility in niche applications. Sequans Communications secured design wins with several European smart meter manufacturers, while Eigencomm made breakthroughs in antenna integration technologies for compact IoT devices. These innovators threaten incumbents by addressing specific pain points neglected by larger competitors.

The competitive intensity is escalating as traditional computing giants enter the fray. Intel leveraged its process technology advantage to launch 10nm IoT-focused SoCs, targeting industrial and automotive applications where its x86 architecture maintains influence. Meanwhile, UNISOC and ASR Microelectronics continue gaining ground in emerging markets through aggressive pricing strategies and customized solutions.

List of Key 5G IoT Chip Manufacturers Profiled

Qualcomm Incorporated (U.S.)

MediaTek Inc. (Taiwan)

Hisilicon (China)

Intel Corporation (U.S.)

UNISOC (China)

ASR Microelectronics Co., Ltd. (China)

Eigencomm (China)

Sequans Communications (France)

Segment Analysis:

By Type

7 nm Segment Dominates Due to High Performance and Energy Efficiency in 5G Connectivity

The market is segmented based on type into:

7 nm

10 nm

12 nm

Others

By Application

Industrial Applications Lead as 5G Chips Drive Smart Manufacturing and Automation

The market is segmented based on application into:

PC

Router/CPE

POS

Smart Meters

Industrial Application

Other

By End User

Telecom Sector Emerges as Key Adopter for 5G Network Infrastructure Deployment

The market is segmented based on end user into:

Telecommunication

Automotive

Healthcare

Consumer Electronics

Others

Regional Analysis: 5G IoT Chip Market

North America The North American 5G IoT chip market is driven by rapid advancements in connectivity infrastructure and strong investments from major tech firms. The U.S. remains a key player, accounting for over 60% of regional market share, primarily due to high 5G deployment rates and innovations from companies like Qualcomm and Intel. Industries such as smart manufacturing, automotive, and healthcare are accelerating demand for low-latency, high-speed IoT connectivity. However, regulatory complexities around spectrum allocation and security concerns pose challenges for large-scale IoT adoption. The rise of private 5G networks for industrial automation is expected to further fuel growth, supported by government initiatives like the National Spectrum Strategy.

Europe Europe’s 5G IoT chip market is characterized by strict data privacy regulations (e.g., GDPR) and a strong push for industrial digitization under initiatives like Industry 4.0. Germany and the U.K. lead in adoption, particularly in smart city and automotive applications. The EU’s focus on semiconductor sovereignty, including the Chips Act, is increasing local production capabilities to reduce dependency on imports. While sustainability and energy-efficient chips are prioritized, slower 5G rollouts in certain countries—due to bureaucratic hurdles—impede faster market expansion. Nonetheless, the demand for ultra-reliable IoT solutions in logistics and healthcare continues to grow, creating long-term opportunities.

Asia-Pacific Asia-Pacific dominates the global 5G IoT chip market, with China, Japan, and South Korea collectively contributing over 50% of worldwide shipments. China’s aggressive 5G rollout and government-backed IoT projects, such as smart city deployments, drive massive demand for cost-effective chips. Meanwhile, India’s expanding telecom infrastructure (e.g., BharatNet) and rising investments in edge computing present new growth avenues. While regional players like Huawei’s Hisilicon and MediaTek lead innovation, geopolitical tensions and supply chain dependencies on Western technology remain key challenges. The shift toward AI-enabled IoT chips for industrial automation and consumer electronics further strengthens the region’s market position.

South America South America’s 5G IoT chip market is nascent but growing, fueled by gradual 5G deployments in Brazil and Argentina. Limited telecom infrastructure and economic instability slow adoption compared to other regions, but sectors like agricultural IoT and smart energy management show promise. Local chip production is almost nonexistent, leaving the region reliant on imports, which inflates costs and delays implementation. However, partnerships with global semiconductor firms and pilot projects in urban centers indicate potential for mid-term growth, particularly as government policies begin prioritizing digital transformation.

Middle East & Africa The Middle East & Africa region is witnessing sporadic but strategic 5G IoT adoption, led by the UAE, Saudi Arabia, and South Africa. Telecom operators are investing heavily in smart city projects (e.g., NEOM in Saudi Arabia), creating demand for high-capacity IoT chips. Conversely, Africa’s market growth is constrained by underdeveloped 5G infrastructure and affordability barriers. Despite challenges, sectors like oil & gas digitization and remote monitoring in mining are driving niche demand. The lack of local semiconductor manufacturing increases reliance on imports, but regional collaborations and foreign investments signal gradual market maturation.

Report Scope

This market research report provides a comprehensive analysis of the global and regional 5G IoT Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global 5G IoT Chip market was valued at USD 1.2 billion in 2024 and is projected to reach USD 3.8 billion by 2032, growing at a CAGR of 15.6%.

Segmentation Analysis: Detailed breakdown by product type (7nm, 10nm, 12nm), application (PC, Router/CPE, Industrial IoT), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific currently holds 48% market share.

Competitive Landscape: Profiles of leading market participants including Qualcomm, MediaTek, Intel, and Hisilicon, covering their product portfolios and strategic initiatives.

Technology Trends & Innovation: Assessment of emerging 5G NR standards, AI integration in chipsets, and advanced fabrication techniques below 10nm.