#Roth IRA benefits

Text

Exploring Roth IRA Accounts: Tax-Advantaged Investing for Retirement

Written by Delvin

As you plan for your retirement, it’s crucial to consider different investment options that can help you grow your savings while enjoying tax advantages. One such option is the Roth Individual Retirement Account (IRA). In this blog post, we’ll explore the features, benefits, and considerations of Roth IRA accounts, empowering you to make informed decisions about your retirement…

View On WordPress

#After-tax contributions#Backdoor Roth IRA#dailyprompt#Estate planning with Roth IRA#Financial#Financial Literacy#Investment options#Retirement accounts#Retirement income#Retirement investment options#Retirement planning#Retirement savings#Retirement savings strategies#Retirement tax planning#Roth IRA#Roth IRA benefits#Roth IRA conversion#Roth IRA eligibility#Roth IRA vs. traditional IRA#Tax-advantaged investing#Tax-efficient savings#Tax-free growth#Tax-free withdrawals

1 note

·

View note

Text

How to Save for Retirement

Good news: There's a lot about retirement savings that you DO NOT have to thoroughly understand to make savvy investments. You don't have to be a math person or have a traditional job or have a "5 year plan".

1) Start saving as early as you can. The one financial advantage we have over the older generations is TIME, so USE IT. Starting early means making "free money," your interest earns interest that will be paid back to you. The amount you save in the early years is expected to double every decade, so the more years with an account, the more free money.

2) Start today if you haven't yet. I mean it. Even if it's only 50-100 / month. You will have an account earning free money in your name, and it's easy to add more funds later when the basics are already set up. If you don't have access to a 401(k) or similar, open an IRA (the Roth IRA kind is for those with a low income and a low tax payment in the springs). NOW is more important than which type of account.

3) Choose an "index fund" with a "target date" around the age you expect to retire. Index funds are basically a tiny sliver of the whole economy around you - stocks for companies large and small, bonds for the US government, real estate, international components. Index funds provide better returns for a lower fee than "actively managed" funds, where the professional's guess wrong more often than not. If you are investing in an index, or piece of the market, than the market can never leave you behind. Target dates mean more higher risk, higher reward stocks in the earliest years, and gradually adjusting to more stable and steady bonds as you near retirement and have less time to recoop a loss. If any of this sounds scary or complicated, this is the common and proven best way to invest over a lifetime.

4) If your employer offers a retirement match contribution (often 2% - 5% of your takehome pay), invest at least that much of your own pay, because again we love FREE MONEY.

5) Increase your retirement payments to yourself anytime life gets easier. Significant raise at work? Moved to a cheaper town? Paid off your car / house / student loans / day care years? Send some of that new monthly money straight into the retirement fund.

6) Your eventual goal is to save 15% of your annual income toward retirement. If this seems insane, start where you can, and aim to add an additional 1-2% with every new year.

7) "Set it and forget it." DO NOT TOUCH your retirement money. Don't even look at it. Maybe once / year if you are curious. The road of compound interest will include some downturns with the stock market is down. This is normal for everyone, but keeping that steady investment through highs & lows is the best strategy for longterm growth of your money.

7b) It is not a kindness to your children to pull money out of your retirement savings on their behalf. You'll lose that much money plus the years of "free money" accumulation plus some early withdrawal fees &/ weird tasks. This makes you more likely to become financially dependent on your kids during your retirement. Not a favor in the long run.

8 ) "If investing feels fun and exciting, then you are not investing, you are gambling." If you are intrigued by the idea of investing in particular companies or trying to time the market - cool. Take some money that wouldn't be disastrous to lose and try your luck - the odds are not in your favor. But your retirement plan must be slow and steady.

Source

#personal finance#financial awareness#financial literacy#retirement#investment#401k#roth ira#compound interest#retirement savings#retirement security#retirement strategies#retirement planning#npr#npr life kit#gambling#investing#benefits#stocks#bonds#stock market#index funds#time is on my side#do not touch#slow and steady

0 notes

Text

honestly being a generationally-poor, first generation accounting student is fucking wild

#like my professors will mention these accounts and things like i should know them#as if anyone has ever been able to save money in my family#like you think i know what a money market account is? what the actual fuck is a roth ira?#my mom once tried to explain retirement accounts to me and i cried#the only reason she knows about them is that she used to be a benefits manager#like how tf do i get any of this knowledge?#do i have to actually listen to finance bros or can i just figure it out through googling it?#god i hate this#k mumbles

1 note

·

View note

Text

{ MASTERPOST } Everything You Need to Know about Retirement and How to Retire

How to start saving for retirement

Dafuq Is a Retirement Plan and Why Do You Need One?

Procrastinating on Opening a Retirement Account? Here’s 3 Ways That’ll Fuck You Over.

Season 4, Episode 5: “401(k)s Aren’t Offered in My Industry. How Do I Save for Retirement if My Employer Won’t Help?”

How To Save for Retirement When You Make Less Than $30,000 a Year

Workplace Benefits and Other Cool Side Effects of Employment

Your School or Workplace Benefits Might Include Cool Free Stuff

Do NOT Make This Disastrous Beginner Mistake With Your Retirement Funds

The Financial Order of Operations: 10 Great Money Choices for Every Stage of Life

Advanced retirement moves

How to Painlessly Run the Gauntlet of a 401k Rollover

The Resignation Checklist: 25 Sneaky Ways To Bleed Your Employer Dry Before Quitting

Ask the Bitches: “Can I Quit With Unvested Funds? Or Am I Walking Away From Too Much Money?”

You Need to Talk to Your Parents About Their Retirement Plan

Season 4, Episode 8: “I’m Queer, and Want To Find an Affordable Place To Retire. How Do I Balance Safety With Cost of Living?”

How Dafuq Do Couples Share Their Money?

Ask the Bitches: “Do Women Need Different Financial Advice Than Men?”

From HYSAs to CDs, Here’s How to Level Up Your Financial Savings

Season 3, Episode 7: “I’m Finished With the Basic Shit. What Are the Advanced Financial Steps That Only Rich People Know?”

Speaking of advanced money moves, make sure you’re not funneling money to The Man through unnecessary account fees. Roll over your old retirement accounts FO’ FREE with our partner Capitalize:

Roll over your retirement fund with Capitalize

Investing for the long term

When Money in the Bank Is a Bad Thing: Understanding Inflation and Depreciation

Investing Deathmatch: Investing in the Stock Market vs. Just… Not

Investing Deathmatch: Traditional IRA vs. Roth IRA

Investing Deathmatch: Stocks vs. Bonds

Wait… Did I Just Lose All My Money Investing in the Stock Market?

Financial Independence, Retire Early (FIRE)

The FIRE Movement, Explained

Your Girl Is Officially Retiring at 35 Years Old

The Real Story of How I Paid off My Mortgage Early in 4 Years

My First 6 Months of Early Retirement Sucked Shit: What They Don’t Tell You about FIRE

Bitchtastic Book Review: Tanja Hester on Early Retirement, Privilege, and Her Book, Work Optional

Earning Her First $100K: An Interview with Tori Dunlap

We’ll periodically update this list with new links as we continue writing about retirement. And by “periodically,” we mean “when we remember to do it.” Maybe remind us, ok? It takes a village.

Contribute to our staff’s retirement!

Holy Justin Baldoni that’s a lot of lengthy, well-researched, thoughtful articles on the subject of retirement. It sure took a lot of time and effort to finely craft all them words over the last five years!

In case I’m not laying it on thick enough: running Bitches Get Riches is a labor of love, but it’s still labor. If our work helped you with your retirement goals, consider contributing to our Patreon to say thanks! You’ll get access to Patreon exclusives, giveaways, and monthly content polls! Join our Patreon or comment below to let us know if you would be interested in a BGR Discord server where you can chat with other Patrons and perhaps even the Bitches themselves! Our other Patrons are neat and we think you should hang out together.

Join the Bitches on Patreon

#retirement#retire#how to retire#retirement account#retirement fund#retirement funds#401k#403b#Roth IRA#Traditional IRA#investing#investors#investing in stocks#Capitalize#401k rollover#personal finance#money tips

404 notes

·

View notes

Text

@wikwalker hi sure yes anything to give me an excuse to procrastinate the post i should be writing right now. here are all teh drugs and how to manage them. you can trust me, a drug addict

first of all: https://www.erowid.org/ , erowid always

don't be afraid of drugs, if they're the right drugs, you should do them since they will be a blast regardless and overcoming fear is also good (but outside the scope here)

OK to do as much as you want:

alcohol - social benefit greatly outweighs health effects, no reason to avoid if predisposed to abuse since that'll happen sooner or later. what can i say? don't be a fucking dork. when you start drinking, really overdo it as much as possible without dying and get a few real nasty hangovers under your belt so you know how much is the right amount to drink.

weed - innocuous enough to be fine but will make you stupid in the long term. make sure to only buy from a real drug dealer and never some legal institution. cut it out when you're a "real adult". don't smoke weed and watch TV routinely, go out and do things so you naturally grow to hate it. good to go through this as early as possible to minimize the time you spend as a cringe weed enthusiast

i guess those are the only two.

ok to do infrequently (annually):

"lsd" - or whatever it is, probably not lsd, blah blah blah, if it works and is sold on blotter its fine and won't make you go nuts or whatever. opt for a better psychadelic imo. see psych rule at bottom of section

mushrooms - better than acid since you know what they are. rule of thumb is to always do more than you think you want. minimum 1/8oz. see psych rule at bottom of post

dmt - if you somehow have a dmt hookup you don't need to be reading any of this. lasts 10 minutes which leads to tendency to way overdo it, don't do this, my favorite webcomic artist is permanently crazy from exactly that. using a crack pipe is also not the uhhhh most dignifying-feeling thing to do either. it's harder than you think.

mdma - for use at electronic music event or rave. overuse causes brain lesions or something.

coke - wait until you're in your 20s, have maxed out your roth IRA for a couple of years in a row, and havent missed a car payment in a similar timeframe. better still if you've worked a very shitty low paying job and know the value of a dollar. if you still find yourself buying candy you're not ready. too expensive to be worth it to get hooked on. know that you are VERY ANNOYING to anyone who also isn't high. don't fuck around with the guy selling it to you. avoid discussing or thinking about business ideas. you can't afford to make it a habit + kinda turns you into a piece of shit after a while, but at least a very interesting one

ketamine - another sick drug that rules, but save it for a special occasion. don't try and go into the k-hole your first time

rule for psychedelics - you get one good strong trip a year and that's it, make it count, always opt for doing a bit more than a bit less. but don't make it a habit, otherwise you turn into a very stupid very annoying "hippy" style cliché and believe in ghosts, aliens, crap like that.

ok to try once

prescription opiates/benzodiazepine (xanax), valium, this kind of shit - worth trying so you can go "holy shit, this stuff is way way way too good to ever use responsibly" and then never do again. especially if you're white. for some reason we just can't handle this shit. if a doctor prescribes it to you, idk, that's your call to make.

ayhuasca - this is just dmt in a different form. do some other psychadelics a number of times before you do this. once you realize the whole "substantial visual hallucinations" thing is made up, its time. do exactly this:

-buy root online (legal). receive box of dirt

-boil dirt into "tea" (read erowid for exact recipe)

-take over-the-counter anti nausea medicine or anything that will give you a stronger stomach

-drink tea (its nasty as fuck, get it down quick)

-have someone bigger than you keep an eye on you for the next five hours.

-have the experience, which is absurdly intense, has no bearing to the real world, etc etc. don't be a bitch and throw up, if you do it'll only last an hour or so. again there is no way to provide a consistent description of the experience except that you will meet god. you only ever need to do this once and never again. trust me

peyote/salvia/etc - try em if you want, you'll never ever want to again afterwords. these are drugs for idiot teenagers too lame to get real drugs. imagine being very very sick from poison and utterly terrified at the same time. No good

whippets/nitrous oxide - just find a dentist that uses it and don't bother creating hundreds of pounds of trash on your floor for this crap that lasts ten seconds. you have to understand the extremely short timeframe coupled with the cost makes zero sense. go to a phish concert parking lot and do some people watching -- you do not want to be these people. only use is as a motivator to get routine dental exam. also if you somehow manage to make it a heavy habit your fucking legs stop working, no shit, but they start working again once you quit.

don't ever do

heroin/meth/pcp - is is truly a mystery why you should never do these 🙄

synthetic weed/k2/shit from the gas station - it is so funny that they sell this as "weed that won't pop you on a drug test". its not weed. it is some dubious chemical sprayed on yard waste. smoke it to have a terrible time and go nuts. only buy drugs from legitimate drug dealers!

kratom - anyone's guess as to why this is legal but it's heroin for pussies. its still heroin

dxm/cough syrup - do you ever wonder why it is exclusively teenagers robotripping? it's because it sucks ass. is like a cheesegrater on your brain in terms of health effects with repeated usage. you're better than this king

inhalants - these are at the bottom of the list for a reason. do not huff gas. don't huff paint. do not consume computer duster. not fun + fastest way to make yourself a complete, uh, (word i can't say anymore) and then dead

not listed

quaaludes- unavailable due to no longer being manufactured. these ruled apparantly

sincis2c - unavailable due to not existing, i just made this up

amphetamines - cannot provide objective take here. they're my albatross, lifelong (posted 4:55am natch)

442 notes

·

View notes

Note

meow?

meow (i have no idea what brought this on or what this means. but life is too temporary not to live it.) meow (look into opening a roth ira when saving for retirement, and you should start early to reap the best benefit.)

63 notes

·

View notes

Text

Femme Fatale Guide: How To Master Your Money & Tips On Financial Literacy

Understanding and taking control of your finances improves your quality of life in many ways. Making strides toward better financial literacy can save you a lot of stress, unnecessary fees and helps you play a more active role in taking control over this aspect of adulthood. Once you understand the game of money, saving, and investing, it becomes infinitely simpler to devise a plan to set yourself up for a more financially-free future. Here are some practical tips to keep your finances streamlined, secure, and systemized to help you gain more financial literacy and win in this area of life.

Overview:

Track Your Income & Expenses

Set Financial Goals & Realistic Limitations

Invest Higher-Quality Items To Save Later

Educate Yourself On Different Types of Banking & Investment Accounts

Establish Credit, But Know Yourself

Create An Emergency Fund

Leverage Credit Card Benefits

Understand The Power of A Roth IRA (or Backdoor Roth IRA) & HSA

Automate Whenever Possible

Get Familiar With Taxes & Write-offs

Stay Informed About Employer Benefits

Purchase Seasonally & With Discount Codes (When Available)

Protect Yourself

Read Books

Seek Expert Advice

TIPS ON MASTERING FINANCIAL LITERACY:

Track Your Income & Expenses: Always have a record of all of the money going in and out of your accounts. Use the tool on your banking account app(s) to confirm your monthly income and expenses. Tools like Mint also are great to track your spending to see where every dollar is going all in one place. Aside from personal use, for small business owners, Quickbooks is my favorite invoicing and expense-tracking option.

Set Financial Goals & Realistic Limitations: Once you know your exact monthly income, budget your essentials, savings, investments, and fun money accordingly. Make sure necessities like rent, food, health insurance, electricity, WiFi, toiletries, etc. are accounted for before anything else. Depending on your financial situation, experts (not me – I try to educate myself as best as I can, but am no expert!) recommend trying to save and invest between 15-30% of your pre-tax income. Give yourself the liberty to spend the rest (say 15-20%) of your income, so you don’t feel deprived and stay on track with your goals.

Invest Higher-Quality Items To Save Later: Initially purchasing a higher-quality item often cuts your overall expenses in a certain area over the long run. (Ex: Well-made clothing, shoes, furniture, kitchen appliances, coffee maker, hair dryer, etc.). If you invest upfront on an item you regularly use, there’s a lower chance that it will deteriorate, rip, break, or otherwise become unusable for the next few years. When you opt for the cheaper option, this practice might save you a few bucks in the short term, but you will probably end up having to replace it a few times over time and spend more in the long run. This tip might seem counterintuitive to some, but it truly does save you a lot of money (and frustration). However, I will place a caveat here and say that this advice comes from a place of privilege. Never purchase something you can’t afford. If you have the means, spend a bit more upfront - it is better for your future wallet, allows you to indulge in a better quality of life, and helps you let go of any scarcity mindset/financial limiting beliefs.

Educate Yourself On The Different Types of Banking & Investment Accounts: Know the differences between and the use purpose of different accounts: Checking, Savings, CDs, 401K, Roth IRA, HSA, etc. Always opt for a high-yield savings account option to help preserve your money’s value over time with rising living costs and inflation.

Establish Credit, But Know Yourself: Your credit score is like your adult report card. It’s essential for so many aspects of life, like renting or buying a home, insurance, cell phone plans, etc., so it’s important to start building your credit as early as you can. However, if you know you’re the type of person to overspend with a credit card, look into secured credit card options (you deposit the money that acts as a credit limit, so it’s like a debit card with credit-building benefits).

Create An Emergency Fund: Pay yourself first. Have between 3-12 months of expenses available in a high-yield savings account at all times. If you have a family or are self-employed, aim for 6-12 months of necessary savings to stay sane. Saving this amount of money takes time. Be patient, and cut back on frivolous expenses if needed for the short term.

Leverage Credit Card Benefits: If you have enough self-control, always use a credit card instead of a debit card – but spend in the same way you would as though the money is coming directly out of your bank account. This gives you additional flight and other purchasing perks, such as cashback and exclusive discounts. Using a credit card provides additional security, too.

Understand The Power of A Roth IRA (or Backdoor Roth IRA, depending on your income) & HSA: Compound interest is your best friend financially. Depending on your income, invest as much as you can into a Roth IRA account or set up a backdoor Roth IRA through your brokerage firm (I use Vanguard!). HSA (Health Saving Accounts) accounts offer so many benefits – they can serve as a tax write-off, lower your overall healthcare costs, and be leveraged to use as an additional retirement investment account, too (I use Fidelity).

Automate Whenever Possible: Automate a portion of your paycheck to savings and your investments, so you never see this money. Pay yourself first before spending (on anything but necessities).

Get Familiar With Taxes & Write-offs: This mainly applies to anyone self-employed or a small business owner (been in the game for 5 years!). However, this point can also potentially be beneficial for students who can leverage an education credit for tax purposes. Explore all of your options to see what write-offs are available in your specific situation. Understand how your income and expenses influence your tax bracket. Investing in a CPA can save you a considerable amount of money and all of your sanity if you’re not a salaried employee. Look over the standardized section C document, and speak with a professional to help maximize your write-off potential (legally and honestly, of course). My CPA is my lifeline!

Stay Informed About Employer Benefits: Always maximize your 401K match (whatever percentage that is at your company), any wellness perks (like a gym membership or massage credit), or any meals and car services credits for late nights/work trips.

Purchase Seasonally & With Discount Codes (When Available): Try to purchase items off-season when you can (e.g. purchase classic winter closet staples in the summer when they’re on sale). Utilize plug-ins like Honey or Cently on your browser to have discount codes for any site readily available.

Protect Yourself: Stay on top of fraud alerts. Freeze your credit bureau accounts if necessary.

Read Books: Educate yourself on saving, investing, budgeting, building a business, etc. See the ‘Finance’ section of my Femme Fatale Booklist for some recommendations. I also love Graham Stephan’s Youtube channel – his videos are highly useful and practical for beginners in this life arena!

Seek Expert Advice: Use licensed professionals (CPAs, brokerage firms, your bank, etc.) as a resource, too, for your personal goals.

This is a lot to take in, so try to implement one action item (or a few) at a time, so you can work towards your goals without getting overwhelmed. Also, for reference, I’m in the United States, so all of these tips are focused on how the system works in my country - if you know of any international equivalents, feel free to drop them in the comments to guide others.

Hope this helps xx

#life advice#finance#adulting#femme fatale#dark femininity#dark feminine energy#it girl#hypergamy#high value woman#divine feminine#high value mindset#hypergamous#the feminine urge#success mindset#productivity#spending habits#entreprenuership#level up#self improvement#ideal self#female power#female excellence#personal growth#investing#girl advice#that girl#femmefatalevibe

1K notes

·

View notes

Text

I see a disturbing number of people, mostly millennials, these days, who have significant incomes and are starting to amass significant savings, who have terrible financial management skills. People who live at home with parents and get a full time job can accumulate money really fast. A lot of people are letting huge amounts of money, like sometimes as much as $20,000 or more, accumulate in checking accounts where it is earning either no interest or negligible interest.

Because inflation is high (over 3% these days), you are effectively losing money when it sits there. Also you're allowing the bank to profit off it; it's lending your money out to other people, often at interest rates as high as 6-7% or more, and it's not paying you for it.

If you have more than maybe around $3000 dollars in an account, you want that money earning interest. Here are things you can do to earn more from your money:

Open a savings account at a higher yield. Go to a different bank if necessary. CIT Bank has rates around 5% these days.

Pay off high interest rate debt but not low-interest rate debt. If the interest rate is above about 7-8% definitely make it a priority to pay it off ASAP. If it is above 5% it is still better to pay it off than to sit on your money. If it is much below 5%, pay it off as slowly as possible (minimum payment only) because there are risk-free ways to earn more interest on your money.

If you don't need the money in the short-term, consider a CD (Certificate of Deposit) which offers a fixed interest rate over a certain time. Often you can get a slightly higher rate by tying your money up for 3 months or 6 months or sometimes even longer. These are good options if you have a specific expenditure in your future, like perhaps moving or buying a home, but you know it won't happen until after a certain date.

Open a brokerage account. Brokerage accounts allow you to buy and sell investments such as stocks, mutual funds, or bonds, which include CD's from banks as well as treasury and municipal bonds and corporate bonds. You get more options for buying CD's (i.e. you can compare many different banks side-by-side, buy CD with the best rate, and manage multiple CD's within a single interface.) Most brokerage accounts have no fees and typically no or very low minimum investments. There is no reason not to have one if you have a few thousand dollars.

In a brokerage account, buy a money market mutual fund. Look for one with no load and no transaction fee, a high yield, and a low expense ratio, and a fixed share price of $1 per share. My two favorite are SWVXX and SNSXX. SWVXX has a higher yield (about 5.19%) whereas SNSXX has a lower yield (just over 5%) but is non-taxable on state income taxes, so SNSXX is a better choice if you have a high state tax rate, otherwise SWVXX is better.

Consider opening a Roth IRA if you haven't, and then, if able, contribute the maximum amount each year. You are allowed to make a contribution that counts towards the previous year, up until the tax filing deadline of the current year. So for example today it is Mar. 14th, 2024, so you can open a Roth IRA today and contribute the max ($6,500) for the 2023 year and also the max ($7,000) for 2024, for a total of $13,500. The main advantage of a Roth IRA is that the money in them can grow tax-free. Roth IRA's benefit anyone able to have one (the richest people are not allowed to contribute to them) and are especially important for people who are self-employed, change jobs a lot, or never work full-time, so they don't have a consistent employee-provided retirement plan.

Consider investing in stocks. Stocks are riskier (in that their price changes, and you can lose money when investing in them), but tend to have a higher yield than savings and money market accounts and funds. The simplest way to buy stocks is to buy an ETF (exchange-traded-fund). I recommend buying one that follows the S&P 500 and has a low expense ratio like SPY or VOO. Whatever you buy, reinvest the dividends and let it grow, contribute a little money every year so are putting in money even in years the market is down. On average you get about a 10% return in the market but it is unpredictable and you will lose in some years, but that's okay, you're not retiring for many decades and the money will have grown a lot by then.

There are options regardless of your risk profile. It is throwing your money away to let a lot of money sit in a checking account. At a bare minimum, go for a high-yield savings account, CD, or better yet get a brokerage account, put it in high-yield money market funds like SWVXX, shop around for CD's or other bonds with the highest rates, and if you are able to tolerate some risk and want a higher return, consider putting some money in more aggressive investments like stocks.

I am 100% for tax reform and other reform to curb the extreme concentration of wealth in the hands of a few, but it's also important to take your financial situation into your own hands. Get financially comfortable. Get a stake in the US economy. Empower yourself so you can live better and help your family, friends, and the causes you care about.

12 notes

·

View notes

Text

Thank god it's Thursday (I have Friday off)

Got paid. 80-90% of my paycheck and my next paycheck will be thrown at my CC debt but after that it should be fine in that it will be less than half a paycheck (assuming no big bills).

I want to get back to where I was in the middle of lent. No drinking, no smoking, get off coffee again - I think the extra cortisol is just stressing me out more than I already am with little benefit.

I have worn so many hats this week. Sys admin with backup and restoring stuff, general IT with fixing our phones, took a phone call to talk to a customer about a new project they want (they liked the work I did for their coworker), database administrator stuff regarding ETL stuff and then general UI/scripting issue help with other people's projects. Today I should be pretty free to just focus on only 2 different projects which is nice.

Will be making my first ROTH IRA contribution today and some more into my dividend/investments. Think I'll be over $10 a month in dividends now, easy street here I come! Lol

10 notes

·

View notes

Text

Here are just two of the corporate giveaways hidden in the rushed, must-pass, end-of-year budget bill

Yesterday, Congress finally voted through the must-pass, end-of-year budget bill. As has become routine, this bill was stalled right until the final moment, so that Congressjerks could cram the 4,000-page, $1.7 trillion package with special favors for their donors, at the expense of the rest of the country.

This year’s budget package included a couple of especially egregious doozies, which were reported out for The American Prospect by Lee Harris (who covered a grotesque retirement giveaway for the ultra-rich) and Doraj Facundo (who covered a safety giveaway to Boeing and its lethal fleet of 737 Max airplanes).

Let’s start with the retirement scam. The budget bill includes Rep Richie Neal’s [DINO-MA] SECURE Act 2.0, which gives savers with retirement funds until age 75 to cash out their retirement savings — netting an extra three years of tax-free growth for the lucky, tiny minority with substantial retirement savings. This follows on Neal’s SECURE Act 1.0 of 2019, when the age was raised from 70.5 to 72.

The tax-exempt retirement savings account is a Carter-era bargain that replaced real pensions — ones that guaranteed that you wouldn’t starve or freeze to death when you retired — with accounts that let people gamble on the stock market, to be the suckers at Wall Street’s poker table:

https://pluralistic.net/2020/07/25/derechos-humanos/#are-there-no-poorhouses

The market-based gambler’s pension is a catastrophic failure. Half of Americans have no retirement savings. Of the half that have any savings, the vast majority have almost nothing saved:

https://www.federalreserve.gov/econres/scf/dataviz/scf/chart/#series:Retirement_Accounts;demographic:all;population:all;units:have

All in all, America has a $7 trillion retirement savings shortfall:

https://crr.bc.edu/wp-content/uploads/2019/10/IB_19-16.pdf

But for a tiny minority of the ultra-rich, tax-free savings accounts like ROTH IRAs are a means of avoiding even the paltry capital gains tax that you have to pay if you own things for a living, rather than doing things for a living. Propublica’s IRS Files revealed how ghouls like Peter Thiel avoided tax on billions in “passive income” by abusing tax-free savings accounts that were supposed to benefit the “middle class”:

https://pluralistic.net/2021/06/26/wax-rothful/#thiels-gambit

Meanwhile, Social Security is crumbling, thanks to a sustained attack on it by the business lobby and its friends in both parties. Progressive Dems had sought to amend SECURE Act 2.0 by inserting some clauses to shore up Social Security, and none of these were included in the final bill.

One of the fixes that died was the Savings Penalty Elimination Act, introduced by Senators Sherrod Brown [D-OH] and Rob Portman [R-OH]. This act would have tweaked the means-testing for Supplemental Security Income, which supports 8m low-income disabled adults and kids. Right now, you can’t collect SSI if you have $2k in the bank, a limit that hasn’t been adjusted for inflation since the 1980s (adjusted for inflation, $2k in 1980 is $7226.00 in 2022).

The $2k savings cap means that you have to be substantially below the poverty level to receive $585/month in SSI assistance — this being the only source of income for the majority of SSI recipients. Means-testing is a self-immolating fetish for corporate Dems and in retrospect, this betrayal seems inevitable:

https://pluralistic.net/2022/05/03/utopia-of-rules/#in-triplicate

(Notice how no one proposes means-testing billionaires when they get PPP loans or hundreds of millions in IRS “refunds” — like Trump, who paid substantially less tax than you did:)

https://www.cnbc.com/2022/12/21/trump-income-tax-returns-detailed-in-new-report-.html

And it was a betrayal: progressive Dems bargained with Neal and co not to publicly condemn SECURE Act 2.0 if they could get some concessions for the 8 million poorest disabled people in America. In the end, Neal rug-pulled them. Of course he did! This is Richie Fucking Neal, the best friend the Trump tax giveaway ever had:

https://pluralistic.net/2020/07/13/youre-still-the-product/#richie-neal

As with everything Neal touches, this screws poor people in multiple ways. First, it leaves the SSI cap intact. But it also creates a giant unfunded liability in the federal budget. Technically, there’s no reason this should lead to cuts. The US Treasury can’t run out of dollars, and giveaways to the rich are only mildly inflationary, since rich people put their money in the bank and mostly spend it on buying politicians, not goods.

But because of the delusion that currency producers like the US Treasury have the same constraints as currency users like you and me, Congress will need to come up with “Pay Fors” in future budgets to “make up for” the money they’re giving to rich people with SECURE Act 2.0. Dollars to toenail clippings, they’ll do that by hacking away at the tattered remains of the US social safety net.

Fear not, you don’t need to be a desperately poor disabled person or child to get fucked over by late additions to a 4,000 page must-pass bill! If you can afford to get on an airplane, Congress has something for you, too!

Remember when Boeing (the monopoly US airplane manufacturer that squandered $43b on stock buybacks and had to borrow $14b from the US public to survive the pandemic) told the FAA that it could self-certify its 737 Max airplanes, and then killed hundreds and hundreds of people with its defective planes?

https://pluralistic.net/2020/03/12/boeing-crashes/#boeing

The 737 Max was unsafe for many reasons, but one glaring factor was the fact that Boeing sold some of its core safety as “extras” — like they were downloadable content for your Fortnite character — leading to multiple crashes in which all lives were lost:

https://apnews.com/article/ethiopia-indonesia-accidents-ap-top-news-international-news-140576a8e9d4449eae646c8c479fdc3a

Boeing was forced to take the 737 Max out of service, but it eventually brought the plane back, “fixing” the problems by renaming the “737 Max” to the “737 8”:

https://pluralistic.net/2020/08/20/dubious-quantitative-residue/#737-8

Supposedly, Boeing has been diligently working on fixing the problems with its defective jets that can’t be addressed by a rebranding campaign. This wasn’t voluntary: the 2020 Aircraft Certification, Safety, and Accountability Act required Boeing — and every other manufacturer whose aircraft were certified by the FAA — to meet new minimum safety standards by December 27, 2022.

Every manufacturer met that deadline, except Boeing, and someone amended the budget bill to give the company three more years to meet these security standards. Critically, the new security measures, when they come, will be certified by an FAA that Republicans will control, thanks to the House changing hands.

https://prospect.org/infrastructure/transportation/government-spending-bill-waives-aircraft-safety-deadline/

Boeing is slated to ship 1,000 new 737 Maxes, which will fetch $50b for the company. Many of these planes will fly directly over my house, which is on the approach path for Burbank airport. Southwest Air flies dozens of 737 Maxes right over my roof every single day.

As Facundo points out, the FAA can ill afford any more hits to its credibility. It was once the case that if the FAA certified an aircraft, every other country in the world would waive any further certification, so trusting were they of the FAA’s judgment. That is no longer the case: today, the European Aviation Safety Agency does its own aircraft testing, holding jets that enter EU airspace to a higher standard than the FAA does for US planes.

It’s just another reminder that the US doesn’t have “corporate criminals” because the US doesn’t have any meaningful enforcement for corporate crimes. In America, we love our companies like we love our billionaires: too big to fail and too big to jail:

https://pluralistic.net/2021/10/12/no-criminals-no-crimes/#get-out-of-jail-free-card

Image:

Ryan Lee (modified)

https://www.flickr.com/photos/190784293@N05/50862532686

CC BY 2.0

https://creativecommons.org/licenses/by/2.0/

Henry Wadey (modified)

https://commons.wikimedia.org/wiki/File:Flames_%2858765896%29.jpeg

CC BY 3.0

https://creativecommons.org/licenses/by/3.0/deed.en

[Image ID: A living room scene, featuring a sofa in the background and a sofa in the foreground. A man's hand reaches into the frame to lift up the corner of the sofa. A broom enters the frame to sweep a pile of dirt under the rug. Mixed in with the dirt are a crashed WWI biplane with Southwest Airlines livery, and an old lady in a rocking chair.]

#pluralistic#secure 2.0#ssi#means testing#irsleaks#fidelity#vanguard#regulatory capture#faa#retirement crisis#retirement#finance#social security#pensions#corruption#congress#aviation#boeing#737 max#must-pass#irs files

83 notes

·

View notes

Text

retirement 101: a very basic guide.

This is instructions without explanations to keep it short. Think of this as a recipe; if you are an expert cook you don't need a recipe, if you are a good cook you can improvise around a recipe. if you are a novice, just follow the recipe to get a decent result.

1) If your employer offers a 401k/403b match, *take advantage of it*. Even if you need the money in the short term, this is a good deal - they are giving you extra money even after you pay an early-withdrawal penalty. Estimated spoon cost: 1 Certainty of advice: 100%. do this.

2) if you have credit card or other bad debt that you don't pay off every month, pay it down as fast as you can. if you have multiple debts, pay down the highest interest rate first. it is okay to have minimal savings if you're paying down a credit card - you can always pull money back out of the card. Estimated spoon cost: 1 Certainty of advice: 90%. Definitely pay off your bad debt, but maybe have an emergency fund first if you feel the need.

2a) if you don't have a credit card or if all of your bad debts are paid off, save in checking or easy-access savings until you have 3 months of expenses saved up. This is your emergency fund and your monthly expense fund. Estimated spoon cost: 0 Certainty of advice: 100%. do this.

3) if you have at least $3000 more than 3 months of savings, open an account at Vanguard (https://personal1.vanguard.com/mmx-move-money/funding-method). Pick Roth IRA for your first account type, and put $3000 - $6500 in it to start, as your available cash allows. This money will be mostly unavailable until you retire. The benefit is that you don't get taxed on money you get from the investments. You can put another $6500 in it every year. You'll need to select some investments. See below for instructions on that. Estimated spoon cost: 1 Certainty of advice: 90%. There are *some* other retirement companies that don't suck, you might want to use them (Fidelity and Charles Schwab are not terrible, for example)

3a) if you have pre-existing 401ks from prior employers or whatever, roll them into Vanguard IRA. If they are Traditional (not Roth) 401ks you will need to open a Traditional IRA at Vanguard to roll into. This process will almost certainly require calling the 401k custodian repeatedly, and having them send the money to either you or Vanguard. Estimated spoon cost: 8 Certainty of advice: 50%. Leaving the money where it is costs ongoing spoons of remembering and managing, and employer 401ks are often suboptimal in terms of fees and investment choices. But if it's a decent custodian and management is nbd, leaving it is okay too.

4) If you have more available money than that, open a Brokerage account at vanguard. This is an *uninsured* and *unsheltered* account - you will be taxed on it and there is the potential for it to be lost. You'll need to select some investments. See below for instructions on that. Certainty of advice: 90%. It is possible to lose money this way, but the upside outweighs the downside.

Selecting investments:

$3000 - $6000: just leave it in the money market default account. Estimated spoon cost: 0

$6000 - $12000: put $5000 in VTSAX and select VTSAX for future contributions. Estimated spoon cost: 1

More: put around 80% in VTSAX and around 20% in VBTLX and select that for future contributions. Estimated spoon cost: 1

Certainty of advice: 70%. These are decent choices but may not match your appetite for risk and/or retirement horizon.

5) continuing work: contribute up to $6500/year into your IRA. contribute as much as you can afford to lock up into your company 401k, up to $22500/year. If your bank account grows much past 3 months while doing those things, move some into your brokerage account.

7 notes

·

View notes

Text

The Pros and Cons of Different Types of Retirement Plans

The Pros and Cons of Different Types of Retirement Plans

https://mattdixongreenvillesc.co/the-pros-and-cons-of-different-types-of-retirement-plans/

Retirement planning is essential with financial planning, and choosing the right retirement plan can significantly impact your future financial security. Several types of retirement plans are available, each with its own advantages and disadvantages. Let’s explore the pros and cons of different retirement plans to help you choose the right one.

Traditional IRA

This is an retirement account that allows you to make tax-deductible contributions, and the earnings grow tax-deferred until you withdraw them in retirement. One of the advantages of a traditional IRA is that it can reduce your taxable income. However, withdrawals are taxed at your current income tax rate, which can be a disadvantage if your tax rate is higher in retirement.

Roth IRA

This is similar to a traditional IRA, but the contributions are made with after-tax dollars. The earnings grow tax-free, and withdrawals are tax-free in retirement. One of the advantages of a Roth IRA is that you won’t pay taxes on your withdrawals in retirement, which can be a significant benefit if your tax rate is higher. However, you won’t receive a tax deduction for your contributions.

401(k) Plan

A 401(k) plan is offered by many employers. Contributions are made with pre-tax dollars, and the earnings grow tax-deferred until you withdraw them. One of the advantages of a 401(k) plan is that many employers offer matching contributions, which can help you save more for retirement. There are limits on how much you can add each year, and withdrawals are taxed at your current income tax rate.

Roth 401(k) Plan

A Roth 401(k) plan is similar to a traditional 401(k) plan, but the contributions are made with after-tax dollars. The earnings grow tax-free, and withdrawals are tax-free in retirement. One of the advantages of a Roth 401(k) plan is that you won’t pay taxes on your withdrawals in retirement, which can be a significant benefit if your tax rate is higher in retirement. However, not all employers offer a Roth 401(k) plan.

Pension Plan

A pension plan is a retirement plan offered by some employers. With a pension plan, your employer contributes to the plan, and you’re guaranteed a specific income in retirement. One of the advantages of a pension plan is there is no worry about managing your investments or market fluctuations. However, not all employers offer pension plans, and you may have limited control over your retirement income.

Several types of retirement plans are available, each with its own advantages and disadvantages. Traditional and Roth IRAs offer tax advantages, while 401(k) and pension plans provide employer contributions and guaranteed income. It’s essential to consider your current and future tax situation, your retirement income needs, and your employer’s retirement plan options when choosing the right retirement plan for you.

The post The Pros and Cons of Different Types of Retirement Plans first appeared on Matt Dixon | Professional Overview, Philanthropy.

via Matt Dixon | Professional Overview, Philanthropy https://mattdixongreenvillesc.co

2 notes

·

View notes

Text

The Benefits of a Roth IRA Savings

The Benefits of a Roth IRA Savings

http://brianrayhack.com/the-benefits-of-a-roth-ira-savings/

A Roth IRA is a type of retirement account that allows people to withdraw tax-free money from their accounts. A Roth has various benefits, such as its ability to grow tax-free.

Roth IRAs are versatile and can provide people with tax-efficient retirement savings. If you are not currently a Roth IRA owner, here are some reasons why starting one is a good idea.

You get tax-free growth

A Roth IRA allows people to avoid taxes on the money they invest. This eliminates the worry of having to report investment earnings on their taxes. Unlike other retirement accounts, Roth IRAs do not have to be held in a bank or other financial institution.

You can take tax-free withdrawals in retirement

Individuals at least 59 1/2 years old and who have owned a Roth account for at least five years can withdraw without paying taxes or penalties.

In retirement, your income will not be affected by a lump-sum withdrawal. This benefit is important because your income will affect your taxes, including those related to Social Security and Medicare Part D premiums.

You decide when, if, and how to take withdrawals

A Roth IRA does not have a minimum distribution requirement. It allows people to withdraw early without paying taxes or penalties on their contributed money. However, if you are under 5912, you may be subject to penalties and taxes on the earnings that you withdraw. It’s generally better to contribute to a Roth IRA and let its returns work for you rather than take distributions from it.

You may qualify for additional tax credits

Individuals who contribute to a retirement fund or a type of retirement account such as a Roth IRA are eligible for the Credit for Savings Contribution. The amount that you’ve contributed and your adjusted gross income are the factors that determine whether or not you can qualify.

Your beneficiaries won’t be taxed

Your beneficiaries will not have to take distributions from your Roth IRA as long as the account has been open for at least five years. This means that they won’t have to pay taxes on the money they withdraw. Please contact your financial advisor if you have any questions about this process.

Choose from a wide variety of investment options

Roth IRAs also provide an extensive selection of investment options. For instance, you can choose from a variety of low-cost exchange-traded funds and mutual funds offered by companies such as The Vanguard Group.

You should keep in mind that you can still contribute to a Roth IRA for as long as you like. Even if you need to take distributions, you’re still contributing to this type of retirement account to ensure that you have enough money for retirement.

The post The Benefits of a Roth IRA Savings first appeared on Brian Rayhack | Professional Overview.

https://ifttt.com/images/no_image_card.png

via Brian Rayhack | Professional Overview http://brianrayhack.com

June 13, 2023 at 10:52PM

2 notes

·

View notes

Text

The Advantages of Planning for Retirement

Many individuals begin their retirement planning by saving and making investments. Most employers often provide these plans. They might be anything from pensions to 401(K) plans. Additionally, you have the choice of combining these programs. To make the most of these alternatives, discussing them with your employer is crucial.

A professional financial planner might aid your retirement planning. These experts will examine your current assets, income, and projected living expenses. They can assist you in creating a plan to satisfy your financial needs and avert upcoming economic issues. Up to one-third of Americans who are working age are thought to face financial hardship. Financial stress is one of the leading causes of sleep loss and a factor that might affect your quality of life. But you can lessen many of the critical financial stress caused by developing a retirement plan.

Planning for retirement has advantages that go beyond improving your financial stability. You should consider using about 80% of your working income in retirement if you are a full-time worker. For instance, a worker earning $50,000 yearly must have around $40k saved up for retirement. By setting up a retirement savings plan, you can prepare ahead of time and ensure that your family has enough money to meet their needs. You may feel more at ease as a result. It can benefit your kids as well. Children of retirees frequently worry about their parent's financial stability.

Early purchases of long-term care insurance are frequently more affordable. The costs for these insurance policies might be decreased by two to four percent annually by buying them when you are younger. However, waiting until retirement could result in higher rates and denial of coverage. The price of nursing home care may be covered in part by long-term care insurance. Long-term care insurance is crucial for future planning because sudden medical expenses could eliminate your retirement funds.

Planning for retirement might help you reduce taxes in addition to investing for the future. Diversifying your assets among several types of accounts is best because tax laws are subject to change. You may pay more taxes than you would otherwise if you have one tax-deferred account. A mix of standard and Roth IRA accounts might be the best choice for your purposes.

Your employer may provide one of several retirement savings options. Some employers offer matching funds. The 403(b) plan is another preferred option. Payroll deductions can be used to set up these programs automatically. With these programs, taxes won't be applied to your savings until you take them out. So you'll be able to maximize your benefits if your company matches your contributions.

The ability to save more for retirement is crucial for firms and people. Employees are more likely to stay with the organization if they are prepared for retirement. In addition, employer-sponsored retirement plans benefit your company by luring in fresh talent. Without these programs, workers could continue working until retirement for payment rather than contributing new ideas.

Even though self-employed people may not have access to this or PPFs, they can still benefit from retirement planning. You can make plans for the future and begin saving and investing as soon as you've evaluated your family's needs and your income flow. In addition, many businesses now provide insurance vehicles as retirement benefits.

Stress reduction is also another gain of retirement preparation. With a retirement funds, you can maintain discipline and stay on track with your retirement savings objectives. It is easier to get sidetracked with a project and bear sight of your dreams. You'll have a higher chance of achieving your objective and taking advantage of your golden years if you have a solid plan to keep you motivated.

7 notes

·

View notes

Photo

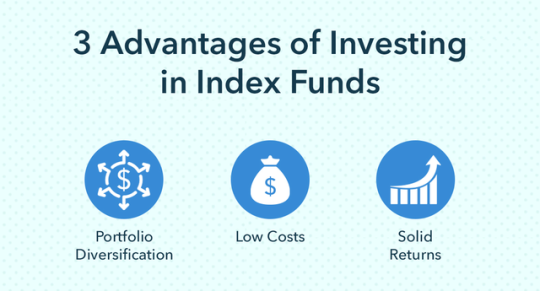

Fundamentals of investing:

What’s the REAL Rate of Return on the Stock Market?

Do NOT Make This Disastrous Beginner Mistake With Your Retirement Funds

The Dark Magic of Financial Horcruxes: How and Why to Diversify Your Assets

Dafuq Is Interest? And How Does It Work for the Forces of Darkness?

Booms, Busts, Bubbles, and Beanie Babies: How Economic Cycles Work

When Money in the Bank Is a Bad Thing: Understanding Inflation and Depreciation

Investing Deathmatch series:

Investing Deathmatch: Managed Funds vs. Index Funds

Investing Deathmatch: Traditional IRA vs. Roth IRA

Investing Deathmatch: Investing in the Stock Market vs. Just… Not

Investing Deathmatch: Stocks vs. Bonds

Investing Deathmatch: Timing the Market vs. Time IN the Market

Investing Deathmatch: Paying off Debt vs. Investing in the Stock Market

Now that we’ve covered the basics, are you ready to invest but don’t know where to begin? We recommend starting small with micro-investing through our partner Acorns. They’ll round up your purchases to the nearest dollar and invest the change in a nicely diversified portfolio of stocks, bonds, and ETFs. Easy as eating pancakes:

Start saving small with Acorns

Alternative investments:

Bullshit Reasons Not to Buy a House: Refuted

Investing in Cryptocurrency is Bad and Stupid

So I Got Chickens, Part 1: Return on Investment

Twelve Reasons Senior Pets Are an Awesome Investment

How To Save for Retirement When You Make Less Than $30,000 a Year

Understanding the stock market:

Ask the Bitches Pandemic Lightning Round: “Did Congress Really Give $1.5 Trillion to Wall Street?”

Season 3, Episode 2: “I Inherited Money. Should I Pay Off Debt, Invest It, or Blow It All on a Car?”

Money Is Fake and GameStop Is King: What Happened When Reddit and a Meme Stock Tanked Hedge Funds

Season 3, Episode 7: “I’m Finished With the Basic Shit. What Are the Advanced Financial Steps That Only Rich People Know?”

Retirement plans:

Dafuq Is a Retirement Plan and Why Do You Need One?

Procrastinating on Opening a Retirement Account? Here’s 3 Ways That’ll Fuck You Over

How to Painlessly Run the Gauntlet of a 401k Rollover

Ask the Bitches: “Can I Quit With Unvested Funds? Or Am I Walking Away From Too Much Money?”

Workplace Benefits and Other Cool Side Effects of Employment

You Need to Talk to Your Parents About Their Retirement Plan

Got a retirement plan already? How about three or four? Have you been leaving a trail of abandoned 401(k)s behind you at every employer you quit? Did we just become best friends? Because that was literally my story until recently. Our partner Capitalize will help you quickly and painlessly get through a 401(k) rollover:

Roll over your retirement fund with Capitalize

Recessions:

Season 1, Episode 12: “Should I Believe the Fear-Mongering about Another Recession?”

There’s a Storm a’Comin’: What We Know About the Next Recession

Ask the Bitches: How Do I Prepare for a Recession?

A Brief History of the 2008 Crash and Recession: We Were All So Fucked

Ask the Bitches Pandemic Lightning Round: “Is This the Right Time To Start Investing?”

1K notes

·

View notes

Text

everything wonderful 19 nov 2022

silky hair

clearest skin of my life

sticking to my moisturizing routine and you can tell

great routine with my eating schedule

consistent hdryation

better at getting to bed earlier

music sounds good again

2 (!) job offers, both at +62k$ per year, both with full benefits and amazing retirement plans

let go of my embarrassment of not having lots of friends

i love my apartment

i love my neighborhood

peace with my dad and sister

on my 4th day of anti depressants

maxed my roth ira this year

expecting student loan refunds

2 notes

·

View notes

Last Seen Blogs

simonsquared

Welcome!

freddie-fetish

Stardust

eetherealgoddess

✩ℯℯ𝓉𝒽ℯ𝓇ℯ𝒶𝓁✩

pabrikhama

PABRIK OBAT HAMA JAMUR TIRAM

desvaneiosby4j

By y4¿