#SBI Mutual Fund

Text

Which Loan is Best, FD, Gold Loan, Mutual Fund, Personal Loan

What is Loan

Some Types of Loans

FD (Fixed Deposit) Loan

You can take a loan against bank FD without breaking it. In this way, along with the benefit of maintaining the savings deposited in the bank, one also gets the necessary cash.

The interest rates (12–15%) applicable on FD loans are also lower than personal loans. This loan is also easily available immediately. Also, there is no need to submit many documents to the bank for this. Savings also remain intact along with debt.

Gold Loan

Gold loans have become attractive these days as gold prices have reached Rs 75,000 per 10 grams. Now you will get more loan than before on mortgaging jewellery.

READ MORE>>>>

#which loan is best#Which loan is best in india#Which Bank is best for personal loan with low interest#Which loan is best for bad credit#FD LOAN#Personal Loan#Gold Loan#Mutual Fund#HDFC Personal Loan#Personal loan rate of interest#Personal loan calculator#interest rate#Fd loan sbi#Gold Loan interest rates#Gold loan Calculator#Gold Loan SBI#Mutual fund calculator#Mutual funds India#SBI Mutual Fund#Mutual fund investment#4 types of mutual funds#Mutual Fund Sahi Hai#HDFC Mutual Fund#Mutual Fund investment Plan#SBI Gold Loan interest rate#Gold loan per gram#Gold loan EMI calculator#Gold loan near me#IIFL gold loan#Fd loan calculator

0 notes

Text

Shape your financial Goals with SBI Mutual Fund's Investment Tools & Calculators. These tools do not just help in setting up a financial goal, but also offer potential solutions on how to meet your goals.

1 note

·

View note

Text

বেষ্ট এস বি আই মিউচুয়াল ফান্ড ২০২৩। স্টেট ব্যাঙ্ক অফ ইন্ডিয়া নিফটি ইনডেক্স ফান্ড ২০২৩

এস বি আই বেষ্ট মিউচুয়াল ফান্ড:- বন্ধুরা আজকের এই পোস্টটিতে আমরা এসবিআই অর্থাৎ স্টেট ব্যাঙ্ক অফ ইন্ডিয়া এর একটি অত্যন্ত লাভজনক মিউচুয়াল ফান্ড প্ল্যান সম্বন্ধে জানব। যেখানে আপনার মান্থলি ইনকা��� এর পাশাপাশি আপনার মূল ইনভেস্টমেন্টের সাথেও হাই ইন্টারেস্ট যুক্ত হবে। যেটি মূলত পোস্ট অফিস এবং এলআইসি এর মান্থলি ইনকাম স্কিম গুলির ক্ষেত্রে হয় না।

তো বন্ধুরা এর আগে আমরা এলআইসি অর্থাৎ ভারতীয় জীবন বীমা…

View On WordPress

0 notes

Text

Best Mutual Funds, Online Investment Platform, Certified Financial Advisor | Sigfyn

https://www.sigfyn.com/

Get Best Mutual Fund Advisory at Sigfyn, we are best AI-powered platforms that provides personalized and holistic financial advisory to grow wealth by SIP. Invest in best mutual funds portfolios such SBI, HDFC, ICICI Prudential, Nippon India curated by expert-built algorithms.

#Best Mutual Funds#Online Investment Platform#Certified Financial Advisor#Financial Advisors#Mutual Funds#SBI Mutual Funds#HDFC Mutual Funds#ICICI Prudential Mutual Funds#Nippon India Mutual Funds#Sigfyn

4 notes

·

View notes

Text

#upcoming ipo#Sbi nifty 500 index fund hindi review#Sbi nifty 500 index fund nav#Sbi nifty 500 index fund hindi price#nfo#nfo mutual fund

0 notes

Text

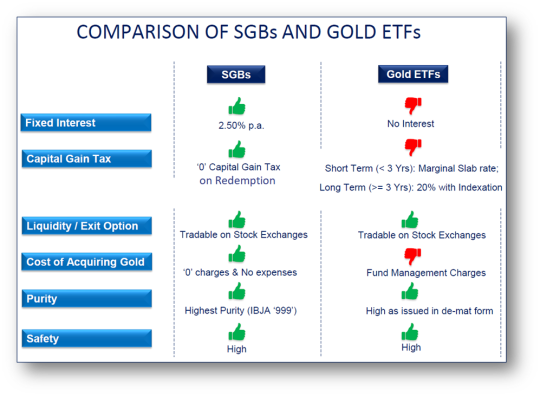

Sovereign Gold Bond vs. Gold ETF: A Comprehensive Comparison for Smart Investors

Over the last few years, the concept of digital gold has arrived in a big way. It started off with gold ETFs and then came the highly popular Sovereign Gold Bond scheme. There are also other digital gold holding vehicles like international gold funds, gold futures and digital gold. In this blog, the focus would largely be on understanding the relative merits and demerits of the sovereign gold bond vs gold ETF debate, and which is more suitable and under what circumstances. Also, a comparison of gold ETF vs SGB is provided on parameters like liquidity, flexibility, charges and tax implications.

What are Sovereign Gold Bonds (SGB) all about?

SGBs or Sovereign Gold Bonds have been around in India since Nov-2015 and have been gradually gaining in heft. These SGBs are central government-backed bonds, denominated in grams of gold. The underlying holding in grams of gold is guaranteed by the central government. In addition, these sovereign gold bonds also bear an interest of 2.50% annually on the issue price, which is paid semi-annually to the investor. Investors also get an upfront discount of Rs. 50/- per gram if the payment mode is digital. SGBs are also advantageous as they do not have the hassles like storing gold, making charges, risk of loss etc.

What really stands out about the SGB is the sovereign guarantee and that the returns are pegged to the price of gold. What the government guarantees is the payment of interest at 2.50% per annum and the holding of gold in grams. Considering that gold has generally given positive returns over longer periods of time, it makes investment in SGBs relatively secure and attractive too.

The SGBs can be held either in physical form or in demat form, as part of the demat account.

Gold ETFs (Exchange Traded Funds)

Unlike SGBs that are issued by the central government, gold ETFs are issued by the mutual fund houses registered with SEBI. They are issued in the form of gold units pegged as equivalent to a certain weight in gold expressed in grams. Gold ETFs are typically closed-ended in that once the NFO period is over, the fund does not offer any purchase or sale of units. However, being Exchange Traded Funds, they are mandatorily listed on the stock exchanges and investors wanting to buy or sell gold ETFs can do so using their existing demat account and trading account.

Gold ETFs are very liquid and hence, entry & exit is hardly a problem without any price damage. You can trade in gold ETFs just as you trade in stocks. It must be noted here that gold ETF issuing mutual funds are required to maintain physical gold equivalent to the units sold with a gold custodian bank as a backing.

Sovereign Gold Bond VS Gold ETF

Let's compare the sovereign gold bonds and the gold ETFs on a variety of parameters like returns, risk, flexibility, liquidity, taxation, etc. This sovereign gold bond vs gold ETF comparison will allow investors to make the best choice.

Here are the highlights of the gold ETF vs SGB debate.

1. How do SGBs and Gold ETFs compare in returns?

Remember, both SGBs and gold ETFs are linked to the price of gold. If the price of gold goes up, then the capital appreciation will benefit the SGB and also the gold ETFs. The difference lies in the interest paid. For instance, SGBs pay an additional assured interest of 2.50% per annum, but such assured returns do not exist in gold ETFs.

2. How do SGBs and Gold ETFs compare in risk?

One can argue that since both are backed by gold, there is no asset risk; however, there is a difference.

Even though SGBs do not have physical gold backing, the returns on these bonds are pegged to gold prices. And they have an explicit guarantee by the central government regarding the gold holding and the interest payable. In the case of gold ETFs, there is no explicit guarantee (sovereign or otherwise) but they do have the physical gold with the gold custodian bank.

3. How do SGBs and Gold ETFs compare in taxation?

Gold ETFs are treated as non-equity assets and hence the capital gains, if any, would be treated as short-term gains if held for less than 3 years and taxed at the marginal tax rate applicable. If the gold ETFs are held for more than 3 years, they are long-term capital gains and they attract tax at 20% with the benefit of indexation.

In the case of SGBs, the method of taxation is the same, with just one critical difference. If the SGBs are held till redemption, then any capital gains on the SGBs are fully tax-free in the hands of the investor. However, interest on gold bonds is fully taxable.

4. How do SGBs and Gold ETFs compare in costs?

Sovereign gold bonds don’t have any recurring cost of ownership. Gold ETFs on the other hand, have annual charges, including brokerage and expense ratio ranging from 0.50 – 1.00%. The costing of SGBs is a lot more transparent than Gold ETFs.

5. How do SGBs and Gold ETFs compare in liquidity?

Gold ETFs can be bought and sold in the secondary market using your existing trading and demat account with your stock broker. SGBs can be bought at the new issue period, which can be several times during the fiscal year. Outside that, SGBs are listed on the stock exchange, but the liquidity is limited.

Let’s look at the table below to quickly review the gold ETF vs SGB debate

To sum up the sovereign gold bond vs gold ETF debate, both are digital modes of holding gold and are linked to gold prices.

Among 6 key parameters viz. fixed interest, taxation, liquidity, costing, purity and safety, SGB stands out across all. On the other hand, Gold ETFs are highly liquid and do not have a maximum investment limit, allowing investors to buy as much as they want while in case of SGBs maximum investment limit for individual investors is 4kg in a Financial Year

Eventually, investors need to take a call on the gold ETF vs SGB choice based on their financial goals & risk profile; and returns, risk, liquidity, taxation, & convenience the products have to offer.

Source URL: https://www.sbisecurities.in/blog/sovereign-gold-bond-vs-gold-etf

0 notes

Video

youtube

Best SBI Mutual Fund for Lumpsum Investment 2024

0 notes

Text

#best online coaching for ras#best test series for ras#Daily Current Affairs Capsules 28th December 2023#Daily Current Affairs Capsules 28th December#RBI permits ICICI Pru Mutual Fund to acquire 10% stake in Federal#RBL Bank#SBI#HDFC Bank will need to maintain higher capital from FY25#says RBI#RBI flags concentration risk among govt-NBFCs#RBI approves IDFC-IDFC First Bank merger#Actor-Politician Vijayakanth Dies At 71#Japan lifts operational ban on world's biggest nuclear plant#India Makes Its 1st-Ever Rupee Payment For Crude Oil Purchase From UAE#RBI Unveils Forex Correspondent Scheme to Enhance Foreign Exchange Services#Incident Of Ammonia Gas Leakage Reported#Reliance Jio working on 'Bharat GPT' with IIT-Bombay#The Hindu Newspaper Analysis#Current affairs 2024#Current affairs 2023#Daily Current Affairs Capsules#Weekly Current Affairs 2023#Daily Current Affairs Class 24#Daily Current Affairs#Current affairs#Current Affairs#Today Current Affairs#Latest Current Affairs 2023#Daily Current Affairs Capsule#Current Affairs Capsule

0 notes

Text

Is SBI a Safe Bet for Long-Term Investment? Here's What the Experts Say

To make informed decisions, investing in the stock market necessitates careful consideration and analysis. State Bank of India (SBI), being quite possibly of the biggest bank in India, frequently grabs the eye of financial backers looking for long haul speculation open doors. Be that as it may

Read More

0 notes

Link

SIP Calculator: Caculate your SIP Returns with this SIP Calculator. You can calculate Mutual funds SIP returns and Stock Market SIP Return with this SIP Calculator.

#SIP Calculator#SIP Calculate#SIP#systematic investment plan#Mutual Funds#SIP Return Calculator#SBI SIP Calculator#SBI MF SIP Calculator

0 notes

Video

youtube

SBI Mutual Fund Launched 3 TM Funds SBI CRISIL IBX Gilt Index - June 203...

0 notes

Text

Sbi Mutual Fund क्या है ?

SBI Mutual Fund, एसेट मैनेजमेंट कंपनी और भारत के सबसे बड़े पब्लिक सेक्टर के बैंक भारतीय स्टेट बैंक द्वारा संचालित एक प्रमुख फंड हाउस है।

sbi mutual fund

SBI म्यूचुअल फंड योजनाओं में निवेश करने के सबसे लोकप्रिय तरीकों में से एक सिस्टेमेटिक इंवेस्टमेंट प्लान (SIP) है। SIP के जरिए आप SBI में निवेश कर सकते हैं। जिन इन्वेस्टर के पास काम राशि है तो वो SIP के द्वारा निवेश कर सकते है Sbi Mutual Fund में निवेश कर सकते है

SIP क्या है ? Systematic Investment Plan

निवेशक SIP के माध्यम से न्यूनतम 500 रुपये की राशि से भी म्यूचुअल फंड में निवेश करना शुरू कर सकते हैं। निवेशक के बैंक अकाउंट से हर महीने एक निश्चित राशि को चुने गए Mutual Fund में निवेश किया जाता है। इसके बाद निवेशक को इसके बदले में, नेट एसेट वैल्यू (NAV) के आधार पर म्यूचुअल फण्ड यूनिट की एक निश्चित संख्या दी जाती है।

Sbi Mutual Fund कैसे काम करता है ?

एसबीआई म्युचुअल में निवेश के दो तरीके उपलब्ध हैं। एसआईपी द्वारा, प्रत्यक्ष निवेश एसआईपी बैंक आवर्ती जमा के समान सिद्धांत पर काम करता है। एसबीआई एसआईपी के लिए आपका मासिक, साप्ताहिक या दैनिक निवेश एक निर्धारित तिथि पर आपके बैंक खाते से स्वचालित रूप से निकाल लिया जाता है। यह राशि आपकी पूर्व-स्थापित एसबीआई म्युचुअल फंड योजनाओं में से एक के लिए रखी गई है। कीमतें हर दिन बदलती हैं। नतीजतन, वितरित मात्रा हर बार अलग-अलग होगी।

Sbi Mutual Fund में निवेश करने की स्कीम

SBI इक्विटी म्यूच्यूअल फंड

Sbi Mutual Fund द्वारा निवेशकों को लग कैप ,मिड कैप ,और स्माल कैप की योजनाओ में निवेश करने की सुबिधा देता है और ये जो फण्ड होते है वो लॉन्ग टर्म के लिए अच्छे रेतुर्न देते है

SBI डेट म्यूच्यूअल फण्ड

SBI डेट म्यूचुअल फंड मुख्य रूप से डेट और परमानेंट इनकम सिक्योरिटी के मिश्रण में निवेश करते हैं। फिक्स्ड इनकम सिक्योरिटीज़ में ट्रेजरी बिल, गवर्नमेंट सिक्योरिटीज़, मनी मार्केट इंस्ट्रूमेंट्स आदि शामिल हैं। इन सिक्योरिटीज़ की एक निश्चित मैच्योरिटी तारीख़ होती है और एक निश्चित ब्याज़ दर मिलती है।

Read More - Sbi Mutual Fund क्या है ?

1 note

·

View note

Text

Lumpsum Investment in Mutual Funds | SBI Investapp | इन्वेस्टमेंट करें म्यूच्यूअल फण्ड में

Watch video on TECH ALERT yt

https://youtu.be/lcjoLasPQ94

#TechAlert #howto #technology #sip #mutualfund #lumpsum #SBI #investapp #investment #interest #trendingreels #viral #Youtube #shorts #love #girls #teenage #growth #howtoinvest #invest

#Lumpsum Investment in Mutual Funds | SBI Investapp | इन्वेस्टमेंट करें म्यूच्यूअल फण्ड में#Watch video on TECH ALERT yt#https://youtu.be/lcjoLasPQ94#TechAlert#howto#technology#sip#mutualfund#lumpsum#SBI#investapp#investment#interest#trendingreels#viral#Youtube#shorts#love#girls#teenage#growth#howtoinvest#invest#instagood#like#technical

1 note

·

View note

Text

Northern Arc Capital IPO: A Strong Contender in the Market

Northern Arc Capital IPO, a non-banking financial institution (NBFC), has garnered significant attention from market analysts who recognize its strong demand and profitability in the financial sector. On the cusp of its initial public offering (IPO), the company revealed that it secured ₹229 crore from a range of esteemed anchor investors. The anchor investors list includes SBI General Insurance Company, SBI Life Insurance Company, Reliance General Insurance Company, Kotak Mahindra Life Insurance Company, Goldman Sachs (Singapore) Pte., Societe Generale, and Quant Mutual Fund.

Northern Arc Capital IPO Details and Timeline

The Northern Arc Capital IPO opened for public subscription on September 16 and closed on September 19. The price band for the offering was set between ₹249 and ₹263 per equity share, with the minimum bid size being 57 equity shares, followed by multiples of the same thereafter.

The company structured its IPO with a balanced allocation across investor categories:

- 50% of the shares were reserved for qualified institutional buyers (QIBs),

- 15% for non-institutional investors (NIIs),

- 35% for retail investors. Additionally, Northern Arc Capital allocated 590,874 shares for employees at a discounted price of ₹24 per share.

Northern Arc Capital IPO Robust Subscription Demand

The IPO witnessed immense demand from investors, leading to a total subscription of 110.91 times by the fourth day. Data from the Bombay Stock Exchange (BSE) highlights that:

- The retail investor portion was subscribed 31.08 times.

- The NII segment saw subscriptions totaling 142.41 times.

- The QIB portion attracted significant interest, with a subscription rate of 240.79 times.

- Even the employee category, though smaller in size, was subscribed 7.33 times.

The IPO received a total of 2,38,22,43,807 bids against an offer of 2,14,78,290 shares, according to data from the BSE.

Northern Arc Capital IPO Day-by-Day Subscription Progress

Northern Arc Capital's IPO showed remarkable traction throughout its subscription period. On the third day, the issue was subscribed 20.18 times, and by the second day, it had already reached 9.99 times subscription. The IPO had a solid start on its opening day, with a subscription rate of 2.87 times, underscoring strong investor confidence in the company from the outset.

Northern Arc Capital IPO Grey Market Premium (GMP) Trends

The grey market premium (GMP) for Northern Arc Capital's shares has been a subject of keen observation among market participants. As of September 21, the GMP for the IPO stood at ₹128 per share, according to investorgain.com. This indicates that Northern Arc Capital shares were trading at a premium of ₹128 over their issue price in the grey market.

Given the upper end of the price band at ₹263 per share, the current GMP suggests an estimated listing price of ₹391 per share, representing a 48.67% premium over the issue price. Historically, IPOs with a strong GMP trend often indicate positive market sentiment and potential listing gains.

GMP Trends Over Time

ipogmp.org noted that Northern Arc Capital Imppo GMP has fluctuated between ₹0 and ₹202 over the past 11 years of grey market activity. Despite the fluctuations, the current strong GMP signals that the IPO is on track for a robust listing.

Expert Recommendations

While the grey market premium is a key indicator of demand, experts advise caution. Investors are encouraged to seek guidance from certified financial professionals before making any investment decisions, especially in IPOs that may carry inherent risks.

Northern Arc Capital’s strong subscription numbers, positive GMP, and solid anchor investor backing position it as a key player in the financial sector with promising prospects for growth. The upcoming listing is highly anticipated, with market participants expecting a favorable debut for the NBFC.

Read the full article

#BajajHousingFinance#DetailsipoNorthernArcCapital#gmp#ipo#ipoNorthernArcCapital#ipoNorthernArcCapitalopen#list#market#multibagger#Northernarccapital#NorthernArcCapitaldetailsipo#NorthernArcCapitalipo#NorthernArcCapitalipobandprice#NorthernArcCapitalipodate#NorthernArcCapitalipogmp#NorthernArcCapitalipogmptoday#NorthernArcCapitalipolotsize#NorthernArcCapitaliponews#NorthernArcCapitalipopricebar#NorthernArcCapitaliposize#NorthernArcCapitaliposubscriptionstatus#NorthernArcCapitallimitedipo#NorthernArcCapitallimitedipodetails#NorthernArcCapitallimitedipogmp#NorthernArcCapitalnsesmeipo#ShareNorthernArcCapitalopen#stock#Stockmarket#Subscription

0 notes

Text

How to Place an Equity SIP (E-SIP) Order through SBI Securities App?

youtube

Equity-SIP Is A Tool That Helps You Build Your Portfolio Over The Long Run With Consistency & Discipline! Enjoy a Fast, Seamless and Intuitive investing

0 notes

Last Seen Blogs

glimpseofsanity

Transcendence

leonidas2

Без названия

nhandinhbongda3s

nhandinhbongda3s

elizondodeb

Deborah Elizondo