#also like every other city rent is more expensive than a mortgage

Text

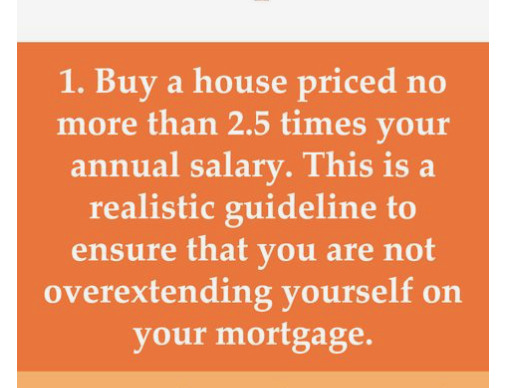

so this just came up on my pinterest feed:

the average individual income in my nearest major city is $64,500 and average household income is $126,700. (according to Career Beacon, whoever they are)

assuming Career Beacon means that is the average gross salary, at 2.5x that's $161,250 and $316,750 respectively.

if they mean that is the average net household income, that bumps it up to $87,500 and approximately $200,000. So according to the pinterest advice, your budget for a house should be $218,750 or $500,000.

average house price in that same city? close to $700k

In my old neighbourhood in that city, condo PARKING SPACES were regularly listed for $40k-$75k. you can't even get a reasonable studio condo anywhere in the city proper for $316,000. in the outskirts, like out past the suburbs...maybe. but then you're paying through the nose for transportation.

you can get a nice (and I do actually mean nice, I'm not being sarcastic or snarky at all I swear) trailer home in the middle of fucking nowhere in a 55+ community for $150-$300k. good luck accessing transit though.

#depending on the neighbourhood a detached house can run you $650k to $5 million or more#(that 650k is land value only btw it's most likely a dilapidated husk of a house being held up by mold termites and spite)#semi detached seem to be in the $600k-$1.2m range#condos where literally every wall is shared with neighbours: $400k-$4.5m#also like every other city rent is more expensive than a mortgage#torn between “I would LOVE to have an annual salary of $64k that sounds like SO MUCH MONEY”#and “even if I earn more than the Prime fucking Minister I'll never own a house in a location I actually want to live in”#while sitting in the house my parents bought in 1989 for $90k#(that they can't afford to move out of bc what's it's currently worth won't buy them a decent house less than 1/2 the size)#and the house before this one? they bought it in 1984 for $33k#like I know home ownership isn't supposed to be a goal for my generation anymore#but fuck what I wouldn't give to have a home that *I* own that nobody can take away from me#I've already had one rental sold out from under me#and every time I've moved (not counting in/out of university residence) hasn't been my decision#so it'd be nice to have some housing stability & security for the first time in my adult life#also financial stability & security#like enough to buy a reasonable house#and reliably afford sufficient food for a week without having to stretch 4-5 days worth of food for a whole week

0 notes

Note

mtl to settle down in the city,suburbia or county side? i love your blog!!

oh interesting!! ranked them city to country and got a little introspective <3

most to least likely to live in the city

→ OIKAWA convinces himself he’s a city guy. he just wants to get away from his rural hometown, so he’d spend the rest of his time in the biggest city he can find. probably posts pictures and tags his location as the city he’s in even though every single photo is in that place.

→ KENMA just can’t imagine himself anywhere but the city. he probably lives in the penthouse suite of a skyscraper with an amazing view and outrageous rent, and he sees at least two rats on the street every week along with dealing with sometimes iffy air quality. still, he wouldn’t trade it for anything.

→ SAKUSA doesn’t even think of it as a choice. he chooses the city because he thinks it’s the most logical option, even though he does think about how living in the countryside would be nice, too. he’d live in the new but not overly populated part of town, very expensive but worth it to him.

→ KUROO feels more comfortable in the city. growing up in tokyo made him like the high density and movement of the big city, and he’d find more job opportunities and things he’d want to do there. also makes fun of the country provinces too much to live there.

→ KAGEYAMA wants the greatest opportunities he can afford, and he thinks the city is better geared for that. he wants to be in the center of it all. facilities with the best courts, gyms with the best trainers, and easy access to anything else he can wish for all exist in the city.

→ BOKUTO bounces around from the city to the country but ends up staying in the city. he likes to stay near his family in tokyo, and even though he strays to other towns every now and then, he’ll settle in the city because that’s where his heart and friends (and job) belong.

→ ATSUMU wants to live somewhere urban but might chose to stay in a smaller city. he’s from rural hyogo, but he feels like everything wants to do and the people he wants to meet are in the city. still, he keeps his kansai dialect and is really proud of his hometown, and he sometimes misses the rolling fields and starry skies.

→ TSUKISHIMA could go either way, but he ends up in the wealthy outskirts of the city because that’s where he gravitates towards. he was never the kind of person who wanted nothing more than to leave their hometown, but he eventually drifts off and finds somewhere else he really loves.

→ OSAMU might settle down in the suburbs. it’s a happy medium between the fast pace of the city and the countryside life he’s used to, and it’s the place he can imagine himself living for the rest of his life. he’ll visit home occasionally and visit friends in the city, and life is good.

→ USHIJIMA lives in the suburbs because it’s easy to commute to the city and back home. he’s taking things like mortgage prices and local schools into consideration when making his decision, and it’s a smart choice. probably has a picket fence around his house and lives in a neighborhood with a tennis court, and it’s his ideal life.

→ HINATA wants to be a cool city guy, but he likes the freedom, peace, and nature that living in miyagi gives him. he’ll go back and forth, though when the chance to really settle down is given, he opts for the countryside or suburbs. it’s closer to his roots, and he’s happy to be there.

→ KITA lives in the countryside. he grew up there, he has family there, and he honestly doesn’t understand the appeal of the city. it’s not like he stays exclusively in rural parts of the country, but he makes his living and orients his life there. he’s content that way.

#haikyuu headcanons#haikyuu hcs#haikyuu x reader#hq headcanons#haikyuu scenarios#haikyuu imagines#oikawa x reader#kenma x reader#kuroo x reader#kageyama x reader#bokuto x reader#atsumu x reader#tsukishima x reader#osamu x reader#ushijima x reader#hinata x reader#kita x reader#philia.headcanons#request.filled

500 notes

·

View notes

Text

This is basically a 1000-word essay, so I’ll put this up here, but do encourage you to read, especially if we disagree and someone sent this to you in a desperate gamble to make you understand.

TLDWR: capitalism does all the ooga-booga that people say socialism does anyway, and the failings are all exactly the same and happens regardless of what economic system you use. Call it what you want, but make living independently actually possible, and the village people will be much less likely to come at you with our fucking pitchforks you idiots.

The reason I believe minimum wage is insufficient and the rich would be fine if they were more heavily taxed:

A lot of these numbers have been simplified to make it easier to follow, but other than the hypothetical 10% tax, they are all roughly accurate to what I could find researching.

If my tax rate is 10% and I make $300 dollars a week, then that leaves me with $270 a week. Take out for groceries at an average of $50 I have $220. Assuming that I don’t have any prescriptions, or rent, or cable, or gas, or utilities, or really anything else considered mandatory for adulting, then that’s not bad, right? But, most people do have those other things, so that’s not so good. So, instead, we make cuts here and there, eat less healthy, decide we probably don’t need to go to the doctor for that pain, because maybe it isn’t something serious after all, and if it is serious, we may have to miss work, and then we may get fired.

If the rich have a tax rate of 10% and make 5,000 dollars a week that gives them 4,500. They would pay more a week in taxes then I make in a week. But they would still have plenty of money to live comfortably.

Rounding down on most things here, but average rent for America is ballpark $1000 a month, mortgage rates I found reported around the same. And that is of course assuming that you qualify. Bear in mind that apartments can require that you make, for example, double the cost of living there as a security measure, and banks will turn you down if they believe your income is too low for a loan. Phone $100. Medical I won’t even presume to make an average on because insulin costs more than most gaming consoles. And I highly doubt the richest of executives is buying one of those every month. I also won’t touch cars, as gasoline prices fluctuate and mpg varies. A monthly pass for public transport, if you’re lucky enough that your city has reliable transport, averages at about $60, but closer to $100 isn’t super unusual for big cities.

So, changing that weekly take home of $270 to a monthly of 1,080 and check it against those prices. Assuming that utilities is included, which covers things as basic as trash disposal and plumbing, we are in pristine health and insurance is paid for and half way decent, which is not a given, as well as no student loans since we’re working on federal minimum wage here, we get to keep negative $80. It costs $80 more than you make at federal minimum wage to live for a month as an independent human being.

Reminder, the -$80 average I found does not include: Food, any form of health care, any utilities, clothing, internet or entertainment outside of what comes with your phone plan, transportation outside of public infrastructure, any surprise fees or expenses of any kind.

I am not touching education costs, including the additional cost of public school. I could make a whole post off the cost of public education without the rest of this depression inducing rant.

At above what Obama wanted to define as wealthy you could do that working one week a month and still have money to put back in the economy.

I grant that this was done off (just above) the federal minimum wage, so most people are probably making more money than this, especially if they’ve been in the same job for a while. But I also took the national average costs for most of the expenses. And anyone working for tips can very easily be making about half that. You also may have noticed that I didn’t include grocery in my monthly figure, because while everyone eats, the cost varies widely, and you can get free food if you need it from banks, churches, your job if you’re in that area of the service sector and lucky, etc.

Yes, if you just start printing money and handing it out, inflation is going to ruin life. But, if you redistribute existing wealth instead of letting it amass and be hoarded by a handful of individuals who basically just pass it around among themselves if they do anything, while still collecting more, then instead there would be a still largely constant amount of wealth, but it would be used instead of artificially rarified (now) or drastically devalued (creating new currency and adding it to the pile). The people who say we can’t just pay people more willy-nilly aren’t wrong unfortunately. And I can certainly understand how someone who has their life style assured struggles (whether through managing to claw up, surviving to the point where it assured by government support paid by with taxes, or some combination) to understand the plight of those who don’t without realizing the climb keeps getting steeper. Presently, people who are actively doing and creating are inevitably passing the money they earn back up to the people who do not, who pass a fraction of it back. Instead of just increasing the amount of currency, now largely a digital entity, so at least we don’t have to trade our wallets for wagons, we need to ensure circulation and assess distribution.

A lot of people don’t like the “s” word, even people on social security will talk about how socialism would destroy this nation. There are also people who believe minimum wage raising would destroy industries. They don’t think it’s fair that the rich should have to pay more. But, if the rich paid 10 cents on every dollar they brought in, they honestly might not even notice. If a person working minimum wage pays 10 cents on every dollar they make then they probably need to live with other people and pool all their recourses in a communal setting while politicians and the wealthy eat expensive meals, spend extravagantly and don’t suffer in the least, like in *insert current socialist or communist boogeyman state* but with the “average” person being aware people are living like this and not personally seeing it.

MacKenzie Scott has proven that the ultra-wealthy would not suffer from increased taxation by, essentially, cutting out the middle man and almost privatizing socialism, as absurd as that sounds. Dolly Parton is also an individual who proves that obnoxious levels of wealth are still possible while distributing wealth to those who don’t have it, though I don’t know as many of the particulars with her. I do know they both, as well as others I do not know, choose to redistribute their wealth to lower social rungs and are still fabulously wealthy.

#socialism#communism#capitalism#cost of living#rant#eat the rich#I don't even care if you do it literally#bare minimum#humanity#value of human life#democratic socialism#democratic capitalism#economy#probably just shouting into the void

5 notes

·

View notes

Text

This Hard Journey

Fic prompt: “There’s something you should know…” Michael Guerin Day 2. This picks up after yesterday’s “This Hard Life” - a part of interconnected ficlets of an AU after the shed, where Alex doesn’t join the Air Force. Mentions of Malex and an Alex/Other here. Finished on ao3 here.

***

He finally got a dog, was all that Michael could think as he sat outside of the house that matched the address Max pulled from the DMV. They had always wanted to get a dog together, but with pet deposits and the tight budget for rent and food, that had always been a non-starter for them. Not anymore.

The quiet shaded street just off of the Buchanan Arts District was lined with old-style Craftsman homes among the peppered in new, renovated sprawling McMansions born of the house flipping obsession during the real estate boom. New construction sprouting between old, mature trees, juxtaposing progress with tradition.

Alex had chosen one of the older homes, untouched by the remodeling fad with a large fenced in yard filling the property footprint, and a dog house that mimicked the main house in style. Two solid years of song-writing had rewarded Alex with financial security, and of course, after three years living in cramped efficiency apartments and noisy neighbors with Michael, the first thing Alex would want again was a house. The roots of his upper middle class childhood were never far away.

Pressing his forehead against the steering wheel, Michael worked to gather the courage that kept him propelled down the over 1,100 miles from Roswell to Nashville. He had made it here, the least he could do was knock on the door instead of freaking out over the fact that Alex had a house with a mortgage while all Michael could muster in the two years since was buying a bank-possessed Airstream.

At least it was better than sleeping rough in his truck again, something he had done when he fell behind on the rent after Alex had left.

Michael took a deep steadying breath and pushed himself out of his truck. The spans of sidewalk suddenly seemed longer than I-40 through Oklahoma. Another deep breath, the irony of borrowing Alex’s self-soothing habit not lost on Michael at all, he tucked his left hand into a pocket to hide the old damage and knocked firmly on the front door.

There was a long silence extended, shoving anticipation into chagrin as Michael turned his head to peek at the tiny side-carport, confirming there was a car there. A loud, chorus of deep barks picked up from within the house. The dog sounded big, but none of that registered as he picked up Alex’s voice, muffled and indistinct.

“-calm down, buddy. Stay- no, stay- It’s probably Daddy’s new speakers arriving-”

After two and half days of driving, Michael had perfected his speech to Alex. It hit every open wound between them, from the fact he was sorry he hadn’t gone with him, to the weak but true explanation that he wasn’t ready then, but he was now. Then finally the big dice throw, the gamble of everything, that every city needed a good mechanic, Nashville was no different, it was no pressure- but maybe? Maybe they could start over?

The door swung open, and like a bag of spilled marbles, all of Michael’s words scattered away from him.

“Michael?” Alex’s polite smile for an expected delivery dropped into disbelieving shock. He did a comical double take, looking back into the house, then to Michael, then over Michael’s shoulder. The classic Chevy truck parked on the street chased away the shock. “Jesus Christ, it really is you.”

“Alex.” Michael swallowed, his eloquence gone. “You look good.”

They had had three years together, and during that time Michael had seen so many different versions of Alex Manes. He had seen Alex tired, dark circles shading his eyes more consistently than eyeliner with an off-kilter alien antennae from the Crashdown. He had seen Alex resolute, using his shoulders to impart a warning in his black clad Wild Pony shirt to any drunk who dared to give him a hard time. He had seen Alex awkward, as he helped Michael with his chores at the Foster’s ranch when it came to cleaning out a cow pen or pulling the twine efficiently off baled hay. He had seen Alex ashamed, as Michael patiently explained during their first grocery store visit that the EBT card only covered certain items.

This Alex was new. Clean, well-rested, skin clear and not tight on his cheekbones from lean meals or bloated from cheap food. An earring shined from his ear, he was dressed in a soft v-neck shirt and artfully cut frayed jeans. Good was an understatement.

“What are you doing here?”

“I’m here- I’m here because Isobel got married, and um, she wanted to invite you, but I talked her out of it. I’m sorry. I mean for that, but also for like, everything. Not following you here was something I regretted every day since, but I thought- I thought I had to stay back then, but I don’t anymore- and there’s something you should know-”

“Babe? Is that our new speakers at the door?” A new voice called out, cutting off the word vomit that was spilling from Michael’s mouth beyond his control.

A male voice.

The wince and apology on Alex’s face told Michael everything he needed to know. Well. He probably should have seen that coming. Only Alex’s reaching out quickly to grab his hand as he turned away stopped him from bolting from the house.

“No, not our speakers, but an old friend from back home is here-” Alex called back, before turning back to make deliberate eye contact with Michael. “He wanted to stop by to say hello.”

A tall well-built black man came into view, holding a squirming pit bull in his arms, walked toward them both with a bright welcoming smile, “A friend from Roswell? An actual flesh and blood human who knows you? I was starting to think you were an alien, Alex.”

“Just because you’re related to half of Nashville and went to school with the other half, Dennis, doesn’t mean I sprouted from a pod-” Alex shot back playfully, clearly picking up a well-worn argument.

Like a couple. A real couple. With a house and a dog. Michael licked his dry lips, forcing his muscles upward, they probably had retirement accounts. In two years Alex had built something more secure than he had in the three years in Roswell.

“Well any friend of yours, Alex, is one of mine,” Dennis greeted, turning his head to avoid an excited dog kiss before transferring the bundle of fur into Alex’s arms in a fluid movement of trust. “I’m Dennis, welcome to Nashville, um-?” he prompted, extending his left hand to Michael.

“Michael Guerin,” he answered politely, before Michael lifted his left hand awkwardly from his pocket and offered his right in return. His name didn’t alter the warm smile on Dennis’s face. Ah. So he must be a nameless ex for Alex then. Swallowing hard, Michael continued, this time a little meanly, “this hand doesn’t shake so well after I got on the wrong side of a hammer, sorry. But good to meet you.”

The stutter of the clumsy interaction hid Alex’s wince and flash of pain of the reminder.

Feeling no joy from that, Michael picked up the conversation lightly, “I’m a friend from high school. Been doing some transport work, and a job sent me here to pick up a car to drive back to Roswell, so I thought I might stop in and see what the famous Alex Manes is up to…”

“I’m not famous, I just write the words,” Alex protested quietly, before backing away from the doorway. “We were just about to have lunch, if you want to stay-”

“He’s famous, don’t listen to him,” Dennis interjected proudly. “Did you hear that new song from Paramore? Alex wrote that.”

“Oh I know, I have all the singles Alex wrote,” Michael smiled, looking around the house and at the couple with another deep breath. “I’m his biggest fan, I think. But um, thank you, I can’t stay, I gotta hit the road back to-” he started to say home, but that hadn’t been true for a long time. “Back to Roswell.”

***

Hours later with his heart heavy, Michael checked into his room at the Super 8. Normally the expense would have bothered him, but after his day, he figured he was entitled to a little bit of spoiling. And if it was sad that plain wrapped soaps and tiny shampoo bottles constituted spoiling, well, he was content with that.

The clunky black case of his small portable DVD player was propped open on the hotel bed. It was a hand-me-down as technology and electronic gadgets moved into smoother, more versatile means. For him, it was perfect to watch a borrowed DVD in his Airstream since he lacked cable.

With the entire contents of a motel conditioner in his hair, Michael started the paused video file. The shaky dark footage started playing, the sound crackling with amateur hands, before the clear, strong voice of Alex Manes filled the air.

It was probably pathetic to watch this cribbed footage from YouTube, but the romanticism that fueled his journey down 1-40 was also the same sentiment that preserved this moment in amber for Michael. Pulling open his old notebook from high school, he let Alex’s voice singing about love and loss carry him through the calculations of point atmospheric entry and the parallax distance of habitable stars.

It would be a hard journey, but Michael didn’t know any other kind at this point. Roswell wasn’t his home. Nashville wasn’t going to be home either, but the universe was ever-expanding, surely there was a place for Michael?

#mgweek20#guerinweek20#malex fic#the lost decade#au after the shed#michael guerin#alex manes#roswell new mexico#Malex#angst here but eventual happy ending#will it show up in the tags?#no one knows certainly not me

81 notes

·

View notes

Note

how do you know what class you're in?

Your social class in the UK?

I think it’s really hard to define, and I honestly think most people in the UK “just know”- although I also sort of know that’s a stupid thing to say.

There are economic factors and there are cultural factors, and it’s also down to your family history. And there are classes within classes too- you can be upper middle class, or upper working class, for example.

The following is semi-serious, semi tongue in cheek, and I’d love my followers to chip in too!

Working class: Your family have traditionally worked in non-professional jobs. These might be skilled trades, service/hospitality jobs, “unskilled” jobs or casual work. These days, they might be self employed, but they would be unlikely to employ someone else. There are varying degrees of financial comfort, and these days, your family may own their own home but you’re not “wealthy”. It’s unlikely your family have assets or investments beyond one property and cars (if they are doing well). If you’re younger than about 35, you or your siblings might have gone to university, but no-one in your parents’ generation has. Your parents probably have a degree of debt beyond a mortgage (if they have one). You probably spent time in childcare when you were young because your parents had to work.

You probably speak with a regional accent and use dialect words. You also use words like serviette, desert, pardon etc. Someone in your family is really into football and supports a team that isn’t in the premiership- if they are into rugby then it’s rugby league unless you’re from Wales or Cornwall. Your female relatives are probably quite house-proud and take a lot of care over their appearances. You probably have a hobby, but it’s probably not one that requires a lot of expensive equipment.

Family and community are important to you- it’s likely you haven’t moved that far from where you grew up (unless you were really desperate for work). It’s possible the area where you grew up is pretty deprived, although it may be increasingly a victim of gentrification, depending on where you are from. Your family home may have been a council house or rented, and it’s very likely that your housing didn’t always feel secure.

If you celebrate Christmas, this was probably really important to your family and your parents might have gone a bit overboard with this, even (especially) if they couldn’t afford it.

At some point in your life, you’ve used the word “scab” as an insult- even if you didn’t know what it meant.

Middle Class: Your family have traditionally worked in more professional jobs. These may not require a degree (especially historically), but we are talking things like accountant, lawyer, doctor, teacher, civil servant etc. They earned a salary rather than being paid by the hour. Some degree of their assets were probably inherited, and they may have some investments e.g. shares or a buy to let property, but this isn’t the whole of their income (unless they are retired and have a decent pension too). Your parents owned their own home, and are/will be mortgage free by the time they retire. You probably had regular foreign holidays growing up. Your parents are likely to save up for big ticket items, rather than get into debt. You’re not the first generation in your family where people went to university. It’s very likely you had a stay at home parent for part of your childhood.

If you speak with a regional accent, it’s probably pretty soft, and it’s likely you don’t use a lot of regional dialect words. You call your midday meal lunch, and your evening meal dinner. If you go to the pub to watch a sports match, it’s more likely to be the six nations than a football game. But it’s equally likely you aren’t into sport at all. Your parents probably made you get swimming and music lessons growing up, and you may well have a hobby- possibly one that requires a bit of financial investment on your part. You like to think you have a sense of style, but you don’t like to look like you are “trying too hard”.

Your family probably don’t all live in the same place, and you may only see them relatively rarely. It’s likely your parents have friends from uni or NCT classes who to some extent take the place of family in your life. You may not have a strong sense of community and it’s very possible that if your parents live rurally, you might have moved to the city for work. You’re probably not very religious.

At some point in your life, you have sneered at someone for being a “chav”. It’s likely you’re quite insecure and there’s lots of things you don’t think of as “classy” and try to avoid.

Upper-middle Class: Your parents are pretty wealthy and almost definitely went to university. You went to a well known university. They likely went to private school and you probably did too (although not a super famous one). If you didn’t go to private school, you went to a grammar school, church school or the most sought after “comp” in the county (your parents probably moved house to get you in). Someone in your extended family or friendship circle owns a second home, or at least a really nice house in the country. You/your parents almost definitely have inherited wealth and assets, as well. You/your parents may just work in a well paid job, but they may also own a medium to large size company. You probably had multiple holidays abroad each year (and it’s very likely you went skiing). If one of your parents’ cars broke down, it would have been very easy for them to replace it, without needing to save up or get into debt, but you don’t have any fear of debt, either. It’s very likely you can get a job through “connections”. It’s likely they employed a cleaner and possibly a gardener, and maybe au-pair or nanny as well.

You speak with an RP accent, and you might have “pudding” after your “supper”. It’s very likely you play a team sport of some kind, probably rugby, cricket, hockey or maybe lacrosse. You might row, or ride horses, or sail. You’ve always been able to do whatever expensive hobby you like, and money has never been a barrier to progressing. You may well shop in charity shops, and brag about the bargains you find there. You may drive an “old” car, but it’s probably a 4x4, genuinely vintage, or quirky in some other way. You have inherited jewellery and possibly some home furnishings. If you’re talented in some way, (sport or artistic) you were probably given every opportunity to persue this.

Networking is important to you and you feel part of a community. You’re probably quite socially confident. It’s likely you know some of the people you work with socially as well. You probably expect to live a reasonably traditional lifestyle, and you’re less likely to be part of a “sub-culture” (unless you’re making a career as an actor or a musician). You probably observe religious festivals, but you don’t go regularly to a place of worship.

On some level, you probably think “poor” people bring it on themselves through poor decision making.

Upper Class: Historically, your family were rich enough not to have to work for a living, and someone in your extended family owns a very large amount of land. You’re related to someone with a title. You went to a well known private school and you may have boarded. It’s likely your family own multiple properties- some are rented out and some you live in. Some or all of these were inherited, rather than bought. You may have a “private income” of some kind. Your family may have had to “diversify” in recent years, and you may actually be working more than your ancestors did. You might have gone to a well known university, or you might have gone to somewhere like RAU. Your family own multiple cars, and one of them is probably a 4x4. It’s likely your family employed “staff”. At some point since the second world war, your family may well have had to sell off property etc- but your money worries are “how do we avoid selling off land” not “how do we afford to replace the washing machine”.

You talk like you are from the 1940s, and everyone you know has a stupid sounding nickname. You use your own form of impenetrable slang- probably specific to whatever school you went to. You’ve probably been hunting and you know someone who plays polo. You go to events like Royal Ascot, Henley Regatta, the Boat Race and Goodwood etc. You ski. You’ve been on multiple long haul holidays, and you probably went on a “Gap Yah”.

Everyone you know knows everyone else you know and you’re suspicious of people who you don’t have acquaintances in common with. You’ll get married, in a church (you are CofE and white) and having children is fairly important to you. You’re probably involved with some kind of charity work.

You pride yourself on not being a snob, because you got on well with the people you met in Africa, but you’ve never actually spoken to someone who grew up in a council house.

33 notes

·

View notes

Text

America's economy is cooked

We are in an extraordinary moment, but not an entirely unprecedented one. Since the earliest days, societies have had to cope with disasters that wiped out the ability of everyday people to service their debts and thus threatened to destroy their societies.

If you've read U Missouri econ prof Michael Hudson's writings on the subject, you know that for millennia, rulers in these circumstances simply wiped out the debts, declaring a "jubilee" that allowed people to rebuild after disasters rather than being trapped in debt spirals.

In a new essay on Naked Capitalism called "How an 'Act of God' Pandemic Is Destroying the West: The US Is Saving the Financial Sector, Not the Economy," Hudson reveals the abyss on whose brink we are balanced, and what we must do to pull back from it.

https://www.nakedcapitalism.com/2020/09/michael-hudson-how-an-act-of-god-pandemic-is-destroying-the-west-the-u-s-is-saving-the-financial-sector-not-the-economy.html

Hudson's oft-repeated golden rule is "Debts that can't be paid, won't be paid." That is to say: making it harder to declare bankruptcy, or binding debtors over to arbitration or wage-garnishing won't actually get them to pay debts they cannot afford.

This is a very sharp observation in the US context. The 2008 crisis was "solved" by bailing out finance, not people - and so the finance sector was able to lend to consumers to buy things again, while consumer debt mounted to spectacular levels.

Between mounting costs for housing, education, transport and health - a place to sleep, a path to employment, a way to get to work, the physical capacity to do your job - being alive has meant increasing your debt burden.

And now the US real economy - the wage-generating (and thus debt-servicing) economy - has ground to a halt. The finance economy continues to boom, largely on the (obviously false) premise that debts will continue to be repaid.

It's worth contrasting the US approach - the $1200/person bailout, the $6T finance bailout - with other countries that are less beholden to their finance sectors.

Canada and many EU governments simply assumed the payrolls of firms, relieving them of their major expense and providing ready cash to consumers that the can use to purchase from those retailers that remain.

And in China, where most of the finance sector is state owned - where banks are public utilities - debts were suspended: "debts, rents, taxes and other carrying charges of living and doing business cannot resume until economic normalcy is able to resume."

Contrast with the US, with ever-more-desperate measures to deny the iron law that "debts that can't be paid won't be paid."

Regulators have unshackled new forms of predatory lending (aka "fintech") with APRs in the hundreds or thousands of percent:

https://theintercept.com/2020/08/30/fintech-debt-personal-loans-economic-crisis/

And at the other end of that pipeline is a massive debt-collection bubble, as fintech subprime darlings like Oportun unleash a tsunami of debt lawsuits (more than 30/day!) against people with no means to pay:

https://www.propublica.org/article/the-loan-company-that-sued-thousands-of-low-income-latinos-during-the-pandemic

Desperate, broke people are willing to work for ever-lower wages, which puts downward pressure on EVERYONE'S wages.

Hudson: "Rising debt overhead serves the business and financial sector by lowering wages while extracting more interest, financial fees, rent and insurance."

America's longest period of expansion - the post-war boom - kicked off with the lowest levels of debt in living memory (wartime wages boomed, while wartime shortages left consumers with nothing to buy). Every recovery since has increased the economy's debt-to-asset ratio.

Eventually there comes a reckoning. Debts that can't be paid won't be paid. Business as usual has been to "let creditors foreclose and draw all the income and wealth over subsistence needs into their own hands."

But that's no longer possible. We've hit bottom.

US consumer debts can only be paid by "shrinking production and consumption, leaving them as strapped as Greece has been since 2015."

Something has to give: "either the population’s broad economic interests, or the vested interests insisting that labor, industry and the government must bear the cost of arrears that have built up during the economic shutdown."

The decision to to force businesses to pay rent during the shutdown led mass bankruptcies: a business that closed for months while accruing a rent buildup cannot recover - even a year of normal takings will leave it with no profits, every penny diverted to the landlord.

19% of hotel mortgages are in arrears, 10% of retailers - commercial real-estate mortgages stand at $2.4T. 40% of retail tenants are not currently paying rent - building up more indebtedness that can't be paid (debts that can't be paid won't be paid).

And while the US government can conjure money into existence by typing numbers into a spreadsheet at the central bank, states and cities (now starved of sales/property tax) cannot, and many are also bound by "balanced budget" rules.

Neither the GOP nor the Dems are willing to confront this. McConnell has advised states to meet bond obligations by raiding their pensions. Dems have abandoned efforts to provide relief to working people.

It's a very different story in China: "China can recover financially and fiscally from the virus disruption because most debts ultimately are owned to the government-based banking system. Money can be created to finance the material economy, labor and industry, construction and agriculture. When a company is unable to pay its bills and rent, the government doesn't stand by and let it be closed down and sold at a distressed price to a vulture investor."

For thousands of years, governments have understood that crises can only be weathered through debt forgiveness. The Anglo-American madness that insists that debts that can't be paid will someday be paid has hit bottom.

64 notes

·

View notes

Text

“The Other Guys” wants cops to go after the real criminals

Before director/writer Adam McKay pivoted into populist screed’s against capitalism and political corruption in films like “Vice” and “The Big Short” he was largely known as one of the many “dumb comedy” directors working in Hollywood.

In fact, with major productions such as “Anchorman,” “Talladega Nights,” and “Step Brothers” he could almost be billed as THE dumb comedy director or certainly THE Will Ferrell director at least.

(To a certain extent, THE John C. Reilly director too.)

Those movies are certainly divisive amongst some filmgoers, as you either fall into the “turn your brain off and laugh” category or the “this is pure nonsense” crowd. I’m somewhat in the middle on all of it but one McKay/Ferrell vehicle provided a bridge between the “dumb comedy” years and his more serious satires of American politics and that movie was 2010’s “The Other Guys.”

Billed as just another parody of buddy cop flicks, “The Other Guys” is a comedy that still holds up pretty well by today’s standards. Mark Wahlberg in many ways plays an unhinged caricature of every tough guy persona he has ever played in detective Hoitz and perhaps more brilliantly Ferrell, as detective Gamble, is allowed to be the straight man of the duo for change, finding humor in a more subdued performance. Together they form a kinetic duo that play hilariously well off each other in a film that is rarely dull from start to finish.

youtube

(Flawless logic here in the famous Tuna vs Lion debate)

“The Other Guys” takes some decent shots at the violent nature of cop culture from excessive police overreach in the film’s hilarious opening scene to cops’ shoot first ask questions later approach with detective Hoitz backstory involving shooting Dereck Jeter during game 7 of the World Series. In between more typical Ferrell comedy flare involving hot wives and ex-wives, hobo sexy orgies, and TLC references there’s a lot of pointed, tongue-in-cheek humor at the police that one can find great humor in.

It’s a descent satire of the cop movie and the culture around law enforcement on this alone but McKay’s real target isn’t the police so much as it is who the police aren’t going after.

youtube

(For the record, peacocks and cops, for that matter, don’t fly.)

2008 probably feels like eons ago to many of you at this point but it was the year I personally came of age. I had graduated high school, The Lakers were good again, “The Dark Knight” and “Iron Man” had just come out, I had hopes and dreams as I entered college at San Jose State and oh…the Great Recession had just started!

I’m not going to go into extreme detail here but our economy had it’s worse collapse since the Great Depression caused by the subprime mortgage crisis due to vast widespread failures in financial regulation, breakdowns in corporate governance, vast trading and over borrowing, housing bubbles bursting, and heads of businesses just vastly ill-equipped to handle their hubris in that moment.

Major businesses and banks were on the verge of collapsing and then at the last minute the US government passed a $700 billion, with a capital B, bailout to put them all back in the green.

Corporations like Bank of America, Citi Group, Morgan Stanley etc received between $10-$25 billion each for their struggles and were able to stay alive in the country’s ever worsening state. This was great, except 2.6 million average working-class people lost their jobs during this period, including my father.

By the way, a guy like Joseph Casano, an executive at AIG, got a $34 million bonus for helping lead companies such as his into the recession.

This is McKay’s real target in “The Other Guys.” The satirical cop humor is largely window dressing to draw audiences in to the theaters so that he can show all of them who the real criminals of this country are.

As the plot of the story starts to kick into full gear the more obvious culprits of a typical Hollywood cop movie are dismissed. Though Hoitz is convinced it’s more the usual cop movie style villains of “sex and drug traffickers” at first, Gamble slowly pieces together a plot of dastardly insider trading. What it ends up being is that the bad guy is really just a doofus hedge fund manager named David Ershon played comically by Steve Coogan who made one too many bad investments to bad people.

Ershon has put his people and the people he owes money to deeper into the red, not at all unlike the wealthy CEOs and bankers who messed up the country during the 2008 recession, and it has led him to take desperate action to get everyone’s money back. Ershon, of course, tries to get Hoitz and Gamble off his tale by bribing them in a variety of hilarious ways (one of the funnier sequences of the film) but eventually gets caught up with the SEC and those who prosecute white collar crime (who are unsurprisingly also in bed with the people he owes money to).

youtube

(Somehow, I don’t think this is far off from reality...)

Hoitz and Gamble continue on the case but find that taking on white collar crime is…complicated to say the least but most importantly ineffectual as detailed in this scene.

youtube

(Again, probably not far off from reality...)

The 2008 recession, wiped out millions of jobs, with rural parts of the country getting hit the hardest and in many ways still feeling the effects today. If you were a POC you were even more unlikely to not recover from the crash. Property values plummeted, student high education success rates dropped, opiod overdoses from “unemployment deaths” and many more awful things happened during this period of great economic distress.

And what happened to the folks largely responsible for causing this mess? They got a fat fucking payday and a dismissive finger wag largely by our own government.

“The Other Guys,” more or less, ends the same way. Despite putting away Ershon, the company he was swindling, who gambled their people’s money, was still bailed out by the US government. A real “happy ending” that is played as a dark, matter of fact, joke before the credits roll.

(Again, we laugh but how far off from reality is this really?...)

I graduated from college in 2013, tens of thousands in debt from student loans and trying to navigate a largely bereft job market where wages had largely not changed in as many years. In 2008 average rent cost about $850 a month, by 2013 it was $953, today in 2020 it’s $1,097. The average entry level salary (for a clerical/ office professional) between 2008 and 2018 went from $46,886 to $45,882 showing a decrease in value.

In 2008 the richest man in the world, Warren Buffet, was worth $64 billion. The richest man in 2020, Jeff Bezos, is worth $200 billion.

If the fact that Jeff Bezos is worth more than some countries on this planet doesn’t make you infuriated alone I don’t know what will.

Btw Buffet’s net worth increased as well to $79 billion himself, in case you think it’s “unfair” to compare him to Bezos.

Sometimes I think the reason people aren’t angrier about this worldwide is 1) a bunch of us think we are all one hard working day away from being filthy fucking rich ourselves, one of the many great lies of capitalism and 2) many of us don’t actually know just how big a BILLION dollars is, so here let me help you all out:

With COVID in 2020 we’re seeing it all happen again, just as it did in 2008. Record unemployment rates, small businesses closing, evictions skyrocketing because no one can pay rent and all we got for it was a $1,200 band-aid (assuming you did get yours). Meanwhile billionaire slugs like Bezos and Elon Musk saw their net worth rise sharply during this period, hell even the fucking Lakers got a $4.6 million dollar “small business” loan (though they did return it…only after getting caught…).

The highest sum of cash ever stolen from a bank was $18.1 million (equivalent to roughly $30.1 million now) in 1997. These are the people cops and other “loose cannons” in popular actions movies are usually running up against. If you think stealing $30.1 million is a lot of money worth sending the cops over then $700 billion of our own tax dollars given to people who ruined the lives of millions of Americans should make you fucking furious. The only real difference here is one was made legal by our own elected government.

Adam McKay’s “The Other Guys” may be on its surface just another “dumb comedy” that mostly satirizes cops, but its villains are very real and unfortunately as American as apple pie. Under capitalism our labor only continues to get devalued every year (even the skilled positions), while the richest 1% of the human race only get fatter with their wealth. Things are only getting more expensive and the working man is getting priced out of more and more daily luxuries and even essentials. This way of life is not sustainable, especially for our environment which these dragons continue to plunder, and eventually we will need to actually hold our overlords accountable for letting it get this far.

If we don’t, they will continue to steal every penny in our pocket and bleed us dry until the next disposable drone can fill our place. If law enforcement won’t take this on, sooner or later we might have to…

youtube

Remember, pimps don’t cry...

#The Other guys#will ferrell#mark wahlberg#adam mckay#comedy#satire#cops#police#blm#black lives matter#rage against the machine#punk rock#movie#film#2008 recession#covid#income inequality#bailout#eat the rich#populism#social justice#socialism#Steve coogan#Jeff Bezos#warren buffett#billions#the rich#the poor#wealth inequality#The rock

9 notes

·

View notes

Text

Advantages of Renting Office Area

As an alternative to buying commercial qualities for the organizations, you are able to lease office place as it could be a handy solution for all your company specifications. Even though buying a residence could have a few positive aspects, it is really not ideal for every business. From the present atmosphere, following a big fiscal downturn and recession that engulfed throughout the world the recent years; renting office area has turned out to be an incredible advantages for a lot of businesses. You are able to hire office place for a variety of good reasons, consisting of the next listing of advantages:

Save Money:

You can expect to spend less as you won't be shelling out for the mortgage and also the costs that come along with buying property. Rather you may use the cash that you simply save to your company to help make issues shift alongside easily. Furthermore, most places of work that are create to rent are often prepared and nicely-loaded for occupancy. So, if you intend to avoid the hassle of undergoing the planning and construction stages of your office, renting would be the perfect way to go.

Headache-Cost-free Upkeep:

It may be cheaper in terms of routine maintenance. You won't must be worried about any issues regarding the house as those will be dealt by the property owner. A professional maintenance company will repair it without charging you as it's included in your monthly rent if something breaks or requires to be repaired in your office. This center also includes cleaning up or routine maintenance monthly bills, household utility bills, water charges, cell phone expenses and online fees. Moreover, your business will likely be furnished with security and car parking places. These establishments could be extremely beneficial for you as it might assistance to save massive amount of money and time.

All-Inclusive Amenities:

You may get express-of-craft properties for your organization alongside with a lot of facilities. In addition, office spaces may be personalized to completely suit your requirements - from dimensions to providers, tiny places of work to sizeable production line room as well as other facilities for example furniture, electric devices, telephones, access to the internet etc. Renting also provides meeting, training and conference bedrooms, a hanging around or wedding party place, a kitchen, the cafeteria area and living room to relax from the office. Every one of these more features can undoubtedly relieve the full procedure for operating a business.

Provides Mobility:

It can allow you to be versatile. If you plan to relocate to some other place in the future then purchasing a space can prove to be a waste of time and money, when you are unsure about the success of your business or. Also, if you decide to expand your business and feel the need to shift a bigger premise or to a different location then having a flexible rent agreement can be more convenient than having to sell the property and re-establish the entire set up elsewhere.

More info about Cho thue nha Van Phuc City site: web link.

1 note

·

View note

Text

Why Buy A Home in Lewisburg, WV?

Maybe you’re wondering if it is a smart move to buy a home in Lewisburg, WV. Frommer's Budget Travel Magazine named Lewisburg as "America's Coolest Town."

And if that isn't enough to convince you, we have listed 5 reasons why buying a home in Lewisburg is a great choice.

Many homebuyers choose Lewisburg, West Virginia because of the following reasons:

The privilege to have a home near historical landmarks.

Beautiful views.

Wide range of affordable home choices.

Affordable cost of living

Safe community

According to the U.S. Census 2019, Lewisburg has added 1,400 people in the last 20 years. These numbers are continually growing. It is easy to see why a lot of home buyers want to move here.

Affordability and community are the two main things that most Americans consider when buying a home. Based on these factors, more and more people are choosing Lewisburg as their home.

Let's look further at each reason we've listed for buying a home in Lewisburg.

1. The privilege to have a home near historical landmarks.

Located in the picturesque county of Greenbrier, Lewisburg is indeed a must-see. One of the attractions that make tourists travel to this city is the many historical landmarks. The city's chest of historic treasures includes century-old theatres and museums.

You will find almost every historic architectural style you can imagine. These designs and styles range from Victorian Gothic to Mid-Century Modern. A lot of residential homes can have those fantastic styles too. A day tour is not enough to see everything that the city offers.

If you live in or near Lewisburg, you have a lot of time to explore the gem that Lewisburg is. To entice you a little more, we made a brief itinerary for you:

Theaters. This city of 3800 plus residents is home to one of the four Carnegie Halls in the world. This world-renowned auditorium is a popular tourist attraction. Watching artistic performances is something to look forward to once you are a new town resident. And since you're only a few minutes drive away, you can conveniently visit them anytime. Lewis Theatre and Greenbrier Valley Theatre are in Lewisburg too.

Museums. If theaters are not your thing, there are plenty of museums here too. The famous Greenbrier Historical Social and North House Museum are in Lewisburg also. Are you a history buff? If yes, you are in luck! There is so much history here in Lewisburg.

Art Galleries. A place known to be big on the arts would most likely have many art galleries. Exhibits are abundant in Lewisburg for enthusiasts. Carnegie Hall has a section for art displays too. It will be a good idea to check this out before you watch a live performance.

2. Beautiful views.

Lewisburg is lucky to be located in one of the country's scenic states. West Virginia is called "Mountain State" for a reason. Its location is within the Appalachian Mountains region, and it's right next to the Mississippi River. Rivers and mountains right next to each other are a glimpse of heaven on earth.

Several of the famous sights in the Mountain State are notable for their natural beauty. A lot of those breath-taking views are in Lewisburg.

Imagine paradise being a few blocks away from your doorstep. Heaven on earth, indeed!

The Lost World Caverns is one of the popular attractions in Lewisburg. Visitors here descend 120 feet below the ground into a century-old cavern. The deep parts of the cave reveal big and glowing stalactites. The Lost World Caverns is one of the many places you will get to visit while living here.

3. Wide range of affordable home choices.

The city has a median home value of around $30,000 lower than the country's average. There is no question of why more people opt to buy their own home instead of rent here in Lewisburg.

In anything we buy, price is most often the first thing we check. This rule also applies when buying homes. Lewisburg will give you a wide range of choices from country cottages to luxury homes. The good thing about them is they're affordable.

Get your finances in order. Talk to your mortgage broker about how much house you can afford. Buying your dream house is a considerable investment. There's always more to it than just the purchase price.

4. Affordable cost of living

Housing is not the only thing that's inexpensive in Lewisburg. The overall cost of living index in Lewisburg is 90.7. That’s 10% lower than the national average. The commodities looked into are transportation, utilities, groceries, health, and miscellaneous. Lewisburg ranked more economical than the U.S. average for all of these living expenses.

The cost of living is an essential factor to consider. You may be able to afford the house of your dreams, but if the living expenses eat up your budget, it's going to be hard to enjoy your home. You will most likely look for a different property because you can't afford to live in the house you bought.

These expenses will be the least of your worries when you buy a home in Lewisburg. Groceries and utilities eat up a big part of everyone's budget. If the cost of those were less, you have more money to spend on other things you can enjoy in the city. You can use the money you saved to take advantage of the many recreational activities offered by Lewisburg.

5. Safe community

With a crime rate that's almost 10% lower than the national average, Lewisburg is no doubt safe. Cost, environment, and community are essential things to consider, but scoring a great real estate deal turns into waste without peace of mind and security.

I'm ready to buy a home in Lewisburg. What's the next step for me?

The first step is to get a smart and reliable realtor. Buying a home is one of the biggest transactions you will ever make. Things can be complicated and frustrating, but it does not have to be a long process with the help of a real estate agent. Getting an expert will give you that dream home in Lewisburg without much hassle.

For a smooth and stress-free home hunting in Lewisburg, don't randomly pick any real estate agent. Find a broker with an extensive knowledge of the neighborhood and a good track record.

I would love to help you find your dream home, call me, Rebecca Gaujot, at 304-520-2133.

youtube

In case you cannot view this video here, please click the link below to view Why Buy A Home in Lewisburg, WV? on my YouTube channel: https://www.youtube.com/watch?v=Ka4Ci9JJKM0&feature=youtu.be

3 notes

·

View notes

Text

Reforming student finance: Looking beyond scrapping tuition fees

Every Labour leadership contender has backed the scrapping of tuition fees, which is great, and is absolutely the correct policy. Most other developed nations manage to have free higher education, so why not the UK as well? If we can afford to bail the banks out, build HS2 and a bridge from Scotland to Northern Ireland, then surely we can afford to cover the cost of higher education for all.

However, although the debt is somewhat off putting for many potential university students and so some will opt not to go at all, there is a cost that has a larger more practical impact. The absolute maximum a student living away from home outside of London can receive in a maintenance loan is £8,944. That amount is only for students whose household income is £25,000 or under, and so for every household income band above that, the figure students can receive goes down and down and down.

The household income figure is usually based on the student’s parents’ income, if the student is under 25. This student maintenance would only not be based on the income of the student’s parents if they are categorised as an ‘independent student’. In order to be categorised as such, they would either have to have been supporting themselves financially for at least three years, be estranged from their parents, be married or in a civil partnership or have no living parents. So unless a student would go to the drastic measure of killing off their parents or marrying their best mate in order to get full maintenance, they’re a bit stuck.

However, what happens in most cases is students don’t receive the maximum loan - if a student comes from a two parent household, the household income is likely to be in the £40,000s, which leaves the student with between £6,000 and £7,000 to live on.

The reason why SFE sets the bands up in the way it has is it assumes students outside of London living independently will be able to live on £8,944. It then assumes that someone who comes from a household where the income is £25,000 or less will not be able to contribute towards their adult son or daughter at university. The next assumption is that as household incomes go up, their parents are willing and able to make up the difference so the student will still have that £8,944 to live on.

There are clearly a lot of problems with the assumptions that SFE make and the information it uses to make these assumptions. It assumes that £8,944 is enough to live on. In some university towns/cities it probably is okay. But that’s only if the rent is cheap in the town/city (e.g. somewhere like Middlesbrough, Hull, Sunderland), the student can get a contract that only lasts the length of the academic year (or near enough) so they’re not paying for 3 months rent during the summer when they’re not there and they don’t have to pay board to their parents during the holidays

The next wrong assumption is parents will make up the difference. The way SFE works out how much maintenance to give a student is purely income, not disposable income. For example, consider two students with two sets of parents both with household incomes of £40,000. Both students will receive £7,019 for the year. Student A is an only child whose parents have already paid their mortgage off and they can afford to top their son/daughter’s maintenance up by an additional £3,000 a year. Student B has two younger siblings still at school and their parents are renting in London (SFE only takes into account where the student will be studying, not where the parents live). Student B’s parents can only contribute a little extra top-up here and there.

This is far from hypothetical. My parents couldn’t afford to top me up to the full amount, but I was very lucky in that I only went to university in cheap cities and always got shorter rent contracts, so I managed. However, a student who was on my course dropped out purely because of financial reasons. Her parents were on high incomes, so she was in one of the lowest bands for student finance. However, she was also one of quite a few children (and one of the oldest) and her parents had very high mortgage repayments. Although I was in a more middle band, her parents could barely afford to top her up at all so she had far less than me to live on. We were going to live together for a placement year in a more expensive city, until she realised she literally could not afford to live there. She left our course and changed to a course without the placement year.

“But you can get a job!” I hear some older people who went to university for free yell in the distance. Working while at university can be great for some people, it can help build their CV, it can help them get work experience, it can help them build skills. Getting a job whilst studying can be a really positive decision for some students. However, it shouldn’t be a choice that students are forced to make for financial reasons so they can afford to eat and pay the rent - student finance should cover that. Students who work on average receive lower grades than those who don’t work. If a student genuinely wants to work and thinks it will be beneficial to them beyond the financial, and so would be happy with getting a 2:1 at the end instead of scraping a 1:1, then that’s fine, but a student’s grades shouldn’t have to suffer because they needed to work. To add to that, for some courses working really is not practical - courses with virtually full-time contact hours where they still have reading and assignments to do when they’re not physically in lectures/tutorials/labs. If they want to be able to attend university, complete all their reading and assignments and also occasionally sleep, there probably isn’t much time to get a job as well. Students with work placements also won’t have much time to hold down paid employment as well. Imagine a medical student working for free on placement at least 9-5 most days, slotting university contact hours in and also ensuring they are read up on what they are meant to be, then also trying to work part-time alongside all of that for extra cash. It’s just not feasible, to the extent that many universities have banned students from taking on paid part-time jobs on some courses (e.g. medicine, nursing, veterinary) and Cambridge strongly advises against all students taking on part-time jobs during term time because terms are so intense - the argument from them being you’re not at university to work, you’re there to study.

What the Labour leadership candidates need to do is look beyond just the scrapping of tuition fees and to the student finance system as a whole. Students are being let down once they are at university - it’s not the tuition fees that make it unaffordable for some, it’s the cost of living and SFE’s inability to cover that. Whether it’s a loan or a grant, or a mixture of the two, all students should receive a minimum which covers the cost of living. If wealthier parents then want to top it up, or students still want to take on part-time work, then so be it, but that finance should enable students to actually study.

#labour leadership#labour leadership election#rebecca long-bailey#keir starmer#lisa nandy#tuition fees#scrapping tuition fees#abolishing tuition fees#student finance#student finance england#sfe#university#higher education#higher education funding#education#uk politics#politics

9 notes

·

View notes

Text

Cheap Homes and Tips For Buying a House in Sale

A home is a financial asset and more: it's a place to live and raise children; it's a plan for the future; it's an investment in your community. That's why all Americans should have an opportunity to enjoy the benefits of owning a home. And here are some tips for first-time home buyers.

Knowledge is said to open doors. This is literally true when it comes to buying a home. To become a first-time home buyer, you need to know where and how to begin the home buying process. The following questions and answers have been carefully selected to give you a foundation of basic knowledge of home purchasing. In addition to helping you begin, these steps will give you the tools necessary to navigate the entire home buying process - from deciding whether you're ready to buy house, all the way to that final proud step of owning a home, getting the keys to your new home.

1. HOW DO I KNOW IF I'M READY TO BUY A HOME?

You can find out by asking yourself some questions:

Do I have a steady source of income (usually a job)? Have I been employed on a regular basis for the last 2-3 years? Is my current income reliable?

Do I have a good record of paying my bills?

Do I have few outstanding long-term debts, like car payments?

Do I have money saved for a down payment?

Do I have the ability to pay a mortgage every month, plus additional costs?

If you can answer "yes" to these questions, you are probably ready to buy your own home.

2. HOW DO I BEGIN THE PROCESS OF BUYING A HOME?

Start by thinking about your situation. Are you ready to buy a home? How much can you afford in a monthly mortgage payment? How much space do you need? What areas of town do you like? After you answer these questions, make a "To Do" list and start doing casual research about property. Talk to friends and family, drive through neighborhoods, and look in the "Homes" section of the newspaper, Foreclosure Listings, and internet search.

3. HOW DOES PURCHASING A HOME COMPARE WITH RENTING?

The two don't really compare at all. The one advantage of renting is being generally free of most maintenance responsibilities. But by renting, you lose the chance to build equity, take advantage of tax benefits, and protect yourself against rent increases. Also, you may not be free to decorate without permission and may be at the mercy of the landlord for housing.

Owning a home has many benefits. When you make a mortgage payment, you are building equity. And that's an investment. Owning a home also qualifies you for tax breaks that assist you in dealing with your new financial responsibilities- like insurance, real estate taxes, and upkeep- which can be substantial. But given the freedom, stability, and security of owning your own home, they are worth it.

4. HOW DOES THE LENDER DECIDE THE MAXIMUM LOAN AMOUNT THAT CAN AFFORD?

The lender considers your debt-to-income ratio, which is a comparison of your gross (pre-tax) income to housing and non-housing expenses. Non-housing expenses include such long-term debts as car or student loan payments, alimony, or child support. Monthly mortgage payments should be no more than 29% of gross income, while the mortgage payment, combined with non-housing expenses, 4 should total no more than 41% of income. The lender also considers cash available for down payment and closing costs, credit history, etc. when determining your maximum loan amount.

5. HOW DO I SELECT THE RIGHT REAL ESTATE AGENT?

Start by asking family and friends if they can recommend an agent. Compile a list of several agents and talk to each before choosing one. Look for an agent who listens well and understands your needs, and whose judgment you trust. The ideal agent knows the local area well and has resources and contacts to help you in your search. Overall, you want to choose an agent that makes you feel comfortable and can provide all the knowledge and real estate services you need.

But make sure you check the prices for homes in the area on internet before you visit any real estate agent.

6. HOW CAN I DETERMINE MY HOUSING NEEDS BEFORE I BEGIN THE SEARCH?

Your home should fit way you live, with spaces and features that appeal to the whole family. Before you begin looking at homes, make a list of your priorities - things like location and size. Should the house be close to certain schools? your job? to public transportation? How large should the house be? What type of lot do you prefer? What kinds of amenities are you looking for? Establish a set of minimum requirements and a 'wish list." Minimum requirements are things that a house must have for you to consider it, while a "wish list" covers things that you'd like to have but aren't essential.

7. WHAT SHOULD I LOOK FOR WHEN DECIDING ON A COMMUNITY?

Select a community that will allow you to best live your daily life. Many people choose communities based on schools. Do you want access to shopping and public transportation? Is access to local facilities like libraries and museums important to you? Or do you prefer the peace and quiet of a rural community? When you find places that you like, talk to people that live there. They know the most about the area and will be your future neighbors. More than anything, you want a neighborhood where you feel comfortable in.

8. HOW CAN I FIND OUT ABOUT LOCAL SCHOOLS?

You can get information about school systems by contacting the city or county school board or the local schools. Your real estate agent may also be knowledgeable about schools in the area.

9. HOW CAN I FIND OUT HOW MUCH HOMES ARE SELLING FOR IN CERTAIN COMMUNITIES AND NEIGHBORHOODS?

Your real estate agent can give you a ballpark figure by showing you comparable listings. If you are working with a real estate professional, they may have access to comparable sales.

10. HOW CAN I FIND INFORMATION ON THE PROPERTY TAX LIABILITY?

The total amount of the previous year's property taxes is usually included in the listing information. If it's not, ask the seller for a tax receipt or contact the local assessor's off ice. Tax rates can change from year to year, so these figures may be approximate.

11. WHAT OTHER TAX ISSUES SHOULD I TAKE INTO CONSIDERATION?

Keep in mind that your mortgage interest and real estate taxes will be deductible. A qualified real estate professional can give you more details on other tax benefits and liabilities,

12. IS AN OLDER HOME A BETTER VALUE THAN A NEW ONE?

There isn't a definitive answer to this question. You should look at each home for its individual characteristics. Generally, older homes may be in more established neighborhoods, offer more ambiance, and have lower property tax rates. People who buy older homes, however, shouldn't mind maintaining their home and making some repairs. Newer homes tend to use more modern architecture and systems, are usually easier to maintain, and may be more energy-efficient. People who buy new homes often don't want to worry initially about upkeep and repairs.

13. WHAT SHOULD I LOOK FOR WHEN WALKING THROUGH A HOME?

In addition to comparing the home to your minimum requirement and wish lists, use the Home Scorecard and consider the following:

Is there enough room for both the present and the future?

Are there enough bedrooms and bathrooms?

Is the house structurally sound?

Do the mechanical systems and appliances work?

Is the yard big enough?

Do you like the floor plan?

Will your furniture fit in the space? Is there enough storage space? (Bring a tape measure to better answer these questions.)

Does anything need to repaired or replaced? Will the seller repair or replace the items?

Imagine the house in good weather and bad, and in each season. Will you be happy with it year-round?

Take your time and think carefully about each house you see. Ask your real estate agent to point out the pros and cons of each home from a professional standpoint.

14. WHAT QUESTIONS SHOULD I ASK WHEN LOOKING AT HOMES?

Many of your questions should focus on potential problems and maintenance issues. Does anything need to be replaced? What things require ongoing maintenance (e.g., paint, roof, HVAC, appliances, carpet)? Also ask about the house and neighborhood, focusing on quality of life issues. Be sure the seller's or real estate agent's answers are clear and complete. Ask questions until you understand all of the information they've given. Making a list of questions ahead of time will help you organize your thoughts and arrange all of the information you receive. Prepare your own Home question list before you visit property. Find out about monthly utility bills for entire home.

15. HOW CAN I KEEP TRACK OF ALL THE HOMES I SEE?

If possible, take photographs of each house: the outside, the major rooms, the yard, and extra features that you like or ones you see as potential problems. And don't hesitate to return for a second look. Organize your photos and notes for each house.

16. HOW MANY HOMES SHOULD I CONSIDER BEFORE CHOOSING ONE?

There isn't a set number of houses you should see before you decide. Visit as many as it takes to find the one you want. On average, home buyers see 15 houses before choosing one. Just be sure to communicate often with your real estate agent about everything you're looking for. It will help avoid wasting your time.

YOU'VE FOUND THE DREAM HOME

17. WHAT DOES A HOME INSPECTOR DO, AND HOW DOES AN INSPECTION FIGURE IN THE PURCHASE OF A HOME?

An inspector checks the safety of your potential new home. Home Inspectors focus especially on the structure, construction, and mechanical systems of the house and will make you aware of only repairs,that are needed.

The Inspector does not evaluate whether or not you're getting good value for your money. Generally, an inspector checks (and gives prices for repairs on): the electrical system, plumbing and waste disposal, the water heater, insulation and Ventilation, the HVAC system, water source and quality, the potential presence of pests, the foundation, doors, windows, ceilings, walls, floors, and roof. Be sure to hire a home inspector that is qualified and experienced.

It's a good idea to have an inspection before you sign a written offer since, once the deal is closed, you've bought the house as is." Or, you may want to include an inspection clause in the offer when negotiating for a home. An inspection t clause gives you an 'out" on buying the house if serious problems are found,or gives you the ability to renegotiate the purchase price if repairs are needed. An inspection clause can also specify that the seller must fix the problem(s) before you purchase the house.

18. DO I NEED TO BE THERE FOR THE INSPECTION?

It's not required, but it's a good idea. Following the inspection, the home inspector will be able to answer questions about the report and any problem areas. This is also an opportunity to hear an objective opinion on the home you'd I like to purchase and it is a good time to ask general, maintenance questions.

19. ARE OTHER TYPES OF INSPECTIONS REQUIRED?

If your home inspector discovers a serious problem a more specific Inspection may be recommended. It's a good idea to consider having your home inspected for the presence of a variety of health-related risks like radon gas asbestos, or possible problems with the water or waste disposal system.

20. HOW CAN I PROTECT MY FAMILY FROM LEAD IN THE HOME?

If the house you're considering was built before 1978 and you have children under the age of seven, you will want to have an inspection for lead-based point. It's important to know that lead flakes from paint can be present in both the home and in the soil surrounding the house. The problem can be fixed by repairing damaged paint surfaces or planting grass over effected soil. Hiring a lead abatement contractor to remove paint chips.

21. DO I NEED A LAWYER TO BUY A HOME?

Laws vary by state. Some states require a lawyer to assist in several aspects of the home buying process while other states do not, as long as a qualified real estate professional is involved. Even if your state doesn't require one, you may want to hire a lawyer to help with the complex paperwork and legal contracts. A lawyer can review contracts, make you aware of special considerations, and assist you with the closing process. Your real estate agent may be able to recommend a lawyer. If not, shop around. Find out what services are provided for what fee, and whether the attorney is experienced at representing home buyers.

22. DO I REALLY NEED HOME OWNER'S INSURANCE?

Yes. A paid home owner's insurance policy (or a paid receipt for one) is required at closing, so arrangements will have to be made prior to that day. Plus, involving the insurance agent early in the home buying process can save you money. Insurance agents are a great resource for information on home safety and they can give tips on how to keep insurance premiums low.

23. WHAT STEPS COULD I TAKE TO LOWER MY HOME OWNER'S INSURANCE COSTS?