#Building equity

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The KCSC sent more than 20K requests to delete posts related to prostitution and porn to Tumblr from January to June 2017.

Text

Building equity in your home is one of the most significant financial benefits of homeownership. Home equity represents the portion of your property that you truly own, which increases as you pay down your mortgage and as your property’s value appreciates. For Canadian homeowners, understanding how to build equity over time can lead to substantial financial advantages. Here’s a guide on how to effectively build equity in your home.

0 notes

Text

Rent vs. Own: Busting Myths and Building Your Future

Ever feel stuck in a rent cycle? Each month, a significant chunk of your income disappears into someone else’s pocket, leaving you with no ownership stake. Many people fall into this trap, but there’s a better way! My Story: From Renter to Homeowner For years, I believed in the “work hard, get rich” mentality. Countless jobs later, I was left with little to show for it. The turning point came…

1 note

·

View note

Text

What Does It Mean to Build Equity?

If you own a home, one of the benefits compared to renting is that each month you’re making mortgage payments, so you’re building an asset which is equity. Equity refers to the amount of your home that you truly own after you take into account the debt you owe.

To calculate your current equity, you should subtract your loan balance from your home’s market value.

If the number is negative, then your home is worth less than what you owe on it. That means you have upside-down equity.

This is obviously not the goal. The goal is to grow your equity over time as you pay your loan. Until you pay off your mortgage, even though you’re considered a homeowner, your lender still has an interest in your property.

You own your home, but it’s collateral for your loan.

How Does Equity Work?

If you bought a home for $200,000 and you put down $40,000, which would be a 20% down payment, you would then have a home equity interest of 20% of your home’s value. You own the $40,000 of your home right off the bat because of your down payment.

If your home value goes up over time, then while your loan balance could stay the same, your equity could go up. If you bought your home and the market spiked, so your home was worth $400,000, you’d still owe only $160,000, meaning you’d have gone from owning 20% of the home to 60%.

How Can You Build Equity?

The primary way you increase your equity is by paying off your loan.

If you have a standard amortizing loan, that means you’re making equal monthly payments. Those payments in this scenario go toward the interest and principal. Over time the amount that’s going toward your principal goes up. Each year that you own your home and pay your mortgage means you’re gradually paying it off faster.

You can also grow your equity by working to increase the value of your home. Home prices do tend to rise in a healthy economy on their own as long as the real estate market is doing well, and you can speed that up based on the work you do to your home.

You can also make accelerated payments on your mortgage. Most of the time as a homeowner, you’ll make 12 payments a year. If you split a payment into two equal amounts and send it every two weeks, you end up making 26 payments a year. That ends up being the same as having paid 13 monthly payments, so you’re taking some interest off the total life of your loan.

You’ll be able to pay your mortgage faster and build equity more quickly too.

Using Home Equity

The equity you have in your home is an important asset, and it’s calculated as part of your net worth. You can use your equity in different ways.

If you sell your home, then you’re taking the equity you have in your home from the sale.

You can also get a loan against your equity. This is known as a home equity loan or second mortgage.

Overall, having a mortgage is sometimes viewed as forced savings. Each month that you’re making a payment or perhaps multiple payments, you’re building equity or building the value of an asset. It’s like adding money to a savings account but instead of your asset being cash, it’s your home’s equity.

0 notes

Text

I spent a bunch of money this past month or so (some on silly things like the Neopets tarot deck, but a TON of it was like. Furniture. A new mattress because my old one was several years past lifespan and needed towels under the middle to keep from continuing to collapse in the middle. Dental product. Family groceries for an Event) and I'm about to hit Pride Month (ton of travel and event costs, some of which I can expense for through work, since we're involved in some of those events, and some of which I can't).

Basically, I'm in a bit of a squeeze and would like to avoid digging into my savings because of the ongoing struggle of trying to put together a down payment so I can move out.

Is there anything I could do to encourage ko-fi donations, commissions, or Patreon subscriptions? Other than what I'm doing already.

(I'm not in an emergency state so don't drop money you NEED, but I am almost thirty and would like to live on my own, and achieving that has been a STRUGGLE. The main reason I'm not in 'help me pay rent' mode like people who ARE in an emergency state is that I still haven't even achieved rent.)

#'why not rent?' my mom is my real estate agent so I can avoid several thousand dollars of commission fees if I buy... but ONLY if I buy.#she hates the idea of me renting instead of building equity. so if I want her help in moving out#(and I do because it is SO very much worth it to have an expert on hand) then I need to focus on buying. and that means down payment#Phoenix Talks#personal

30 notes

·

View notes

Text

Welcome to the Tribe of Hope! 🌱

Our vision is simple:

Equity for all beings.

Sustainability for future generations.

Unity through shared culture and connection.

Take the Earth Pledge. Reflect, try, care, connect, celebrate, grow, and inspire. Together, we can create a better world.

#hope for the future#together we rise#small steps#big changes#humanism#feminism#religion#philosophy#mindfulness#Earthpledge#equity#community building#eco living#eco lifestyle#global#change#health and wellness#spirituality#spiritual awakening#nature lovers#HopeForTheFuture#NatureIsHealing#spotify playlist#RitualMusic#soulfulsounds#UnityInDiversity#EthicalFuture#growthandhealing#green anarchism#transhumanism

4 notes

·

View notes

Text

“we see that you have savings and a dual income and good credit and already pay more to rent than you would to pay this mortgage monthly but what really matters to us is the income you were making 2 years ago for some reason” - banks

10 notes

·

View notes

Text

Home ownership actually kind of sucks.

As in, sucks your bank account.

10 notes

·

View notes

Text

AN OPEN LETTER to THE U.S. CONGRESS

Protect IVF! Pass HR 7056 / S. 3612 the Access to Family Building Act!

796 so far! Help us get to 1,000 signers!

As a concerned constituent, I’m emailing to urge you to cosponsor H.R. 7056 / S. 3612 the Access to Family Building Act and demand it receive a vote.

The Alabama court ruling on IVF shows we need federal protection for the right to access IVF and other services that help people start or grow a family. The Access to Family Building Act would do that and protect families and doctors from criminalization. Will you sign onto this bill and publicly call for a vote on it? I will only support lawmakers that actively fight for reproductive freedom.

▶ Created on April 18 by Jess Craven · 795 signers in the past 7 days

📱 Text SIGN PINHHO to 50409

🤯 Liked it? Text FOLLOW JESSCRAVEN101 to 50409

#JESSCRAVEN101#PINHHO#resistbot#IVF#Access To IVF#Family Building#Reproductive Rights#Assisted Reproductive Technology#HR 7056#S 3612#Fertility Treatment#Family Planning#Infertility#Health Care Access#Congress#Federal Legislation#IVF Protection#Reproductive Health#IVF Rights#Support IVF#Patient Rights#Parenting Rights#IVF Awareness#IVF Support#Cosponsor#Reproductive Freedom#Health Equity#Civil Rights#Women Health#Family Equality

3 notes

·

View notes

Text

When the vibes of the trailer home you’re looking at are just so rancid that the Zillow app literally crashes

#I have no judgement against trailer homes in general#but I can’t afford one that doesn’t look like a crime scene#I knew the real estate market was bad but lads it’s BAD#if I want to live anywhere less than an hour away from work#it’s either something even my parents couldn’t afford#or something that is unlivable without structural repairs but a ‘great investment’#I don’t want to ‘build sweat equity’ I want a small living space that I can afford to just move into#not have to repair or update#but half of these listings literally make my skin crawl

3 notes

·

View notes

Text

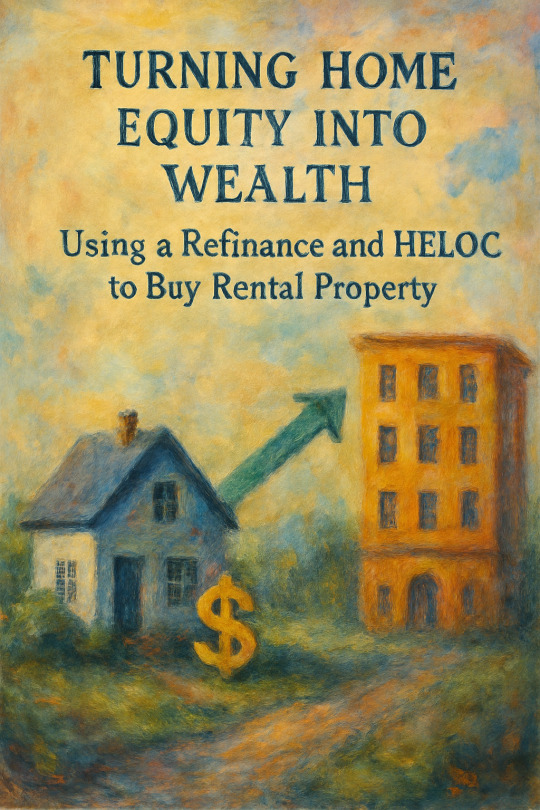

How to Turn Equity into Wealth: Using a Refinance and HELOC to Acquire a Cash-Flowing Multifamily

By The Lancaster Rose

If you’re sitting on a property that’s nearly doubled in value, you might be richer than you think—and not just on paper. Real wealth isn’t just about what you own, it’s about what you do with what you own. So if you’ve built up significant equity—say $350,000 or more—it’s time to start seeing that equity as a tool, not just a trophy.

Let’s talk strategy.

The Setup: Two Mortgages and an Equity Goldmine

Imagine you have a property with both a first and second mortgage. The first mortgage has a favorable 3.83% interest rate but comes with a hefty monthly MIP (mortgage insurance premium) of $350. The second mortgage—often a home equity loan or piggyback loan—has its own MIP, bringing your total monthly insurance burden to $650.

At first glance, it might seem unwise to refinance—after all, prevailing rates are around 6%, and that’s a decent jump from 3.83%. But when you run the numbers, you start to see the value in simplifying the structure.

Why Refinance?

• Consolidation: You can merge both loans into one, eliminating the second mortgage altogether.

• Eliminating MIP: With $350,000 in equity, your loan-to-value (LTV) could fall below 80%, which means most conventional lenders won’t require mortgage insurance at all. That’s $650/month saved—$7,800 a year in your pocket.

• Positioning for Leverage: With a simplified mortgage and no secondary lien, you open the door to something powerful: a Home Equity Line of Credit (HELOC).

Now here’s where the real wealth-building begins.

⸻

Unlocking a HELOC: The Power Move

Once you’ve refinanced and eliminated your MIP, you now own a property with simplified financing and roughly $350,000 in usable equity. Most lenders will allow you to access up to 85% of your home’s value through a HELOC, depending on credit and income factors. That means you could have $200,000 or more at your disposal.

Here’s the play: Use that HELOC as a down payment on a two- or three-family investment property.

⸻

Why This Works

A multifamily property (especially in the right market) can serve as a self-repaying investment. You draw $100,000–$150,000 from your HELOC, use it as a down payment on a $500,000–$600,000 duplex or triplex, and finance the rest with a traditional investment loan. The key is targeting a building where:

• The monthly rental income covers both the investment property’s mortgage AND

• The monthly payments on your HELOC draw.

In essence, the property is paying for itself. You’re not just borrowing against equity—you’re recycling it into a cash-flowing asset.

⸻

The Long Game: Equity Builds Equity

Here’s where things get exponential. If the new multifamily property appreciates over time—say 5% per year—you’re doubling the value of your initial investment in 6–7 years. Even modest appreciation on a $600,000 property results in a $30,000/year increase in value. Combine that with rental income, tax deductions, and principal paydown, and your return on equity explodes.

And remember—your original home is still appreciating, too. So you’re no longer riding one horse. You’re building a stable.

⸻

What’s the Risk?

As with any strategy, you need to weigh:

• Interest rate fluctuations (especially if your HELOC is variable)

• Vacancy and maintenance on the multifamily

• Closing costs on the refinance

• Lender qualification requirements

But for investors who plan, underwrite, and execute with clarity, this is a low-risk, high-reward maneuver.

⸻

Final Thoughts: Use What You Have to Build What You Want

You don’t need to sell your house to use its value. You just need to understand how leverage works. By refinancing to eliminate mortgage insurance, consolidating debt, and opening up a HELOC, you give yourself the ability to create wealth through real estate—without needing outside capital or giving up your home.

The smart move isn’t always the obvious one. Sometimes it takes seeing your mortgage not as a burden but as a bridge—to a new stream of income, a growing portfolio, and long-term freedom.

If you want help identifying good investment properties or understanding what kind of HELOC might be right for you, reach out. The door is open.

#home equity strategy#refinance to invest#eliminate mortgage insurance#HELOC for investment property#real estate wealth building#refinance mortgage 2025#cashflowing multifamily#use equity to invest#home equity line of credit#buy multifamily with HELOC#real estate investment#real estate investment strategy#leveraging home equity#refinance and invest

0 notes

Text

Demystifying Higher Education with AI

New Post has been published on https://thedigitalinsider.com/demystifying-higher-education-with-ai/

Demystifying Higher Education with AI

Higher education is at a crossroads. Budgets are tightening. Student needs are growing more complex. And the pressure to demonstrate measurable outcomes—graduation rates, job placement, lifelong value—has never been higher.

As institutions grapple with these demands, artificial intelligence isn’t some futuristic buzzword anymore—it’s a practical, proven tool that’s helping colleges and universities rise to the challenge. It’s doing the real work: powering personalized support, enabling timely intervention, and helping leaders make better decisions faster.

This shift reflects a broader evolution in how we think about higher education. Students today expect their college experience to be as responsive and seamless as every other part of their lives. If a streaming service can recommend the right show, or a bank can alert you before you overdraft, why shouldn’t your university know when you might be struggling—and help before it’s too late?

Institutions that embrace AI aren’t chasing hype—they’re stepping up to meet a new standard. And if higher education is serious about delivering on its promise to help students succeed, then AI can’t just be an afterthought. It has to be core to the strategy.

One of the biggest challenges on campuses today is capacity. Student services teams are being asked to do more with fewer resources. Advisors, financial aid officers, and support staff want to offer high-quality, human-centered help, but they’re underwater. At the same time, students expect (and deserve) immediate, personalized guidance. They don’t want to wait days for a reply to a simple question. They need answers in real time, and they want to feel like someone is paying attention. That’s where AI can make an immediate impact.

With tools like intelligent chatbots and workflow automation, institutions can free up staff from repetitive, low-impact tasks. AI can triage student questions—whether it’s about FAFSA deadlines, transfer credits, or how to drop a class—24/7. It can route more complex issues to the right person or flag high-priority cases for intervention. This doesn’t replace human connection—it makes it more possible. Staff gain back time to focus on what matters most: nuanced, high-touch conversations that build trust and drive outcomes.

AI also increases the consistency of support. When responses are automated, they don’t vary based on who’s working that day or what time the question comes in. And for students who are first-generation, working full-time, or balancing caregiving responsibilities, that kind of accessibility can be the difference between persistence and giving up.

It’s not just about convenience—it’s about equity. AI helps ensure that every student, regardless of their schedule or background, has access to the timely help they need to succeed.

Most institutions know that improving retention is both a financial imperative and a moral one. But in practice, schools still rely on reactive approaches: midterm grade checks, end-of-semester surveys, or waiting for students to raise their hands. AI enables something better: early, proactive support driven by data.

By analyzing behaviors like LMS logins, assignment submissions, attendance, and GPA fluctuations, AI can help surface subtle signals that a student might be struggling, before they’re at risk of dropping out. These models aren’t about replacing advisors with dashboards. They’re about giving staff more insight and more time to act. Even simple nudges—a reminder to complete a form, encouragement to meet with a tutor, a check-in from an advisor—can have a big impact. When timed well, these messages show students that someone is paying attention. That sense of being seen and supported helps students stay engaged and on track.

And these moments matter. In an era where more students are questioning the value of higher education, institutions have to earn student trust and demonstrate tangible value at every turn. AI helps colleges shift from triaging problems to anticipating and solving them—one student, one moment at a time.

Perhaps the most exciting promise of AI is that it enables colleges to support students not just during enrollment or in the classroom, but throughout their entire journey. With AI, we can become proactive instead of reactive. The tools coming to market today will transform the student lifecycle experience—from the first moment a prospect starts researching schools, to the day they graduate, and well beyond. This is about more than retention. It’s about long-term engagement, continuous improvement, and mission alignment.

Imagine being able to understand how your alumni are doing years after graduation—not just through an annual survey, but through real-time feedback loops. Or being able to track which outreach messages drove the most enrollment conversions and act in real time. These aren’t one-time wins. They’re ongoing feedback mechanisms that help institutions deliver more value and stay aligned with student needs.

These tools don’t just benefit institutions—they benefit students. When things work more smoothly, when support is easier to access, when guidance feels personal and relevant, students are more likely to succeed. They’re more likely to feel like they belong.

Too often, AI is still treated as an add-on—a flashy tool reserved for innovation teams or short-term pilots. But to unlock real value, institutions need to treat AI the way they treat their learning management system or financial aid platform: as foundational infrastructure.

AI isn’t just a tool for chatbots or analytics. It’s a layer that can enhance nearly every touchpoint in the student lifecycle, from marketing and enrollment to advising and alumni engagement. Think about the full journey: A prospective student lands on a university website and gets dynamic, personalized content based on their interests. They’re guided through the application process with tailored messages. Once enrolled, they get just-in-time nudges to register for classes or apply for internships. Years later, they’re prompted to complete a graduate survey or participate in alumni mentoring.

That’s not a future scenario—it’s what’s possible today, when institutions treat AI as a strategic enabler rather than a side project. Of course, with that power comes responsibility. Institutions must be clear with students about how AI is used, where automation begins and ends, and how data is collected and safeguarded. AI systems should be trained on diverse data to avoid reinforcing existing biases. And students should always have a way to escalate to a human when they need one. Equity, transparency, and human oversight aren’t nice-to-haves—they’re non-negotiables. These principles must be embedded from the start, not bolted on later.

At its core, higher education is about helping people reach their potential. It’s about creating opportunity, fostering growth, and unlocking talent. Those goals haven’t changed—but the tools to achieve them have. AI, done right, doesn’t replace the human experience of learning. It enhances it. It removes barriers, extends capacity, and gives every student a better shot at success. The most meaningful impact of AI won’t come from major product launches or shiny demos. It will come from the small ways it makes life better—for staff, for faculty, and most of all, for students.

For institutions navigating change, facing pressure, and looking to do more with less, AI offers a way forward. A way to stay true to their mission while building for the future. Now is the time to stop asking whether AI belongs in higher ed—and start asking how we can use it to serve students better at every step of the journey.

#Accessibility#ADD#add-on#ai#AI systems#Analytics#artificial#Artificial Intelligence#attention#automation#background#bank#biases#budgets#Building#caregiving#challenge#change#chatbots#classes#college#colleges#content#continuous#course#data#Difference Between#education#equity#era

0 notes

Text

Discover effective SIP planning strategies for investing in good equity mutual funds. Learn how to optimize returns with disciplined investing, professional guidance, and portfolio diversification.

#SIP investment tips#equity mutual funds#SIP strategies#investing in SIPs#mutual fund returns#SIP planning#equity SIP plans#wealth building SIP#portfolio management#SIP growth tips#long-term SIPs#best equity funds#market timing SIP#SIP for beginners#equity fund selection#SIP strategy guide#financial planning SIP#mutual fund guide#equity funds for SIP#smart SIP planning.

0 notes

Text

Top 10 Benefits of Owning a Home vs Renting in 2025

In today’s uncertain real estate market, many people ask, “Should I rent or buy a home?” While renting offers flexibility, owning a home comes with powerful long-term advantages that can significantly improve your financial future. This article explores the top 10 benefits of owning a home vs renting, helping you make an informed decision in 2025 and beyond.

1. Build Equity Instead of Paying Rent

When you own a home, your mortgage payments build equity, not someone else's wealth. With every payment, you're gaining ownership in a tangible asset — your home — rather than throwing money away on rent.

Related keyword: building equity through homeownership

2. Stable Monthly Payments with a Fixed-Rate Mortgage

Unlike rent, which can increase every year, a fixed-rate mortgage locks in your payment for 15–30 years. This provides predictable housing costs, allowing for better budgeting and financial planning.

Related keyword: fixed mortgage vs rising rent

3. Tax Benefits for Homeowners

Homeowners enjoy various tax deductions, including mortgage interest, property taxes, and in some cases, home office deductions. These perks can reduce your taxable income significantly.

Related keyword: tax benefits of buying a home

4. Increase Property Value Over Time

Real estate typically appreciates in value. When you buy a home in a growing area, your investment can increase significantly over time — a benefit renters don’t receive.

Related keyword: home value appreciation 2025

5. Freedom to Customize Your Space

Homeowners have complete control to remodel, upgrade, or personalize their living space. Renters often face restrictions on painting, renovating, or even hanging artwork.

Related keyword: owning vs renting customization freedom

6. Forced Savings Through Mortgage Payments

Your mortgage is like a built-in savings plan. Each month, you're paying down your loan and increasing your ownership stake — helping you build long-term wealth.

Related keyword: forced savings with homeownership

7. Pride of Ownership and Stability

Homeownership provides a sense of permanence, pride, and community connection. You’re more likely to engage with neighbors and contribute to your local area when you’re a homeowner.

Related keyword: benefits of owning a home long-term

8. Potential Rental Income

If you own a multi-unit home or eventually move, you can rent out your property for passive income. This option doesn’t exist when renting.

Related keyword: earn rental income as homeowner

9. Better Credit Opportunities Over Time

Paying your mortgage on time can boost your credit score, leading to lower interest rates on future loans. This can open the door to better financial opportunities.

Related keyword: homeownership and credit score

10. Protection Against Inflation

As inflation increases, so does rent. But with a locked-in mortgage, you protect yourself from rising housing costs, making homeownership a great hedge against inflation.

Related keyword: buying a home to fight inflation

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also credit repair and passive income programs.

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - [email protected]

Renting vs Buying: Which Is Right for You?

While renting offers flexibility and lower upfront costs, owning a home offers powerful long-term advantages — especially if you're planning to stay in one place for several years. If you're ready to build wealth, enjoy stability, and gain control over your living space, buying a home in 2025 may be the right move.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also credit repair and passive income programs.

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - [email protected]

Learn More!!

Prestige Business Financial Services LLC

"Your One Stop Shop To All Your Personal And Business Funding Needs"

Website- https://prestigebusinessfinancialservices.com

Email - [email protected]

Phone- 1-800-622-0453

#building equity through homeownership#fixed mortgage vs rising rent#tax benefits of buying a home#home value appreciation 2025#owning vs renting customization freedom#personal loans#personal finance#personalfunding

1 note

·

View note

Text

Anyway don't look at your investments (stocks, pensions, long-term invested savings). Keep a steady investment pace. If you don't have any investments, now is as good a time to start as any, unless if you don't have any emergency savings in which case that should always be your first priority.

I know this is a useless post on the everyone-is-broke -website but like genuinely an emergency savings account the equivalent of 3-6 months of basic living expenses is essential and once you have that even 5$ a month towards long term (5-15+ years) investments is a deeply valuable use of your money.

#bluh bluh#i know youre suspicious of the big financial systems but look. if the only way to win is not to play the mere fact that you are already her#should tell you all you need to know about what your options actually are#good praxis means investing and saving while you can in order to build equity which you can then leverage for allyship and solidarity#don't look at your investments right now if you can help it and now is as good a time as any to start

1 note

·

View note

Text

Understanding Bullying, Gossip, Harassment, and Canada's Basic Human Rights Protections

View On WordPress

#accountability#anti-defamation#bullying#bullying prevention#Canada#cancel culture#clickbait#community building#Community Empowerment#community safety#community values#compassion#corporate responsibility#cultural inclusion#cultural sensitivity#cyberbullying#defamation#defamation law#digital media#discrimination#diversity#emotional harm#emotional intelligence#Equity#ethical communication#ethical leadership#ethics#fact-checking#fairness#free speech

0 notes

Text

Equity vs. Debt: Choosing the Right Funding Strategy for Your Small Business

When it comes to financing a small business, entrepreneurs often face the crucial decision of choosing between equity and debt financing. Each funding strategy has distinct advantages and disadvantages that can impact your business’s growth, control, and financial health. In this article, we will explore the key differences between equity and debt, the factors to consider when choosing a funding…

#best practices for brand management#Branding strategies for small businesses#building brand loyalty#Business#business growth strategies#Choosing#corporate social responsibility#creating a strong brand identity#customer relationship management#Debt#digital marketing for startups#e-commerce tips for businesses#Equity#Funding#how to scale your business.#how to start a successful business#importance of social media for businesses#influencer marketing for brands#Small#small business funding options#Strategy#top business trends 2024

1 note

·

View note