#i paid 300 towards bills. another 300 towards my credit card to pay that off in full

Text

I cant believe bonuses are taxable income. this fucking blows man, I hate it

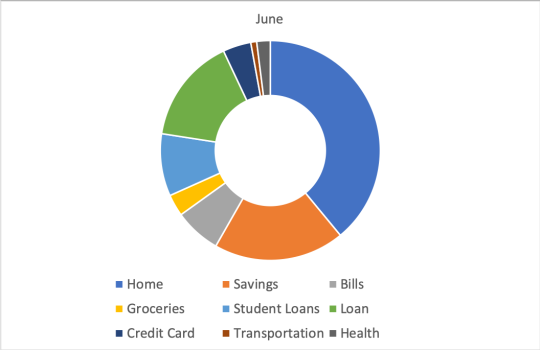

#text#mine#kieran talks#kieran.work#like. idk its fine i can still pay off what i need to i just#wont be able to get the driving lessons i planned on paying for with it#whatever its fine. i paid 2k dollars towards my teeth work#and insurance kicks back in to help with payments next month for my wisdom teeth and stuff#i paid 300 towards bills. another 300 towards my credit card to pay that off in full#ive got about. 400 left im savings to get me through to my next paycheck??#so thats my bonus and birthday money used up already i guess 😮💨😮💨#this fucking blows

0 notes

Video

youtube

21 SMART Money And Energy Saving Tips

With energy bills, fuel and interest rates soaring, there’s never been a more critical time to make savings and learn how to manage our money to the best of our ability. I cover many more tips and money-making ideas in my programme, Master Your Money the S.M.A.R.T Way training. Check it out for free - https://bit.ly/3isugCr.

Please LIKE and SHARE

Here are some tips to help you save and accumulate more money.

1 Pay yourself and save first, spend what’s left

Pay yourself first is the golden rule and money mindset the rich and well-off follow. Do this and you’re on your way towards financial freedom. Try the 50/30/20 formula and have your salary automatically paid in separate accounts:

50% of your take home pay for your needs (bills, food, minimum debt payments),

30% for fun, play, eating out and entertainment

20% saved for your future, extra debt payments, saving for emergencies and investing.

2 Avoid credit card debt interest

Plan a strategy to get rid of it credit card balances with cash or by transferring the debt to a 0% balance credit card to avoid paying interest for a fixed time (up to 30 months) COMBINED with paying off the balance every month.

Another useful tip set up a direct debit to avoid missing minimum payments and being stung with high charges and bad credit report history. You can also move to another deal if you don’t manage to clear the balance. Pay off purchase balance every month.

3 Track your income and expenditure

‘T’ for ‘track’ is included in my programme, Master Your Money the S.M.A.R.T Way training. Check it out for free - https://bit.ly/3isugCr. Set up a tracking system and also try challenger digital banks like Monzo, which allows you to transfer a set amount of spending money to your card and informs you every time it is used, ore prepaid cards – like Monese and Transferwise – where you can only spend what you load.

You can also do this manually and set your account up by allocating your income into different ‘jars’ for different needs.

4 Start saving and investing

Whatever you are earning or how much you have in the bank, you can start saving a percentage of your income. Apps such as Moneybox let you start with a few pennies by rounding up loose change every time you spend.

You can legally shelter your savings from tax by maximising your £20,000 tax free ISA allowance and using other tax shelters. Pension schemes also enjoy a favourable tax treatment. You can either put money into a cash or investment ISA, which carries more risk. Interest rates have been low for a decade but are now rising, which is good news for saver but bad for borrowers.

Check out www.gov.uk/individual-savings-accounts for more information. Check for the best cash ISA rates at Moneyfacts. Shop around and be prepared to move your money to obtain the best rates.

5 Emergency or contingency funds

Everyone needs a rainy-day fund. You should aim to have three months’ income saved for emergencies, ideally six if you have a mortgage.

6 Loyalty doesn’t always pay - switch suppliers

If you check out any good comparison site, you are sure to discover cheaper deals on your household bills, as well as savings accounts and insurance. Ofgem calculates that the average household can save £300 a year by switching to a better energy and gas deal. This might not always be possible in the current climate.

Check your latest utility statements and check out comparison sites, such as uswitch or moneysupermarket.

7 Reduce your car insurance

Some of us are using our cars less as a result of working from home, so check your car insurance is still the right fit and inform your insurer. Don’t auto renew, and check for better deals via your existing supplier and comparison websites like CompareTheMarket and MoneySupermarket.

8 Review your mortgage

Over 100,000 people reach the end of a fixed term fixed rate mortgage every month, according to a BBC report. Staying with the same lender could mean paying a ‘loyalty’ penalty of higher interest of up to £1000 a year. Consult an independent mortgage broker about remortgaging to the best deal for you even if your current deal is expiring in 6-12 months’ time.

‘R’ for ‘review’ is part of my programme, Master Your Money the S.M.A.R.T Way training. Check it out - https://bit.ly/3isugCr.

9 Check your tax code to pay less to HMRC

Make sure you’re not paying too much tax. You could even get a nice rebate from HMRC.

Working from home could entitle you to tax relief and you could claim some money back for working from home expenses in the form of tax relief paid by HMRC.

10 Look for old bank accounts and pension policies

Billions is waiting to be claimed in forgotten bank accounts, insurance policies and pension schemes. Have a root through your old papers or contact the ABI (Association of British Insurers).

You can also query your council tax band, check for discounts if you live alone or care for someone.

11 Check for any entitlements to benefits.

There are numerous benefits you can access even if you are working and earning a family income of up to £40,000.

12 Reduce your grocery bill

Buy only what you need and avoid ‘two for one’ offers, which lead to food waste and can cost you more.

Buy own brand food from supermarkets which have often scored higher in blind tests.

Plan your meals for the week ahead and use discount supermarkets and pound stores, which can be significantly cheaper that M&S, Waitrose and Tesco’s.

Explore the ‘world food; aisle in your supermarket which can have savings of up to 75% on cupboard staples including rice, lentils, beans, spices and sauces.

Shop in the late afternoons and evenings for yellow sticker discounts.

Don’t buy plastic bags and make your food, fruit and veg last longer.

13 Avoid wasting food

Use your common sense and avoid throwing away food which is still safe despite passing sell by dates.

14 Explore local charities for help – there is an abundance of food given away by supermarkets

If you are in need, use Foodbanks and the many other charities for help with food and other items including energy. They help everyone from the homeless to working people who just can’t make ends meet, and there is a lot of money and resources out there if you search. Nobody should go hungry in the west.

15 Check your workplace or private pension

Make sure you’re saving enough for retirement and you’re happy with how your pension is being invested according to your individual risk profile.

Checking whether your employer will match pound for pound any personal contributions you make – free money.

16 Check your state pension and NI contributions level

You have until next April 2023 to top-up National Insurance contributions to boost your old age state pension if you have not made sufficient contributions during your working life due to career breaks or time spent overseas. Topping up contributions can be a good investment. Check with a financial adviser.

Women in retirement may have been underpaid and could be entitled to back payments.

Go to the .gov website or Google the links.

17 Use loyalty cards, price match and vouchers and deal finders

Points, discounts and free stuff all add up on loyalty cards like Tesco’s Clubcard or Nectar.

Stores like John Lewis and Currys offer price matching policies, which are subject to change sot do your research and don’t be shy to ask.

Try hacks like VoucherCodes ‘DealFinder’ as a plug-in on Chrome to be alerted to the best deals while buying online.

There are hundreds of money saving apps and discount offers, such as Sweatcoin and BetterPoints, where you can get paid to walk and exchange your steps for store discounts and freebies.

18 Cut energy bills

Check out the Energy Saving Trust for some great energy and money saving hacks. For instance, charging gadgets overnight can cost you more than charging for a few hours during the day. And not filling your kettle up when boiling water for a cuppa and defrosting your freezer when iced up will also cut your bills.

Going paperless and paying by direct debit will save you money.

Insulating your home will keep you warm in the winter and cut energy bills. Check your local authority for tips grants on insulation and solar panels, even if you are a tenant.

19 Sell unwanted stuff on resale platforms

Did you know that the average British woman accumulates an estimated £22,000 of unworn clothes over a lifetime? You can turn unwanted clothes into cash using resale platforms such as Depop, Vinted and eBay.

You can also save money by buying through these sites for top-quality gifts and clothes instead of paying for new. Some items sold on these sites are brand new unused.

You can also clear your garage, loft and spare room of unwanted stuff by selling on sites like Facebook Marketplace and eBay.

20 Mindset – avoid emotional spending and blowing your salary on payday

In my programmes and YouTube Money Tips Podcast videos I talk about money mindset. A recent survey by Nationwide’s Payday Saveday revealed that 1 in 5 people blow over half their spare monthly wages within 48 hours of payday! Shops, restaurants and online stores gear up offers for payday surges in expenditure. Ask yourself if you really need something before you buy and give yourself time to think before parting with your cash.

21 Plan, organise and forecast

The key is in planning and organising your expenditure, work, goals, relationships and life! As in the first tip, prioritise essential expenditure and your savings pot, before spending. That way, you’ll know how much disposable income you really have to last the rest of the month. Use a spreadsheet, app or notebook to map out or forecast your finances and expenditure just like a business does. You should know exactly how much money you have in your account right now and how much is coming in and going out tomorrow.

Finally, searching for the best deals, tracking and reviewing your finances and being mindful of spending money on things to don’t really need will not only help you get through the current crises but help you form lifelong habits that will enable to build wealth.

For more ideas and tips, see out my new training to help you get control of your finances in 28 days!

Click to join: https://bit.ly/3isugCr

#freetraining #savemoney #moneysavingtips #mortgage #creditcarddebt #energybill #costofliving #goals #foodbank #getcontroloffinances #money

0 notes

Text

how i got an agent, or: my writing timeline

when i started writing, i had no idea how publishing worked and i had a lot of misconceptions about it. but i just signed my first literary agent so i thought i’d share what my experience has been getting to this point, in case it helps anyone else with their own publication goals. i’m also including financial details, like submission fees and income, because “i could never afford to pursue writing as a career” is something that kept me from taking the idea seriously.

for context, i write mostly literary fiction and i’m on the academic/scholarly writing path. this process looks a lot different for other genres.

i didn’t write this in my pretty nonfiction narrative voice; it’s really just the bare-bones facts of how it went down, how long it took, how many words i wrote (both fanfiction and original fiction), and how much it all cost.

background

2002 - 2005: read a fuckton of books, wrote some fiction, wanted to be a writer but knew it would never happen, journaled every moment of my life in intimate detail

2006: started working full-time (at a chinese restaurant) while still in high school, also started taking courses for college credit; no time to write, and forgot i had ever wanted to be a writer

2007: graduated high school, started college (psych major), still worked at the restaurant, moved out of my parents’ house into an apartment with my boyfriend; my dad got diagnosed with stage 3 colon cancer

2008: continued college full-time, quit the restaurant and started part-time as a bank teller, broke up with bf and moved in with a friend at an apartment where the rent was obscenely high; had to pick up a second job altering bridal gowns

2009: continued college full-time, started dating someone else, moved in with him, had to support him, took a third job as an admin assistant

2010: continued college full-time, still had 3 jobs; my dad’s cancer became terminal

2011: my dad passed away; i graduated college with a 3.9 and $31k of debt; quit 2 of 3 jobs; got promoted at the bank; my bf cheated on me and we broke up; moved back in with my mom

2012: a very dark time; also, bought a house (because where i’m from, it’s cheaper to buy than rent)

2013: discovered fandom

2014, age 24

this is the year i started writing and posting fanfic. prior to that i was a compulsive journaler but had no drive or desire to become a writer, despite how much i had written when i was a teenager. it seemed like a very childish dream. at this point i assumed writing was just a phase like all my other hobbies i’d picked up and set down.

but fandom proved to be really healthy for me, and i made some good friends who encouraged my writing and made me want to be better at it. i was really not very good at writing. i don’t think i had any natural creative talent whatsoever, or even a particularly vivid imagination. the only thing i had going for me was the ability to put thoughts into words after a decade of obsessive journaling.

i started writing in spring, and by the end of the year my total word count was 311k. i was making a decent income at the bank, insofar as my bills were covered and i had health insurance. i still had a significant amount of credit card debt from college that i was trying to pay down, and which was eating up all my extra income.

2015, age 25

i continued writing through 2015 and went to visit @aeriallon, whom i’d met in fandom and who told me i should consider applying to MFAs. i was miserable at the bank and knew i wanted to go back to school, but i didn’t think there was a chance in hell a grad program would accept me, since my writing wasn’t very good and i hadn’t so much as taken a single english class in undergrad. she told me to just look around and do a few google searches to see what i found.

when i started searching, i assumed i would probably be more compelled toward an MEd or MSW programs and go the therapy route, which is what the plan had been in undergrad before my dad died and my life got derailed. i never wanted to be a banker, but i’d got a promotion into commercial finance that paid decently, so i took it and told myself i’d work for a year before going back to school. but then i kept getting promoted and one year became many.

i ended up being more drawn to creative writing MFA programs because they seemed to want people with weird backgrounds like mine. also the classes sounded fun and the programs were funded. i didn’t know how i would be able to afford my mortgage payment or sell my house on a fraction of the income i was making at the bank, but i figured i’d apply and see what happened.

it took 6 months to get a writing sample ready to apply to MFAs. it was the only ofic story i’d written as an adult, and in retrospect i had no idea what i was doing because at that point i didn’t read literary short fiction. but i got the sample as good as i could get it and completed my applications. i applied to 6 schools and got accepted into 1.

in 2015 i wrote 250k. i can’t find my application spreadsheet from that year, but i probably spent between $300 and $400 on application fees. early in the year, i had finally managed to pay off my credit card debt and save a little bit of money.

2016, age 26

the school i got into was within driving distance of my house, so i didn’t bother moving. i tried to quit the bank but my boss convinced me to stay on 2 days a week working from home. i agreed to it, because my grad stipend wasn’t enough to cover my bills, and i was counting on what little savings i had accrued to get me through the program. i still had no drive or interest to publish. i mostly just wanted to go back to school so i could learn how to be better at this thing i really enjoyed doing.

in the MFA, as you might imagine, i had to read a lot of stuff and write a lot of stuff, and was encouraged to begin submitting some of the short stories i wrote for workshop. i was not particularly into the idea, considering it seemed like a lot of work for little reward, and also i didn’t think my stories were very good.

i also started teaching english comp. i hated it and decided that after the MFA, i never wanted to do it again. haha. hahahahahaha

in 2016 i wrote 343k. i didn’t apply/submit in 2016 so i didn’t pay any fees, but my grad stipend was $14k for the academic year, plus the income i was making at the bank.

2017, age 27

i did a complete 180 and decided i loved teaching more than anything else in the entire world, and i was willing to do whatever it took to become a teacher. i realized that to become a teacher, i needed to publish. begrudgingly i started submitting to literary journals. i also applied to summer workshops and got into tin house, which i highly recommend if that’s something you’re interested in. at tin house i met my dream agent, who seemed really interested in my work and encouraged me to query her as soon as i had a book done.

a lot of personal drama happened that year. i was still working at the bank in addition to teaching a 2/2 and taking a full course load. in summer i had a long overdue mental breakdown.

2017 was a rough year. i wrote 149k. this is the year i started keeping a dedicated expenses spreadsheet. i spent $174 in submission fees. tin house tuition with room and board was a little over $1500 + travel. i thought it was worth it because i met the agent i thought i would later sign, but that didn’t pan out. (i made some great friends though!!) tin house was definitely an unwise financial decision; i paid for it out of what little i managed to save in 2015.

2018, age 28

early in 2018, i went from teaching comp/rhet to creative writing, which only cemented my desire to teach writing as a career. i realized i was far better at teaching writing than writing, but i knew i had to keep writing to keep teaching (shocked pikachu.jpg), so i kept submitting to journals. i got my first story accepted. i didn’t receive any payment for that publication. i quit the bank early in the year (finally! after 10 years!) and was terrified about money, in part because my student loan payments were coming out of deferment and i was still paying off my hospital bills from my breakdown.

in spring semester, i won a few departmental awards (totaling $500ish) and got a second story accepted (again, no payment). i also got accepted to another workshop which i will not name because i hated it. i graduated in may and defended my thesis in july. the thesis would later become my short story collection, zucchini.

in fall, i stayed on at my school as an adjunct, and started writing training wheels which would later become an original novel called baby.

i wrote 450k in 2018. i paid $373 in submission fees. i was also nominated for an award for one of my publications but didn’t win. the workshop i went to was like $4000 with room and board (it was a month-long workshop). i got 75% of it covered with scholarships and i paid for the rest of it out of my savings, and even though i’d intended to drive there, my mom ended up buying me a plane ticket. again, i met a lot of big-wig writers i thought for sure would help me get an agent. i told myself i was networking, and that publication was all about Who You Knew. but that turned out not to be true for me.

as an adjunct i made $3200 per course, and i taught 3 classes in fall. in winter, i got my shit together and started applying for creative writing PhDs, mostly to convince my family i was doing something with my life, with no expectation that i would get in. in winter i applied to 2 schools. with application fees and the GRE, i ended up paying well over $500.

2019, age 29

in spring semester, i taught 2 classes while i revised training wheels into baby. when i had a completed manuscript, i finally pulled the plug and used all my networking contacts to get my dream agent i’d met at tin house. i queried her, and a very popular and well-regarded author i’d met at the other workshop emailed her on my behalf to tell her good things about me. i thought for sure i had it in the bag. this author also touched base with a few other agents whom he thought would like my work.

i didn’t hear back from any of them. not even a “no thanks.” i set down querying for a while.

i got a third story picked up and published around this time, and i was paid $25 for it. they also nominated me for an award, and i don’t think i won? but i can’t find out who did win so idk.

my grandpa passed away and i decided to sell my house and move in with my grandma so she wouldn’t be alone. i got rejected from both PhD programs i applied to and decided to get a “real job” instead, and began applying for random positions that offered health insurance, because i knew i was drastically undermedicated and it was becoming a Problem.

near the end of spring semester, i moved out of my house, put it on the market, and was interviewing for a community development manager position for a nonprofit. at the same time, i found out about another university that was taking late-season applications, and i applied. five days later, i got accepted. one day after that, i got a job offer for the nonprofit. since i had no idea how long it would take for my house to sell, and being unable to afford both rent in a new city and my mortgage payment, i deferred my PhD acceptance for a year and decided to work at the nonprofit for a while. the risk was that i could only defer my admission, not my funding, so there was a chance that the following year i wouldn’t get the same funding package.

i lasted one month at the “real job” before i had another breakdown and ended up quitting.

my house sold for well under the asking price and i received only $4000 in equity once it was all said and done. that’s a lot of money to me, but considering that i’d been paying on the house for 7 years, i was expecting a lot more.

i had a year to kill until the PhD so i decided to take a break from teaching and apply to artist residencies instead. i applied to 8 residencies and got accepted into 4, but only ended up attending 3, because the 4th was outrageously priced and there was no indication of the cost when i had applied.

in winter i picked up querying agents again. i queried 10 agents every other week. i also got a ghostwriting gig writing children’s books that paid $800 a month.

in 2019 i wrote 417k. i spent $441 in submission fees (to residencies and contests, not agent queries. never pay money to query an agent!!). i ended up teaching 3 classes fall semester.

2020, age 30

i started out the year driving across the country going to residencies. the first cost $100 (no food), the second cost $250 (A LOT OF VERY GOOD FOOD), and the third paid me $500. i was at the third when the pandemic hit.

the query rejections started rolling in. i gave up in february after 60 queries. of those 60, i received 7 manuscript requests for baby, but the consensus was that it was too long and plotless (you got me there.jpg). at the second residency completed and revised zucchini and decided to begin querying with that instead. i could only find a few agents who accepted collections so i only queried 16. i got one request for the manuscript but then didn’t hear back. i gave up in april shortly after the pandemic hit.

when i figured the collection, like the novel, just wasn’t publishable, i started submitting to contests which is the more standard route for the genre. i submitted to 12 in total and was a finalist in 1. i was rejected or withdrew from the rest.

the PhD program reached out to ask if i was still interested in starting in fall, and i said i was, so they put me in the running for funding again and i was accepted. the stipend was $17k per academic year.

like most of us, i got totally derailed in spring and stopped doing basically everything. the ghostwriting gig started paying $1500 a month and i also started my creative coaching business, which slowly but surely began to supplement my income. i also received the $1200 stimulus.

when school started, i quit the ghostwriting gig. i had no intention to continue querying either book, but i saw a twitter pitch event called DVpit (diverse voices) and decided to participate. for those who don’t know, a twitter pitch event is where you tweet the pitch for your book and use the hashtag, and agents scroll through the tag and like tweets. if an agent likes your tweet, you query them.

i got one like, so i followed up with the query. the agent asked for the full MS and a couple weeks later followed up with the offer for representation. we talked on the phone, she sent me the contract, i asked for a couple changes, and then signed!

so far this year i’ve written 375k and paid $518 in submission fees. i’ll give more details when i do my end of year roundup next month. oh, and i finally paid off my student loans.

totals

word count: 2.3 million

agent queries: 77

agent MS requests: 9

agent rejections: 28

agent no responses: 44

short story submissions: 86

short story acceptances: 3

short story income: $25

total submission/application fees: $1472

my (final) query letter

honestly this query letter probably isn’t very good which is why i got such a minimal response, but it got the job done eventually.

Thank you for expressing interest in ZUCCHINI through this year's DVpit event.

ZUCCHINI is a collection that views sex through an asexual lens. It poses inquiries into constructs like gender, sexuality, and love to dissect the patriarchal/puritanical foundations from which our social perspectives often derive. Being a collection about asexuality, each story portrays a relationship that develops from forms of attraction other than physical.

In one story, a grieving widow purchases her first sex toy; in another, a woman uses sex to cope with the death of her abusive father, and later in the collection faces the long road to recovery; an administrative assistant seeks out a codependent relationship with her boss; a masochist hires a professional sadist to lead him toward self-actualization; a woman begins to recover from her sexual assault by staging a reenactment on her own terms; and lastly, two lifelong friends in a queerplatonic relationship decide to get married. Asexuality is an under-acknowledged identity within the LGBTQIA community and is often misunderstood. In seven stories, ZUCCHINI dissects the notion of attraction, explores the intersections of sexual identity and trauma recovery, and conveys the experience of intimacy without physical desire.

Three stories in the collection have been published in literary magazines. “Lien” appeared in volume 24 of Quarter After Eight and was nominated for the PEN/Robert J. Dau Short Story Prize for Emerging Writers. “An Informed Purchase” appeared in the summer 2018 issue of Midwestern Gothic and won the Jordan-Goodman Prize in Fiction. “The Ashtray” appeared in issue 16 of Rivet Journal and has been nominated for a 2020 Pushcart Prize.

Complete at 53,000 words, ZUCCHINI is a collection in conversation with Carmen Maria Machado’s HER BODY AND OTHER PARTIES, Lauren Groff’s FLORIDA, and Samantha Hunt’s THE DARK DARK.

If ZUCCHINI is of interest to you, I would be happy to send you the manuscript. Per your guidelines, I've appended the first twenty pages below, which is the entirety of the first story.

what comes next

i’m going to spend january revising the collection per my agent’s feedback. when i send it back to her, she’ll shoot it out to the first round of publishers. my understanding is that the goal is to get multiple offers on it so that it has to go to auction. if there are no offers, she’ll do another round of submissions, and so on, until we’ve exhausted our options. if that happens, we’ll reassess, but by then hopefully i’ll have another novel finished.

meanwhile, i’ll be continuing the PhD which entails teaching a 2/2, workshop, and 2 lit seminars per semester. i’m also still doing my creative coaching, writing fanfic, and working on my original projects. in summer, i’ll finally be moving to hopefully start going to school in person next fall.

the PhD is a 3 year program with an optional fourth year. i don’t see myself finishing in 3 years so i do plan to take the extra year unless something comes up. after the PhD, i’m not sure what i’ll do. a lot will probably change by then so i’m trying not to commit to one idea. i might apply to post-doc fellowships and tenure track positions, or i might leave the country and teach overseas, or i might move to LA and try to get in a writer’s room somewhere. i’ve got a lot of options.

overall thoughts/stuff i learned

first of all, you don’t have to go through all of this to publish a book. you could feasibly just write a book and query agents. the only reason it took me this long is because my PTSD brain was sabotaging me every step of the way and i didn’t start taking anything seriously until i found something i was willing to fight for (teaching). i went the MFA/literary route but other, faster routes are just as good. maybe better. probably better. actually if there’s any chance you can go a different route, you should take it.

reflecting on all of this, very little of it has anything to do with talent or being a good writer. nor does it have to do with being at the right place at the right time. i’ve only made it this far because i took very small steps over and over again, and during that walk met people who could help me -- the authors who have mentored me, the editors who accepted my stories, the agent who signed me. and as i got further along my path, i started being able to help other writers in the way i was helped.

i don’t believe i’ll ever be a great writer. the best thing i can say about my writing is that it’s competent and accessible. everything i write sets out to do something and most of the time it gets the job done. i don’t imagine i’ll ever be able to financially support myself with publishing, and i’ll certainly never be famous or well-known, but i’m good enough to keep making progress. i’ll probably continue to find opportunities that are adjacent to writing and that will keep me afloat, pending my health and provided the country doesn’t devolve into civil war.

probably the most important thing i learned in all this is that having a wide appeal isn’t the goal. you don’t write to be lauded or liked. you have to stay as true to yourself and your interests as you possibly can, so that the people who come across your path can see you and help you. you’ll need those people; no one gets anywhere alone. if you pander, if you’re too concerned with praise and success or being adored, you won’t make it very far. the rejection will eventually kill you.

with all that said, my advice to you is this: never stop writing. the ability to share our stories is the single most precious thing we have. you can’t let anything stop you from telling your stories the way you need them to be told.

95 notes

·

View notes

Text

*** disclaimer: this is a very long diary type of entry that is probably quite boring for everyone else and may be ignored. it's merely a very lenghty epiphany I just had about my life and myself and I had to type it out for me, to lock in the thoughts, if you will. it was pretty therapeutic tho. 🙃 ***

10/Sept/2021

I just had the realization that I'm in the process of redefining every aspect of my self and my life.

I quit smoking cigarettes from one day to another exactly 2 months ago tomorrow and went from a heavy to a casual party smoker.

I rarely ever smoke weed anymore (plus when I did since quitting tabacco, I rolled with herbs) and now made the conscious decision to take another long break, so it doesn't interfere with my weight loss again. I get the worst munchies and have no self control when I'm stoned. I'm talking "5000+ cals in one sitting" type of binges. I'm not tolerating this kind of self sabotage anymore.

I re-discovered edblr. Yes. I know. Not the healthiest habit to get back into but it's the only thing that has actually helped me gain the motivation and willpower to put a stop to my raging sugar addiction and instead, an actual effort into losing weight again. Besides, I'm doing it in a much more careful and "responsible" way now (high restricting, taking supplements, no strict/exact calorie limit, very light to no exercise (okay, to be fair the reason for that is mainly my injured knee but still), letting myself eat/drink more than planned if I feel my body needs it). And let's not forget that I've literally been binging every day for the past 2 or 3 months. My diet nearly exclusively consisted of chocolate, pastries and pizza. Literally. I've gained 10 kgs (22lbs) during that time. That lifestyle was just as unhealthy, if not unhealthier.

I finally got to hang up and use my calender. Due to my ADHD (self diagnosed for now), I'm very forgetful and unorganized - at least in my private life. That's why I made the decision to get a big calender which I can use as a semi To Do/Buy list and appointment/meeting/bill reminder. Since I'm glueing a sticker to each day I got through without binging, I'm looking at it pretty much every day anyways. Plus, it's a motivater to not binge (reward that inner child)! Overall, it's helping me become more organized and put together which are two areas I've been lacking in in the past years. So far, I've been mostly using my phone notes but I usually write something down and immediately forget about it if it's not a grocery list or a To Do list I'm actively working through on that same day.

I have my first appointment at a psych ward since I was a teen. It's just a phone call and first get to know conversation but it's better than nothing and more than overdue. I'm finally taking the first steps towards getting diagnosed and being eligible for therapy. I'm sick of feeling like a victim of my own brain, I just want to be better. I deserve to be better.

I'm hungry for knowledge again. I deleted Tiktok from my phone because of how big of a distraction it was and because I realized that even though I'm being bombarded with new information everyday, I'm not learning anything. Our brains can't even comprehend the amount of information given in that short time span. Nothing sticks. Sure, you find out about some pretty cool stuff on TT depending on what kinda fyp you have but for me personally, it was just hours and hours of mindless scrolling in the end. It's crazy how addictive it is, too. Even despite the fact that I was already at a point where it didn't even give me that quick dopamine quick anymore. It felt boring and repetitive and I was merely doing it out of habit.

So, I got rid off the app. I started watching documentaries again. Mostly about gut health and mental illnesses like ADHD, Autism, BPD, Narcissm etc. Like TED talks or interviews/discussions by and with professionals/experts/diagnosed people. I'm back to not just craving but actually consuming something with substance, something that gives me more knowledge and insight on a topic. Something I actually want to know more about.

I realized and accepted that even though I am a creative mind, a fully creative job might just not be for me. I'm learning that maybe I'm the type of person who does something entirely different in their free time than what they do at work. And that that's very much okay. I noticed that at my job (this was the case for every job I ever had), my mind seems to work differently. When people expect me to do something, I have the needed pressure and motivation to get it done. I could also observe in myself that at work, I enjoy organizing/sorting stuff, I'm a fast and independent learner while I'm also excellent at training new employees, I'm much more detail oriented than in my private life - overall, it came to my attention that I might not actually be the ever chaotic forgetful mess who can't form a logic thought - or I can at least recognize that this is merely a part of me and not what defines and limits me as a person. I realized I actually like straightforward work, I like working alone and I like working precisely. When I was younger I would have never used any of these traits to describe my dream career. I would gag at the idea of working an office job and now I feel like this would actually suit me very well. Especially the working alone part would mean feeling less drained at the end of a work day and still having the energy to hang out with people I actually want to see. This is an extremely valuable lesson about myself that I finally seem to have learned.

After this big sub- and now concious evaluation about myself I'm also finally taking actual steps towards a possible career. I bought a course and worked through the first 2 lectures today, taking notes and writing everything down neatly for 3 - 3 1/2 hours (in total with breaks in between). I even got a notebook specifically for this new life project. I'm excited to learn. I feel scared, too. This is something I've never done before but I'm telling myself that trying won't hurt. I have my main job as a safety net, financially nothing can happen to me. I can only learn, even if I fail. And time will pass anyways, whether I get my ass up and put in the work or continue to be unhappy with what I'm doing without trying to change anything.

Speaking of finances, I also started taking those more seriously now. I stopped using my credit card (I was in negative numbers constantly, big numbers like -300 to -800€ due to constant overspending). I set up standing orders for my monthly fixed costs to make sure bills are always paid on time. Due to my forgetfulness and ADHD freeze I would often forget to pay or postpone paying bills until the reminder came in the mail and led to me having to pay on top or generating debt. I still have a little bit of debt to pay off but it's thankfully not a dramatic amount. I also have a second bank account for savings now where I transfer 200€ to every month. Even the simple act of calculating my fixed costs to see how much I can use for what was something that was desperately overdue. What I still have to do is sort out my receipts and write everything down in a housekeeping/budget book. And my first ever tax return. I am very much dreading both of these. 😃

Anyways. Wow. I really needed to type this out. I have the very harmful tendency to look at all the negative stuff and only focus on what I don't have and don't do. I really needed to take a long, deep look at all the things I've been changing around in the past couple months. A lot of it really passed me by until now. It's crazy but I really feel like a complete failure when my body isn't looking its best and it makes me blind for everything else. So, thank you to myself for reminding me that I am actually making a lot of progress, even if it has been in areas other than my fitness and looks. They're just as important (from a healthy brains point significantly more important, obviously) and deserve to be noticed and celebrated.

Conclusion: ❤️✨YAY, ME✨❤️

8 notes

·

View notes

Text

Good News/Bad News

Okay. Good news first! The car is fixable, and it’s not as bad as we expected it was going to be ($300 for the better parts and labor included, which is making me think we got lucky and there was no damage to the rotor). So this left us with $400 after we had spent money on food and stuff. We had paid the utility bill earlier in the week, and I just paid my credit card bill (which will give us one or possibly two tanks of gas later in the month) and put $100 towards paying off the rest of our car insurance for the year.

Bad news? We can’t move the old unit into the new one until next month, and I can only afford to pay the old unit once we cover our rent tomorrow. I also won’t have gas for visits for most of this month with my son, money for the cable bill nor (on a more superfluous note) any money to do something for my birthday. I also need to start paying for my prescriptions again, which is not fun.

We need $400 to cover the new unit and the cable, and another $60 - $120 for gas (though as I said, I should be able to cover two $50 tanks if my math is right). Any help at all would be amazing. We’re prepared to pay the cable late since it’s not due until the 22nd and we can pay it late, but we need to move stuff to our new unit from botht he old unit as well as the apartment so we need to pay it ASAP..

Any help can be directed to [email protected] via PayPal or by clicking this link. Thank you very much for any help or reblogs you can give!

158 notes

·

View notes

Text

A Trip to the Mainland (Taiyuu cooking event) (?)

@taiyuu-high-oct

A Train from Taiyuu Island to Mainland Japan took a couple hours, hours of ocean, boredom and more ocean. Staring at the TV, Zeke remembered a time before Taiyuu, before Japan even.

----------------------------------------------------------------------------------------------------------

A small town on the coast of Germany, a large building, a small apartment.

A teenager enters, around 17 years old, wiping his feet and looking around, the clock reads 8pm. He spotted his younger brother in the living “room” by himself watching cartoons. The younger one couldn’t be older than 9.

“Hey, kiddo. Where’s Mum?”

“She got called into work.”

Frustrated in his mother’s irresponsibility and lack of note, the older brother tried to keep the conversation going as he made his way to the kitchen.

“Whatcha doing?”

“Watchin TV.”

“Oh, so you found the remote?”

“No.”

Flick. The channel changed.

Opening the pantry the older brother found… half a loaf of bread and a whole lot of empty space.

“Have you had anything to eat yet?”

“No. Mum was gonna get groceries but she got called into work.”

Biting his fist in frustration, the older brother pounded the pantry door with his head. Silently seething in anger the older brother put on a happy face, the older brother came out and sat next to the younger brother.

“Let’s go out for dinner tonight, just you and me.”

“Won’t Mum and Dad get angry?”

“They’ll never know, I got a little extra money from work today.”

“I mean… sure.”

“Alright, get your stuff ready and we’ll leave in a few.” The older brother wrote a note for their Mother, if she returned home tonight.

When the two got ready and were almost out the door, the younger brother stopped.

“Umm... Schlaut?”

“What’s up Zeke?”

“Are you sure Mum and Dad won’t find out?”

“Hey, we’ll leave our trash in a public bin, they’ll never know.”

-----------------------------------------------------------------------------------------------------------

Finally on the Mainland of Japan Zeke had a couple trips to make.

The first stop for today was to withdraw money, but look like a cool guy, Sunglasses on. Wandering around the Whatever City, Zeke can’t remember what it’s called, he started to get his bearings.

‘Alright, grocery shop’s there, post office’s there and-’

Zeke felt a rumble down to his core.

‘It’s going to be a thunderstorm tonight.’

Finally finding an ATM in Whatever City, that took forever. Taking his “Credit” Card out Zeke approached the ATM, noone was nearby anyway but he still felt he had to play the part.

Feeling the ATM Zeke felt all the different compartments, searching for the most used 4, Zeke found what he needed.

Trying the first one: Whirr, Zzzt And Dispense. 1000 Yen, not quite what he needed.

Next compartment: Whirr, Zzzt and Dispense. 5000 Yen, close but not the notes he needed.

The Third compartment: Whirr, Zzzt and Dispense. 10,000, exactly what Zeke needed.

Grabbing an extra 13 10k Yen bills Zeke had enough to pay for his tuition, with some left over.

That wasn’t right, only take what you need. Zeke remembered when this all became second nature to him, why quickly searching these machines became so easy.

-----------------------------------------------------------------------------------------------------------

“That’d be 50 Euros sir.” A cashier lady, in a large mall grocery store.

“I’m really sorry, can you wave it just this once?” Schlaut, now at the age of 19, pleaded to the cashier holding a 20 Euro note.

“I’m sorry sir, if you couldn’t afford it you shouldn’t have picked it up.”

“But this is all we have for the week, we’ll go hungry without this food.” Schlaut

“Then get 20 Euros worth of food or get out of the store.”

“Fine. C’mon Zeke we’re outta here.” Zeke, now 11 years old, followed his brother out of the store.

“What’s the plan now Schlaut?”

“I dunno kiddo, we’ll figure something out.”

It wasn’t long into the usual walk home when they walked past an ATM, it’s screen illuminating the sidewalk. The screen flickered strange colours, reds, blues even a neon green. Schlaut paused, did a slow turn on his feet and paced to the ATM.

“Zeke?”

“Yeah Schlaut?”

“Are you doing that?”

Zeke’s stiffened and he turned his face away from his brother.

“Zeke look at me.”

Zeke reluctantly looked at his Older Brother, the pupils of his brown eyes glowing a slight blue.

“Did I do something wrong?” Zeke was looking at the ground in shame.

“No no no no nononono nono, no Zeke. You did something very, very right.” Schlaut hadn’t felt this excited in a while.

“Let’s play a game Zeke, see if you can find some paper in this machine.” Schlaut pointed to the ATM.

“You mean money, isn’t that stealing?” Zeke was willing to do this, but he wasn’t very happy about it.

“Hey, we’re only going to take what we need ok? No more. We’re not villains, we’re survivors. See if you can find a 20 note and a 10 note.” Zeke had found a way to save us!

“Ok. I’ll try.”

-----------------------------------------------------------------------------------------------------------

Returning back to the present Zeke held about 2000 Yen too much in his hands. The fridge at Taiyuu was running low, this money seems appropriate for everyone to use.

Zeke went to that small grocery store he passed by earlier. Fresh fruits and vegetables, that’s what Taiyuu needed, none of that instant shit. Apples, carrots, broccoli and one pack of the cheapest Cup Noodles he could find.

‘How would the others at Taiyuu react? I don’t think Sako or Spellman would be particularly fond of me anymore. Ah well, they won’t find out. All the years of pulling this same stunt we were only found out once.’

Zeke paid a total of 1962 yen.

“Have a good day.”

“Yeah, you too.”

‘Only found out once.’

Supermarket (Schlauts Quirk)

-----------------------------------------------------------------------------------------------------------

“How’s that Zeke, just enough to get us through this week. Mum should have the day off tomorrow so we’ll cook a whole bunch then.” Schlaut, now 21, said to his brother Zeke, now 13.

“Yeah, maybe Dad’d have time to help as well.”

“I doubt it kiddo.”

RUUUUUUMMMBBBBBLEEE

“We should get going before it rains, seems like a storm is brewing.

Off they were on the usual walk home, Through an empty courtyard, groceries in hand. Not too much, just enough to get by.

“Hey Asshole!”

Schlaut turned, almost like he was expecting this.

“Yes, Gregory?”

A potbellied man, more of a sphere than a man, called out to the two.

“You mess with one of us, you mess with all of us.”

“Us?” Zeke panicked.

“There’s about 4 of them, stay behind me Zeke.”

“What, who are you talking about, how do you know these people?”

“It’s complicated. You wouldn’t understand.”

3 other men came up from behind the Sphere Man. One looked too long to be normal, another looked like a leaf man, the last one had spines coming out of his back.

“Yeah, not so tough are ya now there’s more of us.” Sphere man said, he sounded like he was from New York, which is weird because this is Germany.

“Huh, Good one boss.” The Leaf Man said, he had a very deep voice.

“Yeah, good one boss.” The Spine Man said, he had a very snively voice.

“Hehehe, heheh hehehe hehehe” The Long Man said, he had a very creepy laugh.

“You made it easier for me.” Schlaut butted in, sounding far too confident for a 4 on 1 fight.

RUUUUMMMMMMMBLLLLLLEEEEE

Long Man reached over and punched Sphere Man in the face.

“Aaaah, Tony, whaddya doin? Hit him not me!” Sphere Man was both confused and angry

“Heheheh, heheh, Hehehehhe!” The Long Man’s laugh seemed very panicked and confused.

Leaf Man punched Spine Man, Spine Man grabbed Long Man. It was a free for all, none of the assorted goons and henchmen ever came near Schlaut and Zeke, Zeke leaned over Schlauts shoulder.

“What are they doing Schlaut? Why are they here?” Schlaut looked back at his younger brother.

“Don’t worry, Zeke, they’re taking care of it themselves.” Schlaut looked at Zeke for a moment, just one moment was all it took for Zeke to notice the slight red glow from his brother's pupils.

It wasn’t too long before the four strangers were all on the ground unconscious. Not once did the 4 even take a step towards the Funkee brothers.

“Let’s go Zeke, it’s all taken care of.”

“But… but-”

“Let’s GO Zeke.”

RUUUUMMMMMMMBBBBBBBBBBBBBBBLLLLLLEEEEE

They turned to continue on their way home, when Zeke heard skidding. No. Rolling? Turning around in curiosity Zeke saw Sphere Man rolling towards them, like a ball. A very angry ball.

“Schlaut, look out!” Zeke jumped, panicked and….

FLASH

BOOOOOOOOOOOOOOOOOOOOOOOMMMMMMM

-----------------------------------------------------------------------------------------------------------

Not done for the day yet, still gotta send a letter off to Mum back in Germany, quick visit to the Posty and back to Taiyuu. Card, letter, shipping. Totaling 300 yen, that is cheap!

Hey Mum,

Taiyous Taiyuus going great, i think im really hitting it off with everybody here. This place seems more my style than uA anyway. Theres a whole bunch of really weird people here. One person can even shapeshit shapeshift!

Anyway hows things with you, hows the new job in France?

Has Schlaut come back yet?

Love,

Zeke

“Just one letter, wouldn’t a text be better?” The teller was confused.

“It’s just a little tradition we have. Notes and written things are easier to keep anyway.”

Zeke made his way back to Taiyuu, hours on the train, again. The news reports were going on about a villain by the name “The King”. Luckily Taiyuu covered the costs of going back to Mainland Japan. Making his way back to the kitchen area Zeke deposited the fruits and veggies into the communal fridge. However, Zeke kept the Noodle Cup.

Zeke set the kettle to boil and thought of the day everything changed, the day Schlaut left. There was no bang, there was no warning. Around when Zeke was 13 Schlaut just, poof, gone. The whole family thought he was dead for months until Zeke’s 14th birthday, where Zeke got an RC car, brand new and very high end. It came with a note.

Hey Kiddo, Happy Birthday. Sorry I couldn’t be there this year

Noone ever really bothered Zeke again, of course Zeke still had his friends but noone bullied, assaulted or even annoyed him again. The icecream place even gave him a discount. Teachers were a whole lot nicer, even recommending him to hero courses like UA: LA, Shiketsu and Seijin. That was 2 years ago.

The screech of the kettle brought Zeke out of his thoughts. Filling his Cup Noodles with boiling water Zeke had made a shitty meal at Taiyuu.

BOOOOOOOMMMMMM

“Ow ow ow ow ow ow ow hot hot hot hot hot hot hot hot.”

Maybe not.

5 notes

·

View notes

Text

So back in December my father took his medication, one pill got stuck in his throat and that’s where it dissolved. After that, he began having throat pain and was told it was an ulcer. Towards the middle of January, he began having jaw pain, and was told it was an abscessed tooth, that was the final push he needed to get all his teeth removed and have dentures. Only the pain never went away, it spread to the back of his head. He went to the doctor and was told he has a lump pin his neck.

He got an ultrasound and turns out this lump was strangling his only functioning carotid artery, which was causing the pain in his head. The next week he went for a CT scan and it found 3 large, potentially rapidly growing masses in his neck, two near his carotid and one over his voice box. He’s in such extreme pain he can barely eat, but his next doctors appointment is on March 15. I’m the kind of person who’s mind goes straight for the worse case scenario, which would be fatal cancer. I don’t want him to die, but I’m thinking about what’s going to happen to my mother if he does. My mother is early stages Alzheimer's or dementia.

To say my dad is a financial clusterfuck is putting it lightly, this man was raised with no financial responsibility and still has none. When I was younger, my mother talked to him about getting life insurance and his response was “why would I get that? I’ll be dead and have no need for it.” And that’s the attitude he’s had. He is irresponsible at best. My mother finally paid off the mortgage of the house and my dad took another high one out on our house without telling her. He has about $20,000 of debt on his credit cards, bought 2 $15,000 cars that he’s paying off, and just took out another loan, on top of bills that we have to pay. To add to this, my dad’s accountant pulled some shady shit on our family’s business for the past four years without our knowledge, because my dad trusted him so much he let the accountant take care of it, and now we owe $235,000 in penalties and back taxes, something we could pay off if we tighten our belts for the next 6 or 7 years. On top of this my dad wants to spend another $18,000 to buy a backhoe that he’s wanted since before I was born, and to be honest, he can use it for work but most likely it would sit in our back yard and rust. I have about $200,000 in debt and a low paying job. With my student loan payments $2,000 a month and a medical and car payment for $300 each I can’t afford rent, groceries, or anything. This is why when I moved back with my family to take care of my parents they said helping them with everything would be my payment for rent and etc. No I'm terrified my mom will lose her house and everything in it because of the bills that will come if my dad dies. I have no one to talk to this about so I’m just writing to vent.

0 notes

Text

The Money Hack for Using the Local Coinstar for FREE

Is it just me or do you love cashing in your coins?

It always feels like free money since I’m never actively thinking about cashing in my jar of loose change. Only once my jar is full and heavy, do I realize that it’s time to finally empty and collect my money.

If you’re like me, you’ve probably asked yourself (or Google), where are the coin machines near me?

However, during your research you may find that Coinstar charges a whopping 12% in fees!

Ouch.

Lucky for you, we have the answer to avoiding Coinstar fees altogether.

Table of Contents

Avoiding the Coinstar Fee

What is Coinstar?

What are the Coinstar Fees?

The Hack to Avoiding the 12% Coinstar Fee

Donate Your Cash With Coinstar

Charities That Partner with Coinstar

How to Use Coinstar

Now, Is Using Coinstar Safe?

Finding A Coinstar Near Me?

Why Use Coinstar?

The Future of Coinstar

The Banks

Banks That Accept Rolled Coins

Credit Unions

Other Ways to Use Your Spare Change

Acorns App

Self-Checkout to Pay for Normal Items

Find and Sell Rare Coins

Donate to a Local Charity

Final Thoughts

Maximize Your Change

Avoiding the Coinstar Fee

If you don’t feel like counting coins one-by-one and then rolling them in those difficult paper rollers, you may want to consider Coinstar as a great alternative.

What is Coinstar?

You know those giant green machines found near the checkout of just about every grocery store in America? These machines allow you to dump all of your loose change into them and then it will count your change for you in a matter of seconds. However, there is a fee associated with the convenience of the machine.

What are the Coinstar Fees?

Coinstar charges a convenience fee of 11.9%! That means for every $100 of coins you put through the machine, you only get to keep $88 of it.

Is it worth it to use Coinstar? That answer is completely up to you, but there is a hack to workaround those hefty convenience fees.

The Hack to Avoiding the 12% Coinstar Fee

If you want to bypass the high fees that come with using Coinstar, there are few hacks you need to know about.

Instead of choosing to get paid out in dollar bills, you can choose to get paid out in Amazon gift cards and bypass the fees associated with Coinstar.

The minimum amount to receive an Amazon e-gift card is $5.00, with a maximum of $1,000.

But, if you’re not an Amazon shopper like me, there is one last option if you’re in a location within a Wal-Mart and some other retailers. You can get your receipt and use the funds toward purchase at Walmart or participating store. While I didn’t see much info online I know I’ve personally used this option at Walmart and Kroger stores in the past.

Donate Your Cash With Coinstar

While the nearly 12% fees still eat most of us, Coinstar does offer another positive alternative to using their services. You can now donate your coins directly to one of the seven charities they have partnered with.

The best part? They don’t charge you the nearly 12% fee!

Not to mention you are donating to a cause you believe in. Plus, it’s a tax write off so it’s a win-win-win!

Charities That Partner with Coinstar

Here’s a quick summary of the main charities that Coinstar has partnered with:

Feeding America: A nationwide network with 200 food banks that help fight hunger in the United States.

American Red Cross: The American Red Cross is where people mobilize to help their neighbors in emergencies whether across the street or across the world.

WWF (World WIldlife Foundation): This charity helps stop the degradation of the environment to help protect and restore animals natural habitats

Children’s Miracle Network Hospitals: Children’s Miracle Network Hospitals raises funds and awareness for 170 member hospitals that provide 32 million treatments each year to kids across the U.S. and Canada.

United Way: Each donation helps fight for education, health, and financial stability for others in the community.

UNICEF: This charity works in more than 190 countries to save and improve children’s lives by providing health care, clean water, and nutrition.

Leukemia & Lymphoma Society: They are dedicated to finding more effective treatments and cures for blood cancers so patients can live a longer life.

Who knew that your spare change could be easily contributed to helping such great causes around the world? One thing to note, not all of the charities listed above are available on every kiosk. Make sure to check online to ensure you can donate to the charity of your choice.

Also, make sure to keep your receipt. Donations like these one are 100% tax deductible and want to keep the receipt for your future taxes.

Lastly, you might not have noticed that there is one other option besides an Amazon e-card or certificate. If you’re not a huge Amazon shopper or want to put your spare change to a good cause you have one other option.

How to Use Coinstar

Using Coinstar is pretty straight forward to cash in your spare change. At the kiosk, make sure to check e-gift card for Amazon, cash, or if you want to donate the money. Add your coins to the machine and wait until it is done counting them.

If you have any coins that aren’t accepted or foreign objects accidentally inserted, the coin dispenser will spit them back out in a slot below. Once the machine is done counting you will receive the cash, store certificate or Amazon e-gift card receipt.

Make sure to not lose that receipt it’s small and I’m not sure they have any way to help if you end up losing it.

Now, Is Using Coinstar Safe?

Machines never fail, right? Well, that’s not always the case. When using any coin machine there is always room for error.

A story ran back in 2016 about a TD Ameritrade kiosk being off by $44 off from a $300 total. That’s a huge amount of money you’re not getting back!

Coinstar does appear to be the leader in the coin machine industry and released this statement after people began doubting the coin machines after the 2016 ABC investigation. Here’s what they said:

“Its number one goal is to provide its customers with a satisfying and reliable experience…it has refined technology and implemented regular maintenance schedules to service, clean, calibrate and test the machines to ensure reliability and high accuracy levels…rigorous testing has delivered extremely accurate coin counting and more than 95% machine uptime.”

Finding A Coinstar Near Me?

You can find Coinstar machine at most grocery locations but make sure to check out their locations page here.

Here is a list of the most common stores to help you find a coin machine near you:

Albertsons

CVS

Kmart Super Centers

Kroger (This includes a ton of brands underneath it including Fry’s Food and Drug, Pay Less Super Markets, Ralphs, Food 4 Less, Foods Co, and others)

Lowes

Rays Food Places

Target Superstores (these are bigger than normal Target stores and include a full grocery selection as well)

The Food Emporium

Walmart

Why Use Coinstar?

After reading about cashing your coins in a bank Coinstar takes away a lot of the frustration by making it simple and convenient. You don’t have to roll up your coins and make a separate trip to the bank. You can save gas money and combine the experience with a normal trip to your store.

The Future of Coinstar

While Amazon e-gift cards and donations are great the options are kind of limited. Especially since they used to have 5-7 different e-card options until 2018. But Coinstar is about to roll another feature later this year that is a huge benefit for you.

Coinstar and Doxo announced a partnership in April of 2018 that will allow you to pay some of your bills with the kiosk. Through this partnership, you will be able to pay bills including utilities, phone, car loans, cable, certain types of insurance, and more. All of this will be done using your spare change at up to 7,000 Coinstar kiosks by the end of 2018.

Not to mention, Doxo is a huge company so you will probably have access to at least one or two monthly bills that you are already paying. Doxo has a crowd sourced directory of more than 45,000 local and national billers.

The Banks

Did you know that not all banks actually accept coins anymore?

Yes, a government-backed entity like a huge bank doesn’t always accept your legal tender! How crazy is that? Is it even legal? I didn’t go too far down that rabbit hole but this seems ridiculous.

While some banks do have coin cashing machines in the lobby, they are usually reserved only for account holders. Typically, you have to enter your debit card and PIN before it will actually allow you to get cash for your coins. Even if they do have a coin machine it might not always be free, even if you bank with them!

Then there are banks like TD Bank which charges you a fee to use the machine. It’s hard to believe it’s so much effort to get cash for your coins even at banks.

Banks That Accept Rolled Coins

As you can see the list of banks that don’t accept coins that aren’t rolled isn’t many! Most banks choose to only accept them if you have them properly rolled.

This usually means you have to buy the device to help roll or do it manually. Most of the banks will provide wrappers for free but some of the banks will still charge a fee!

1. Bank of America

No fees for Bank of America customers

No fees for non-Bank of America customers

2. Chase Bank

No fees for Chase Bank customers with an unlimited amount

No fees for non-Chase Bank customers until $200. Anything above there are fees which weren’t disclosed online

3. BB&T

Fees vary for BB&T customers. They are free for under $25; 5% for more than $25

10% Fees for non-BB&T customers (Yes, 10% at a bank!)

4. Cape Bank

No fees for Cape Bank customers

No fees for non-Cape Bank customers (and uncapped total amount unlike others on the list)

5. Citibank

No fees for Citibank customers unless you live in the state of Illinois in which there is a 5% of the total amount

No fees for non-Citibank customers unless you live in the state of Illinois in which there is a 5% of the total amount (Sorry Chicago readers)

6. Home State Bank

No fees for Home State Bank customers

10% Fees for non-Home State Bank customers. Yikes, might as well head to Coinstar or a credit union for that price

7. JBT

No fees for JBT customers

5%fees for non-JBT customers

8. Manasquan Bank

No fees for Manasquan Bank customers

5% Fees for non-Manasquan Bank customers

9. Shelby Savings Bank

No fees for Shelby Savings Bank customers

5% of the total amount for non-Shelby Savings Bank customers

10. U.S. Bank

No fees for U.S. Bank customers

No fees for non-U.S. Bank customers

11. Wells Fargo

No fees for Wells Fargo customers

No fees for non-Wells Fargo customers

12. People’s United Bank

No fees for People’s United Bank if you’re a customer

Unknown fees if you’re not a customer

13. Umpqua Bank (Pacific Northwest)

If you’re a customer they do not charge and coins don’t have to be rolled.

Unknown fees if you’re not a customer

If you don’t have any luck finding one of these locations near you, make sure to search for smaller banks and credit unions.

Credit Unions

If you’re not familiar there is a big difference between credit unions and banks, especially big banks like Chase and Bank of America. While banks have customers (and sometimes shareholders), credit unions are membership based. Once you get accepted based to the affiliation of the credit union you can become a member.

Credit unions tend to have more personalized service and don’t give you as much grief for want cash for your change! If you are a member, most of the bigger credit unions won’t charge you any fees. This is definitely one of the biggest perks of using credit unions!

And some credit unions have Coinstar type of machines that will allow you to give them your change without having to spend time rolling them.This is a huge time and money saver for you. Some credit unions do allow non-members to take advantage of their kiosks but they charge around 9-10%. Still a high rate but ultimately lower than Coinstar if you want cash.

Credit unions are also a great fit if you’ve had problems getting loans or credit cards due to a low credit score. They are much more likely to work with you than big banks.

If you don’t want the work of rolling your coins and finding a bank or credit union it’s time to learn about Coinstar.

Other Ways to Use Your Spare Change

If you’re not a fan of rolling coins, using Amazon, or paying 12% in fees, there a few lesser known options to best utilize your spare change.

Acorns App

Acorns is the free app that takes your spare change and not only saves it for you, but invests it for you using roundups from use on any of your debit or credit cards.

If you would like to see exactly how it works, you can check out our Acorns app review which explains in detail how Acorns works and why microinvesting is becoming wildly popular.

Self-Checkout to Pay for Normal Items

This is a method that you might love or hate. Personally, I always get frustrated when people using self-checkouts and are slow. To me, it kind of defeats the purpose entirely.

But, this method does let you save money so I understand. Instead of having to roll your coins for the bank or lose money to Coinstar, just pay for items with coins in the self-checkout.

You won’t have to pay any fees and can easily use self-checkouts at most grocery or retail stores. Maybe keep the total to a minimum not to hold up the line with $50 of spare change.

Find and Sell Rare Coins

I’ll admit this step requires a little more and is kind of a side hustle as much as anything else. Before you decide to use one of these options for your coins, double check to see if you have rare coins.

Sometimes you will be able to find coins that are of more value than the actual amount! Again, I want to preface that this will take more effort on your end and certainly not for every reader.

Here are some of the most common coins you can look for and potentially earn some extra money:

A buffalo nickel (this has a Native American and a buffalo on either side of the coin)

A penny made before 1982. This means the coin is 95% copper and worth more money!

A quarter, nickel, or dime minted prior to 1964. If it is prior to 1964 that means the coin contains silver and worth more money.

Plus if you have any older coins you can always go to a dealer and see if they are worth more to you than sitting in storage.

Donate to a Local Charity

If you don’t want to make a separate trip to find a Coinstar or don’t like the limited options you can always choose to donate your change. Religious institutions, community center, and the Salvation Army are among a few that will accept your donations. If you have international coins from your travels some of these places will also accept them as well.

Final Thoughts

Back in the day, this wasn’t something you needed to ask. Instead, you could just go to your local bank, get cash, and go about your day. Sadly, it’s just not the case anymore when it comes to trading your spare change for cash.

While getting money is always nice, it’s getting harder and harder to get 100% of your change converted to cash. With banks, machines, and high fees, you normally only get a fraction of your money. A lot of cases you only get around 90% of your “free money” after expenses!

It’s a shame that banks and our financial system have made it so difficult for people to get money for legal tender. What’s the point of having a piggy bank if you can only collect 90% of what you save? Probably not a great example from our financial institutions to teach our youth.

Maximize Your Change

But there are some alternatives to help you maximize your change for the full amount. This article will help you minimize those fees and find the best ways to get started.

Start clearing out your couch cushions, car consoles, and every random area of your house. With these methods, you can finally start using that change for something you actually need!

In today’s digital world coins and cash seem to be used less and less. Inevitably you will end up with spare coins that you need to cash out eventually. Besides, it’s not like you’re collecting interest on coins that are scattered throughout your life.

There are plenty of options to get started. Whether you roll your coins and take them to your local bank or take the fees and use Coinstar. And for quick purchases at the grocery store you can always carry your spare change with you. While it is a little of bit of work, every penny counts when it comes to meeting your financial goals!

Hopefully, this helps you deal with coin machines, fees, and the other hassles when finding a coin machine. Make sure you remember to check your Coinstar in 2019 so you can use your spare change to help you pay for your monthly bills.

What method do you use for dealing with spare change? Do you prefer the old school method of rolling them or the convenience of Coinstar?

Let us know in the comments and happy free coin rolling!

Related Posts You May Like

45 Cheap, Fun and Easy Hobbies You Should Know About

150+ Freebies You Can Get on Your Birthday: Food, Retail, & Experiences

19 Ways to Get Free Gas This Year How to Avoid Those Free Gas Scams

The Money Hack for Using the Local Coinstar for FREE published first on https://justinbetreviews.tumblr.com/

0 notes

Text

The Money Hack for Using the Local Coinstar for FREE

Is it just me or do you love cashing in your coins?

It always feels like free money since I’m never actively thinking about cashing in my jar of loose change. Only once my jar is full and heavy, do I realize that it’s time to finally empty and collect my money.

If you’re like me, you’ve probably asked yourself (or Google), where are the coin machines near me?

However, during your research you may find that Coinstar charges a whopping 12% in fees!

Ouch.

Lucky for you, we have the answer to avoiding Coinstar fees altogether.

Table of Contents

Avoiding the Coinstar Fee

What is Coinstar?

What are the Coinstar Fees?

The Hack to Avoiding the 12% Coinstar Fee

Donate Your Cash With Coinstar

Charities That Partner with Coinstar

How to Use Coinstar

Now, Is Using Coinstar Safe?

Finding A Coinstar Near Me?

Why Use Coinstar?

The Future of Coinstar

The Banks

Banks That Accept Rolled Coins

Credit Unions

Other Ways to Use Your Spare Change

Acorns App

Self-Checkout to Pay for Normal Items

Find and Sell Rare Coins

Donate to a Local Charity

Final Thoughts

Maximize Your Change

Avoiding the Coinstar Fee

If you don’t feel like counting coins one-by-one and then rolling them in those difficult paper rollers, you may want to consider Coinstar as a great alternative.

What is Coinstar?

You know those giant green machines found near the checkout of just about every grocery store in America? These machines allow you to dump all of your loose change into them and then it will count your change for you in a matter of seconds. However, there is a fee associated with the convenience of the machine.

What are the Coinstar Fees?

Coinstar charges a convenience fee of 11.9%! That means for every $100 of coins you put through the machine, you only get to keep $88 of it.

Is it worth it to use Coinstar? That answer is completely up to you, but there is a hack to workaround those hefty convenience fees.

The Hack to Avoiding the 12% Coinstar Fee

If you want to bypass the high fees that come with using Coinstar, there are few hacks you need to know about.

Instead of choosing to get paid out in dollar bills, you can choose to get paid out in Amazon gift cards and bypass the fees associated with Coinstar.

The minimum amount to receive an Amazon e-gift card is $5.00, with a maximum of $1,000.

But, if you’re not an Amazon shopper like me, there is one last option if you’re in a location within a Wal-Mart and some other retailers. You can get your receipt and use the funds toward purchase at Walmart or participating store. While I didn’t see much info online I know I’ve personally used this option at Walmart and Kroger stores in the past.

Donate Your Cash With Coinstar

While the nearly 12% fees still eat most of us, Coinstar does offer another positive alternative to using their services. You can now donate your coins directly to one of the seven charities they have partnered with.

The best part? They don’t charge you the nearly 12% fee!

Not to mention you are donating to a cause you believe in. Plus, it’s a tax write off so it’s a win-win-win!

Charities That Partner with Coinstar

Here’s a quick summary of the main charities that Coinstar has partnered with:

Feeding America: A nationwide network with 200 food banks that help fight hunger in the United States.

American Red Cross: The American Red Cross is where people mobilize to help their neighbors in emergencies whether across the street or across the world.

WWF (World WIldlife Foundation): This charity helps stop the degradation of the environment to help protect and restore animals natural habitats

Children’s Miracle Network Hospitals: Children’s Miracle Network Hospitals raises funds and awareness for 170 member hospitals that provide 32 million treatments each year to kids across the U.S. and Canada.

United Way: Each donation helps fight for education, health, and financial stability for others in the community.

UNICEF: This charity works in more than 190 countries to save and improve children’s lives by providing health care, clean water, and nutrition.