#Fraud Risk Management Services

Text

Empowering Financial Security: BANKiQ's Advanced Fraud Risk Management Solutions

Unlock superior fraud risk management services with BANKiQ's advanced tools. Discover how BANKiQ leverages smart technology and AI-ML intelligence to enhance fraud detection. Elevate your financial security with BANKiQ's innovative fraud risk management solutions and strategies. Safeguard your assets with BANKiQ, a trusted leader in the realm of fraud protection services.

Visit: https://bankiq.co/

#fraud risk management services#fraud risk management solutions#fraud risk management strategies#fraud detection#fraud and risk management

0 notes

Text

Fraud Risk Management Services

Fraud risk management services provide a disciplined environment for proactive decision-making to assess continuously what could go wrong in fraud risks, determine which risks are important to deal with, formulate strategies for reducing those risks, and implementing the strategies to deal with those risks. Grant Thornton is the right choice if you are looking for the best fraud risk management services in India. We offer many advisory and consulting services, including business advisory, tax advisory, financial statement audit, and many more.

1 note

·

View note

Text

Flavorful Fraud Prevention: Crafting Effective Security Measures in Merchant Services

In the bustling world of merchant services, where digital transactions reign supreme, ensuring the safety of financial data has become a top priority. The landscape is rich with opportunities, but it's also rife with challenges. As businesses innovate to meet customer demands, so do fraudsters who seek to exploit vulnerabilities. In this dynamic environment, Oponinnovations emerges as a key player, revolutionizing security strategies and crafting robust measures to safeguard transactions and customer trust.

Understanding the Complex Terrain of Fraud

As digital commerce evolves, so does the craftiness of cyber criminals. From card-not-present fraud to phishing attacks, the techniques employed by fraudsters are increasingly sophisticated. It's imperative for businesses to recognize the evolving nature of fraud and adopt measures that stay a step ahead. Oponinnovations, a trailblazing technology solutions provider, take the lead in helping businesses understand the nuances of fraud and develop tailored defense mechanisms.

Embracing Cutting-Edge Technology

Oponinnovations knows that traditional security methods are no longer sufficient. The company leverages the power of artificial intelligence, machine learning, and data analytics to create a multifaceted defense against fraud. By analyzing patterns, detecting anomalies, and adapting to new threats in real time, Oponinnovations empowers businesses to thwart fraud attempts before they even unfold.

Securing the Customer Journey

The modern consumer expects a seamless and secure transaction experience. Oponinnovations realizes that security measures shouldn't hinder the user journey; they should enhance it. The company employs frictionless authentication methods that ensure customer trust while deterring potential threats. From biometric authentication to behavioral analytics, Oponinnovations crafts a security layer that's as unobtrusive as it is effective.

Adapting to New Norms

The COVID-19 pandemic brought about a rapid shift to online transactions, which in turn led to a surge in fraud attempts. Oponinnovations swiftly responded to this new normal, offering innovative solutions that address pandemic-induced challenges. By combining insights from global trends with cutting-edge technology, Oponinnovations helped businesses adapt to the changing landscape while maintaining the highest levels of security.

Collaborative Defense: Protecting the Ecosystem

Oponinnovations understands that the fight against fraud isn't a solitary endeavor. It requires collaboration between businesses, consumers, and technology partners. The company fosters a culture of shared responsibility, where information is exchanged, insights are shared, and a united front against fraud is established. This collaborative approach strengthens the entire merchant services ecosystem.

Continuous Vigilance and Learning

The battle against fraud is ongoing, as cybercriminals continually evolve their tactics. Oponinnovations instills a culture of continuous vigilance and learning among its clients. Through regular updates, educational resources, and insights into emerging threats, the company ensures that businesses remain proactive in their security measures.

A Trustworthy Partner in Security

In a world where digital transactions shape the future of commerce, security is non-negotiable. Oponinnovations stands as a beacon of trust, guiding businesses through the intricate landscape of fraud prevention. With innovative technology, data-driven insights, and a commitment to safeguarding customer trust, Oponinnovations empowers businesses to embrace the digital age with confidence.

Elevate Your Security with Oponinnovations

Flavorful fraud prevention is no longer a distant aspiration. With Oponinnovations by your side, your business can craft security measures that not only defend against threats but also enhance customer experiences. Discover the power of cutting-edge fraud prevention strategies and elevate your business to new heights of security and success. Learn more at oponinnovations.com and embark on a journey of robust protection and growth.

#business#finance#management#staffing#payment solutions#fintech#marketing#technology#business consulting#business strategy#fraud prevention#fraud#high risk merchant account#merchant services

0 notes

Text

Insurance Meets Blockchain

Insurance is an essential sector that helps people in difficult situations, and blockchain technology is changing the game in this sector. With blockchain, insurance companies can reap the benefits of faster payouts, cost savings, and fraud prevention while enhancing transparency and efficiency.

Do you think integrating blockchain into the insurance business is worthwhile? If so, connect with a leading blockchain consulting company for better assistance.

Keep reading to learn how blockchain technology drives growth and positive change in the insurance industry.

Blockchain Blocks False Claims

The insurance industry suffers significantly from fraudulent claims, leading to annual losses worth billions of dollars. Blockchain technology’s inherent feature of capturing time-stamped transactions with complete audit trials makes it difficult for fraudsters to commit fraud. Blockchain replaces authenticity certificates and stops duplicate claims, artificial replacements, and fake insurance claims.

Enhances Customer Experience

Insurance providers need to offer innovative solutions to win customers’ trust without compromising on price margins. Blockchain enables automated processing using smart contracts, where business agreements are built into the blockchain, and payments are auto-triggered when certain conditions are fulfilled. This way, customers can have a seamless experience while enjoying the benefits of automation.

Are you looking for an expert team to develop blockchain? Seek assistance from the best blockchain development company at affordable prices.

Improves Trustworthiness

One of the significant advantages of using blockchain in insurance is to create trust between different entities. Consensus algorithms built into blockchain allow immutability and audits, making creating smart contracts on the blockchain easier. Moreover, smart contracts enable timely, transparent, and trustworthy transactions, reducing fraud and making auditing more seamless.

Empowers More Automation

Smart contracts streamline the insurance process and enable transparent transactions. The entire insurance claims process works smoothly as the blockchain executes on the smart contract terms. Automation is a massive benefit for insurance companies, as blockchain saves time, effort, and money by lowering administrative costs.

Helps Collect And Store Useful Data

Blockchain collects usage data using artificial intelligence (AI) and Internet of Things (IoT) technologies. This data can be used to make informed decisions on insurance premiums and help monitor vehicles to qualify insureds for safe driver discounts.

5 Top Use Cases Of Blockchain In The Insurance Industry

Smart contracts eliminate the need for intermediaries and human intervention, reducing the risks of unauthorized manipulation and contract errors and increasing efficiency.

On-demand insurance is a flexible insurance model where policyholders can turn on and off their insurance policies with just a click. This model requires underwriting, buyer’s records, policy documents, and other stakeholders’ interactions, making it a perfect use case for blockchain technology.

Fraud detection and prevention can be significantly improved using blockchain technology to track and monitor high-value items like jewelry. This way, the insurance industry can avoid duplicate claims, fake replacements, and fake insurance claims.

Health insurance claims processing can be faster and more efficient using blockchain technology to store and share patients’ data between healthcare providers and insurance companies.

P2P insurance allows individuals to pool their risks and insure themselves without intermediaries. Blockchain technology can enable secure transactions and transparency between individuals, making P2P insurance a viable option.

Closing Words

Blockchain benefits to the insurance industry are numerous and significant. From fraud detection and prevention to enhanced customer experience, blockchain technology can bring about positive changes and growth in the industry. With the industry’s projected increase in the years ahead, now is the perfect time for blockchain developers to unlock the potential of blockchain and grow their businesses.

Get the finest enterprise blockchain development services from our experts.

#blockchain development#blockchain solutions#enterprise blockchain development#Impact of Blockchain on Insurance#Blockchain Development Services#Blockchain Development Company#Blockchain App Development Services#enterprise blockchain#enterprise blockchain development company#enterprise blockchain development services#custom blockchain development#End to end blockchain development service#End to end blockchain development Company#End-to-End Blockchain Development#Blockchain Insurance#InsureTech#Smart Contracts#Risk Management#Fraud Prevention#Peer-to-Peer#Claim Processing#Policy Management

0 notes

Text

#fintech#digital banking#embedded finance#financial services#open banking#decentralisation#digital transformation#customer onboarding#fraud prevention#compliance#risk management#cashless payment

0 notes

Text

“The vast majority of serious violence in our society is committed by men: 94% of murders and 98% of serious sexual assaults. So while the left and right variously emphasise the rehabilitation and punishment aspects of prison, its most critical function is public safety: keeping dangerous men out of society. Prison abolitionism is the ultimate luxury belief from those who don’t have to confront these risks.

However, prison can only achieve so much on this count. Not just because only some violent men are ever dealt justice; a tiny fraction of the number of rapes reported to police ever result in a conviction. Not just because the male prison estate itself is dilapidated and dangerous, impeding any theoretically rehabilitative effects it might have. But because many of these violent men pose a risk to society that extends long beyond their time in prison. Those convicted of the worst crimes have to go before the Parole Board before being released on licence – and its dreadful (now overturned) decision to release the prolific rapist John Worboys after serving just nine years shows it can get its assessments very wrong – but many are released automatically after serving half their sentence.

This is the first double injustice of the criminal justice system for women. Male violence against women and children is not accorded equal priority to other forms of violence. And although sex-based differences in patterns of violence mean it is vanishingly rare that a woman will genuinely be a danger to society, female offenders are treated as though they are violent men. Women’s prisons are crammed full of domestic abuse victims separated from their children, who have been convicted of petty crimes such as shoplifting, fraud and minor drug offences. Women who kill their abusive partners in self-defence or as a result of being under prolonged coercive control tend to get lengthy custodial sentences – and these have become longer over time, ironically as a result of policymakers wanting dangerous men to serve longer.

We know that experience of childhood trauma for boys is associated with a higher propensity to violence in adulthood, so any effort to reduce male violence must include more investment in children’s services. But there will always be some very violent men in society and it is naive to think they can all be rehabilitated with programmes such as anger management courses. They need to be monitored, managed and prevented from committing crimes against women and children. That’s why the failing probation service is one of the most important frontiers in the feminist fight to keep women safe from male violence.”

#radblr#femicide#feminism#male violence#radfems do interact#this is an abridged version go read the full article

344 notes

·

View notes

Text

Poisoned (Veneers Version)

The twins finish a day of work and community service at Vacay Island. As they sit in their room…something happens to Velvet. Veneer is noticing changes in his sister… changes that happened after using the Trolls essence… changes that he fear have left his sister to far gone.

Tonight, they stayed at Vacay Island.

Bruce designated a suit just for them. Velvet and Veneer spent the rest of the night in their room after a long day of work around the resort. Veneer exhausted himself on top of his bed, Velvet sat at there desk writing something… her back faced towards him.

“Not a bad day!” Veneer exclaimed with a smile on his face. “We even managed to make a few good extra tips.”

“This is slave work.” Velvet declared.

“Oh come on Vels! This is hard earned money we’re making now. And may I add we’re at least OUT here instead of rotting INSIDE a prison cell.” Her brother said. Velvet hissed…. Something was wrong, he figured, she had been much moodier lately. Veneer sat up to look at his sister.

“Everything okay, Vels?” Veneer was trying to be more open with Velvet again… to establish that relationship they once had. “….. Y-you know you can talk to me right?” His voice grew shakey.

“Oh really I can? That’s wonderful! Maybe you can tell all my secrets to the entire world while you’re at it!” She said in a scream…. She still didn’t face her brother.

“Are you still mad about what happened? I had to Vels… You were…. Changing.” Veneer admitted. “We had to get out…. And we did. The little Trolls… they saved us.”

“No! They ruined us! We had everything Veneer!” She stood up and faced him…..his heart sank.

“V-Vels….” He stammered…. He recognized that look… the pink pigmentation around her eyes…whoever this was now… it wasn’t his sister. He had to be careful.

“We were at the top! Everyone loved us!” Velvet yelled.

“… it wasn’t real though…” Veneer responded. “They were just responding to an effect the Troll had…y-you know that.”

“I don’t care! I had everything! Everyone LOVED me, ADMIRED me. I was it. I was popular. ME! And you took it away!” She screamed.

SMACK!

She hit her brother clear across the face, knocking him to the ground. Her nails left long, red mark from his eye down to the corner of his lip.

“Vels!” He cried. She hovered over him.

“They loved me Veneer. They loved me. Why did you have to take it away from me? Just like you took mom and dad’s love away with your stupid sickness! You ruin everything! Everything!” Velvet attempted to go for his neck, but he was quick to move. His sister lost balance and fell to the floor.

Veneer dared not turn around. He went over to lock all the locks to their suit…. Hoping it would prevent anyone from coming in and getting hurt at the fit of her rage. He then quickly ran to the bathroom and locked him self in.

Velvet pulled and pulled at the door.

“Coward! You’ve always been a coward!” She screamed as she pulled and pulled at the door.

Veneer sat in the deep most corner of the bathroom, hugging his knees, rocking back and forth.

“It’ll be over. It’ll be over.” He whispered to himself…. He noticed how his sister got angrier as time went on… this wasn’t this first… this is why he did what he did… why he admitted to the world that they were frauds… he could’ve lost his sister. But then he began to wonder, if he already did.

He heard a knock from the outside door leading into the room.

“Guys? Guys! What’s going on?” It was Floyd.

“Stay out, Floyd!” Veneer screamed loud enough for the little Troll to hear… he didn’t want to risk Velvet hurting Floyd or any of the other Trolls.

“Open the door Veneer!” His sister screamed as she shook and shook the door.

“Please, stop, please stop.” He whispered rocking back and forth as he hugged his knees.

“Velvet! What’s going on??” Floyd cried out again.

SNAP!

Velvet was able to break the door open… her pink pigmented eyes glaring down at Veneer…. There was actual fear in his eyes… this moment right here was all too familiar to him ….

“I’m going to break you!” Velvet said as she neared her brother. Veneer covered his entire face with his arms.

“Stop please, don’t hurt me! I’m sorry! I’m sorry!” He cried. At that instant something over came Velvet… the cry of her brother, the fear in his voice and eyes… the pigmentation around her eyes began to disappear. She blinked cluelessly at her surrounding, then down at Veneer.

“Ven?” She asked as she knelt down laying a hand on his shoulder. He shrugged her away, making himself into a tighter ball.

“Dont touch me!” He said, his face buried in between his knees. The door to their suit finally opened up, in came running the little Trolls, Gristle with the keys to the room in hand behind them.

“Whats going on in here?” Branch asked with Floyd at his heals. They all caught a glimpse of the red slash across Veneeres face..

“…oh my god…” Velvet whispered. Did she do that? She’d always rough Veneer up a bit, but never to the point where she would ever hurt him….what happened? Why? Why did she hurt him?

Veneer didn’t move. He trembled as he began to cry, not looking up at anyone.

“I…. I have to…. I have to go…” She said as she stood up and ran out of the room. Branch looked after her… then to Veneer.

The little Troll recalled that day he found Veneer standing at the edge of a cliff, unknowingly ready to throw himself off… something was happening… the twins had to be watched carefully.

“Keep an on him. I’m going to follow Vels.” Branch said as he ran off.

#dreamworks trolls#trolls band together#trolls 3#trolls veneer#velvet and veneer#velvet trolls#veneer#velvet#velvet and veneer trolls#fandom#fanfiction#fanfic#oneshot#au#poison

40 notes

·

View notes

Text

Tristan Rocha [FNAF AR, Renegade AU]

https://www.deviantart.com/paigelts05/art/Tristan-Rocha-FNAF-AR-Renegade-AU-1044234141

Published: Apr 21 2024

CK animatronic maintenance and R&D Robotics contract with Faz Ent has ended, but their stories are far from over.

Tristan is one of the two people who run R&D robotics. The other being Charles D, aka CD.

Tristan Rocha is the twin sibling of Daniel Rocha, so his story also started with Fazbear Entertainment, as their dad, Oliver Rocha, was one of the two technicians at Circus Baby's animatronic rental service back in the late 80's who had been ambushed by the animatronics, got strung up on the stages in order to trick the sensors, but survived thanks to the other technician, Morgan Smith, cutting himself and Oliver loose. Dan and his brother Tristan had only ever heard stories about Oliver's experience, and they knew that he wasn't exaggerating about what happened to Eggs.

Tristan wasn't surprised when Dan got into an accident in his first job at a factory, and after begrudgingly accepting the contract with Faz Ent, Tristan knew it was only a matter of time before he too would become the victim of a grizzly accident.

Knowing about the underbelly of Faz Ent since birth, he knew what to say and do to stay as under the radar as possible and reduce the risk of getting killed by an angry Exec, and when Ness started sending him newspaper clippings of an incident regarding the brother of an old Freddy's manager and information on the limits of the human body, he knew exactly what to expect. He also figured out how Faz Ent planned to kill Nora and helped her prevent it by removing the facial recognition from the toy animatronics that Faz Ent had intended on using against her.

He just didn't expect to get blindsided by magician mangle so soon after: he'd received blueprints and heard a whisper of Faz Ent's plans to kill his brother, but he'd had no time read the blueprint or tell anyone because as soon as he looked up, that's when the animatronic attacked him; it broke his bones and tried to cut him in half. The information he got from Ness regarding the limits of the human body saved his life, so whilst the animatronic left him on the brink of death and in a coma, he was able to survive.

He doesn't know how long he was in a coma for, only that something unusual was keeping him there. Whatever it was let him go though when his brother was wheeled into the hospital post "Adelaide Incident".

Seeing his brother heavily injured and missing a rib, Tristan knew that he'd woken up too late for what he knew about the plans Faz Ent had for his brother to be useful. But in learning about the Adelaide incident, Nora seemed to link Adelaide to the blueprint Tristan had received prior to getting attacked by Magician Mangle and she was able to warn Izzy and CD that Charles was likely in danger, and this heads-up actually saved CD's life, as Adelaide had immediately gone from trying to kill CK animatronic maintenance to trying to kill CD. So, so much for Nora claiming to know jack squat about all the shit Faz Ent tries to pull. Then again, a Ballora variant with the name Adelaide on the blueprint was a very obvious link. And just to top such a chaotic day off, how a doctor responded to him going into a panic attack because he thought he saw the Mangle out of the corners of his eyes outed one of the hospital's doctors as a fraud and former employee of an asylum that companies similar to and including Faz Ent used as witness disposal: so that was an eventful hospital stay.

Once Tristan had physically recovered, he returned to work. Acclimating to not putting pressure through various parts of his body, and adjusting to CD having to use written communication and starting to learn sign language because Adelaide's Arctic Ballora attack on CD had severed his vocal chords, so even if doctors could give him his voice back, he'd likely never sound the same again. Then, R&D robotics got a new hire, a new girl called Sadie who was adjusting to a loss of her own: someone close to her had been murdered. Tristan was the most surprised though when so soon after starting work and Nora getting her set up with the tools to survive the Special Delivery project, Sadie came in to work with news that her close companion was back from the dead and in a robotic form.

After Faz Ent finally got off of R&D Robotics back, Tristan finally had the time to process just how much he'd had to adjust: he still had to limit the weight of what he could carry, he couldn't bend as far so door frames were slightly more annoying (he's tall), but he had also grown closer to his fiancé Nora, and to those around him as well. He'd even made some new friends along the way too.

#2024#art#artwork#fnaf#fnaf au#renegade au#fnaf renegade au#fnaf fanart#five nights at freddys#fnaf ar#fnaf ar emails#fnaf ar special delivery#fnaf ar sd#fnaf ar tristan#fnaf tristan#tristan fnaf#tristan fnaf ar#fnaf special delivery

10 notes

·

View notes

Text

Discussing Partnerships in the High-Risk Merchant Processing Industry

Article by Jonathan Bomser | CEO | Accept-Credit-Cards-Now.com

youtube

In the current financial landscape, the high-risk merchant processing industry plays a crucial role in facilitating transactions for businesses considered riskier by traditional financial institutions. As businesses aim to expand their reach, partnerships become a key strategy in navigating the complexities of accepting credit cards.

Merchant Account Processing: Building Trust through Collaboration

In the realm of high-risk merchant account processing, establishing reliable partnerships is of utmost importance. Given the unique challenges associated with high-risk businesses, collaboration between payment processors and merchants can lead to innovative solutions that address specific industry needs. One primary advantage of strategic partnerships in merchant account processing is the ability to pool resources and expertise. Payment processors, with their knowledge of compliance requirements and risk management, can work closely with high-risk businesses to create tailored solutions. This approach not only ensures smoother merchant onboarding but also fosters a relationship built on trust and understanding.

Accept Credit Cards: Expanding Market Reach

For businesses operating in high-risk sectors, the ability to accept credit cards is a game-changer. Consumers increasingly prefer the convenience of card payments, and businesses unable to accommodate this preference may find themselves at a competitive disadvantage. Partnerships in the high-risk merchant processing industry can open doors for businesses to seamlessly integrate credit card acceptance. Payment processors, equipped with the latest technologies and security measures, can guide merchants through the integration process. This enhances the customer experience and broadens the market reach for high-risk businesses, enabling them to tap into a larger consumer base.

Payment Processing: Mitigating Risks through Collaboration

Effective risk management is at the core of successful high-risk merchant processing. In a landscape where fraudulent activities and chargebacks are prevalent, collaborative partnerships become instrumental in developing robust payment processing solutions. By leveraging the expertise of payment processors, high-risk merchants can implement advanced fraud detection tools and security measures. Shared insights and data analytics can further enhance risk assessment strategies, allowing businesses to stay one step ahead of potential threats. Through these collaborative efforts, the payment processing experience becomes not only secure but also efficient.

Enhancing Customer Support: A Focus on Service Excellence

Providing exceptional customer support is crucial for building long-term partnerships in payment processing. Collaborative efforts between payment processors and merchants can extend beyond transaction processing to include comprehensive customer support services. By working together, payment processors can offer dedicated support teams that specialize in high-risk industries. These teams are well-versed in the unique challenges faced by merchants in these sectors and can provide timely and knowledgeable assistance. Whether it's addressing payment issues, resolving disputes, or providing technical support, a strong focus on service excellence strengthens the relationship between payment processors and merchants, fostering trust and loyalty.

Staying Ahead of Regulatory Compliance: A Shared Responsibility

Compliance with regulatory standards is a top priority for businesses in the high-risk merchant processing industry. Collaborative partnerships play a vital role in staying ahead of evolving compliance requirements and ensuring adherence to industry regulations. Payment processors can actively monitor changes in regulations and communicate them to their merchant partners. By sharing insights and providing guidance on compliance best practices, payment processors help high-risk businesses navigate the complex landscape of regulatory requirements. This collaborative approach minimizes the risk of non-compliance, protects businesses from penalties or legal issues, and maintains a strong reputation within the industry.

By working together, payment processors and high-risk merchants can proactively address compliance challenges, establish robust internal controls, and demonstrate a commitment to operating ethically and responsibly.

#high risk merchant account#merchant processing#payment processing#high risk payment gateway#high risk payment processing#credit card processing#accept credit cards#credit card payment#payment#youtube#Youtube

21 notes

·

View notes

Text

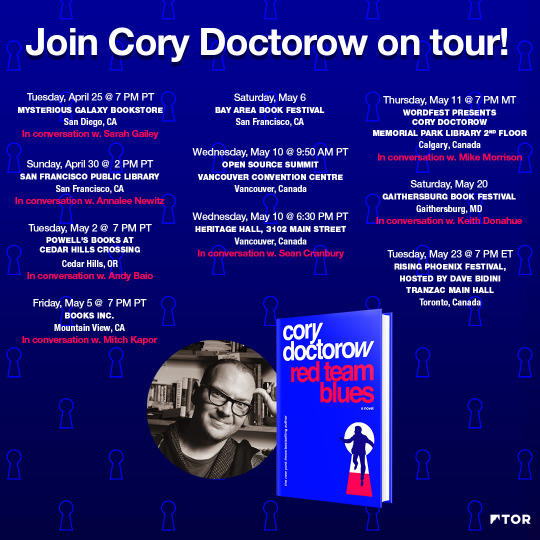

KPMG audits the nursing homes it advises on how to beat audits

Tomorrow (May 10), I’m in VANCOUVER for a keynote at the Open Source Summit and a book event for Red Team Blues at Heritage Hall and on Thurs (May 11), I’m in CALGARY for Wordfest.

Auditors are capitalism’s lubricants, who keep the gears of finance capital smoothly a-whirl, allowing investors to move their money in and out of companies without having to go pore over their books and walk through their facilities. Without auditors, the gears of capitalism would grind themselves to dust:

https://pluralistic.net/2021/02/18/ink-stained-wretches/#countless

If you’d like an essay-formatted version of this thread to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/05/09/dingo-babysitter/#maybe-the-dingos-ate-your-nan

Unfortunately for capitalism, auditing is irredeemably broken. The Big Four auditors (PWC, EY, Deloitte and KPMG) have merged to monopoly, becoming “too big to fail” and “too big to jail.” These four gigantic firms have spun up fantastically lucrative “consulting” divisions that advise companies on how to cheat on their audits and attain incredible (paper) gains. The work of these “consultants” is worth far more than the accounting and auditing jobs the companies do, and the weaker the audits are, the more profitable the consulting is:

https://pluralistic.net/2021/06/04/aaronsw/#crooked-ref

This crisis has been a long time brewing. Back in 2001, the accounting/consulting giant Arthur Andersen was at the center of Enron’s fraud, which lit $11B in shareholder capital on fire. Enron had been making everyday people angry for years, engineering rolling blackouts and incredible energy-price gouging, but no one cares about working peoples’ complaints. By contrast, stealing $11B from rich people was something the authorities couldn’t ignore. They gave Andersen the death penalty, trying to teach the surviving accounting firms a lesson about what happens when you fuck with plutes.

But those other firms learned the wrong lesson: the collapse of Andersen was so disruptive that it soon became clear that the authorities would never take another giant consulting firm down, no matter how egregious its conduct was. They doubled down on crime, and then doubled down again.

It’s hard to pick a winner in the Big Four Accounting Firm Corruption Olympics, but KPMG is a strong contender, with a long history of just being monumentally inept and wrong. Back when Enron was unspooling, KPMG devoted itself to threatening people who linked to its website “without a license to do so”:

https://web.archive.org/web/20020207141547/http://chris.raettig.org/email/jnl00040.html

A couple years later, they declared war on wifi, trying to convince normies that wireless networks were an existential risk to human civilization:

http://news.bbc.co.uk/2/hi/technology/2885339.stm

But there’s not much money in wifi scare stories or licenses to link. KPMG are good dialectical materialists, devoted to money over ideology, and boy did they figure out some wild ways to make money. For one thing, they figured out that they could get more accountants certified by cheating…on ethics exams:

https://www.marketwatch.com/story/the-kpmg-cheating-scandal-was-much-more-widespread-than-originally-thought-2019-06-18

KPMG’s top managers bribed regulators to give them the answer-sheets for ethics exams. What did they bribe those public employees with? Jobs at KPMG:

https://www.pogo.org/investigation/2020/01/how-accountants-took-washingtons-revolving-door-to-a-criminal-extreme

There’s hardly a month that goes by without another KPMG scandal somewhere in the world, with enormous monetary and social fallout. During the lockdowns, Justin Trudeau’s Liberal government outsourced the creation and maintenance of ArriveCAN (a contact tracing app for people who entered Canada) to a grifter called GC Strategies, who billed millions for their services. GC Strategies didn’t do any work — instead, they paid KPMG $1,000-$1,500 day to hire freelancers to build the app. The app itself was a catastrophic failure, and that failure didn’t just embarrass the government — it also failed to protect Canadians during a once-in-a-century global pandemic. KPMG raked off a 30% commission:

https://pluralistic.net/2023/01/31/mckinsey-and-canada/#comment-dit-beltway-bandits-en-canadien

In the USA, KPMG helped Microsoft work up a radioactively illegal tax-evasion scheme. Microsoft poured the millions it saved by cheating on its taxes into dark-money operations that lobbied to defund the IRS so that KPMG and Microsoft could cook up even more illegal tax-evasion schemes:

https://www.propublica.org/article/the-irs-decided-to-get-tough-against-microsoft-microsoft-got-tougher

But KPMG doesn’t content itself with screwing over everyday people and rotting our democratic institutions — it also engages in the dangerous business of helping billionaires steal from millionaires. KPMG was the auditor that signed off on the scam “oil company” Miller Energy Partners, a fraud that operated for years thanks to KPMG’s rubber-stamp on its crooked books:

https://www.desmog.com/2021/06/03/miller-energy-kpmg-auditors-oil-fraud/

The company was run by serial fraudsters with long rapsheets for stealing millions. They staffed their C-suite with executives from disgraced companies that had been busted for running Ponzi schemes, issuing press releases praising those execs’ “proven track records in raising capital.” KPMG ignored every red flag, ignored the hundreds of millions in fraud on the books — and when the whole thing came crashing down, the responsible KPMG partner kept his job for years, until retiring with a full and fat pension.

More recently, KPMG made millions by confidently certifying the stability of a large regional bank, assuring investors and depositors that it was managing its risk and could be trusted. The name of the client that KPMG was so bullish on will be familiar to you: Silicon Valley Bank:

https://www.wsj.com/articles/kpmg-faces-scrutiny-for-audits-of-svb-and-signature-bank-42dc49dd

KPMG epitomizes the idea of Too Big To Fail and Too Big to Jail. Despite being at the center of virtually every major finance scandal, it continues to thrive and grow. Remember the Carillion bust, in which billions went up in smoke and swathes of privatized government services vanished overnight? Not only did KPMG sign off on fraudulent Carillion books, but it escaped fines for doing so — and got paid to help administer Carillion’s bankruptcy:

https://www.reuters.com/business/finance/uk-watchdog-fines-kpmg-24-mln-over-carillion-regenersis-audits-2022-07-25/

Despite this, KPMG continues to find willing buyers for its services. After all, when the sector is dominated by four giant, lavishly corrupt firms, there’s not much choice in the matter:

https://pluralistic.net/2022/11/29/great-andersens-ghost/#mene-mene-bezzle

This is bad news for the investor class, of course, but it’s even worse news for the people who rely on the services that KPMG certifies, even as it helps grifters destroy them. Every kind of business relies on audits, from transit to aviation to day-care to eldercare.

Here’s a scary one for you: in Australia, the job of auditing residential eldercare homes’ compliance with safety and anti-abuse rules has been outsourced to KPMG. While KPMG earns a mid-sized fortune from these audits, it earns far more advising the owners of residential aged care homes on how to beat those audits:

https://www.theguardian.com/australia-news/2023/may/04/firm-performing-australian-aged-care-audit-also-charging-providers-for-expertise

KPMG says that the division that ensures the safety and dignity of elderly people is firewalled off from the division that advises companies on how to spend as little as possible on that safety and dignity — but KPMG also went to great lengths to keep the fact that it was selling services to both sides a secret.

Once the secret got out, an anonymous KPMG spokesmonster said, “When considering a request to perform an audit, we undertake a detailed process to ensure the engagement is free of conflicts.”

It’s hypothetically possible that this is true, but anyone who believes anything KPMG says is a sucker. The company’s rap-sheet goes back decades. This is, after all, a company that cheated on its ethics exams.

Catch me on tour with Red Team Blues in Vancouver, Calgary, Toronto, DC, Gaithersburg, Oxford, Hay, Manchester, Nottingham, London, and Berlin!

[Image ID: Two business-suited male figures seen side on; each has a bomb for a head, and each is holding a lit lighter that has ignited the other's fuse. Each bomb is wearing a green accountant's eyeshade. In the background is a fiery mushroom cloud. They wear KPMG logos on their lapels.]

Image:

Vectorportal.com (modified)

https://vectorportal.com/vector/business-deal-illustration/23215

CC BY 4.0

https://creativecommons.org/licenses/by/4.0/

Inspired by an illustration by Matt Kenyon for the Financial Times:

https://www.ft.com/content/07184d86-81cf-11e2-b050-00144feabdc0

#pluralistic#too big to jail#too big to fail#elder abuse#eldercare#conflict of interest#auspol#kpmg#nursing homes#dingo babysitters#australia#auditors

25 notes

·

View notes

Text

Understanding Blockchain Technology: Beyond Bitcoin

Introduction

Blockchain technology, often synonymous with Bitcoin, is a revolutionary system that has far-reaching implications beyond its initial use in cryptocurrency. While Bitcoin introduced the world to the concept of a decentralized ledger, blockchain's potential extends well beyond digital currencies. This article explores the fundamentals of blockchain technology and delves into its various applications across different industries.

What is Blockchain Technology?

At its core, blockchain is a decentralized, distributed ledger that records transactions across many computers in such a way that the registered transactions cannot be altered retroactively. This ensures transparency and security. Each block in the chain contains a list of transactions, and once a block is completed, it is added to the chain in a linear, chronological order.

Key features of blockchain include:

Transparency: All participants in the network can see the transactions recorded on the blockchain.

Immutability: Once data is recorded on the blockchain, it cannot be altered or deleted.

Security: Transactions are encrypted, and the decentralized nature of blockchain makes it highly secure against hacks and fraud.

Blockchain Beyond Bitcoin

While Bitcoin brought blockchain into the spotlight, other cryptocurrencies like Ethereum and Ripple have expanded its use cases. Ethereum, for example, introduced the concept of smart contracts—self-executing contracts where the terms are directly written into code. These smart contracts enable decentralized applications (DApps) that operate without the need for a central authority.

Applications of Blockchain Technology

Finance:

Decentralized Finance (DeFi): DeFi platforms leverage blockchain to create financial products and services that are open, permissionless, and transparent. These include lending, borrowing, and trading without intermediaries.

Cross-border Payments: Blockchain simplifies and speeds up cross-border transactions while reducing costs and increasing security.

Fraud Reduction: The transparency and immutability of blockchain make it harder for fraud to occur, as all transactions are visible and verifiable.

Supply Chain Management:

Tracking and Transparency: Blockchain provides end-to-end visibility of the supply chain, ensuring that all parties can track the movement and origin of goods.

Reducing Fraud: By recording every transaction, blockchain helps prevent fraud and counterfeiting, ensuring the authenticity of products.

Healthcare:

Secure Data Sharing: Blockchain allows for secure sharing of patient data between healthcare providers while maintaining privacy and consent.

Drug Traceability: Blockchain helps track pharmaceuticals through the supply chain, reducing the risk of counterfeit drugs.

Voting Systems:

Secure Elections: Blockchain can provide a transparent and tamper-proof system for voting, ensuring that each vote is recorded and counted accurately.

Increasing Voter Participation: The security and convenience of blockchain-based voting could lead to higher voter turnout and greater confidence in electoral systems.

Real Estate:

Property Transactions: Blockchain can streamline property transactions by reducing paperwork, ensuring transparency, and preventing fraud.

Record-Keeping: Immutable records of property ownership and transactions enhance security and trust in the real estate market.

Challenges and Limitations

Despite its potential, blockchain technology faces several challenges:

Scalability: The ability of blockchain networks to handle a large number of transactions per second is limited, impacting its adoption in high-volume industries.

Energy Consumption: Blockchain, particularly proof-of-work systems like Bitcoin, requires significant energy, raising concerns about its environmental impact.

Regulatory Challenges: The decentralized and borderless nature of blockchain poses regulatory and legal challenges, as governments and institutions seek to manage and control its use.

The Future of Blockchain Technology

The future of blockchain looks promising, with continuous advancements and innovations. Potential developments include improved scalability solutions like sharding and proof-of-stake consensus mechanisms, which aim to reduce energy consumption and increase transaction speeds. As blockchain technology matures, its adoption across various industries is expected to grow, potentially transforming the way we conduct business, manage data, and interact with digital systems.

Conclusion

Blockchain technology, initially popularized by Bitcoin, holds immense potential beyond cryptocurrencies. Its applications in finance, supply chain management, healthcare, voting, and real estate demonstrate its versatility and transformative power. While challenges remain, ongoing innovations and growing interest in blockchain suggest a future where this technology plays a crucial role in various aspects of our lives.

#blockchain#Bitcoin#blockchaintechnology#cryptocurrency#decentralizedfinance#DeFi#supplychain#healthcare#votingsystems#realestate#blockchainapplications#smartcontracts#DApps#digitalledger#blockchainsecurity#blockchainfuture#blockchainadoption#techinnovation#financial education#financial empowerment#financial experts#finance#digitalcurrency#unplugged financial#globaleconomy

2 notes

·

View notes

Text

Advantages of Electronic Insurance

Electronic insurance, also known as e-insurance, revolutionizes the insurance industry by leveraging digital technologies. In today's fast-paced world, where convenience and efficiency reign supreme, electronic insurance offers a myriad of benefits over traditional methods. Let's delve into the advantages of embracing electronic insurance in our lives.

Convenience

Embracing electronic insurance grants policyholders unparalleled convenience. With electronic insurance, individuals can conveniently access their policies anytime, anywhere, through online portals or mobile applications. Managing insurance portfolios becomes a breeze with just a few taps on a smartphone.

Cost-Effectiveness

One of the most appealing aspects of electronic insurance is its cost-effectiveness. By eliminating the need for physical infrastructure and streamlining administrative processes, insurers can offer lower premiums to policyholders. Additionally, electronic insurance reduces paperwork, saving both time and resources for insurers and policyholders alike.

Coverage

Electronic insurance offers comprehensive protection tailored to individual needs. Policyholders can choose from a wide range of flexible policies that suit their lifestyle and preferences. Whether it's health, life, auto, or property insurance, electronic platforms provide diverse coverage options to safeguard against unforeseen circumstances.

Quick Processing

In today's fast-paced world, time is of the essence. Electronic insurance ensures swift processing from policy issuance to claims settlement. With automated systems and digital workflows, policyholders can obtain insurance policies instantly and experience expedited claims processing, minimizing downtime during critical situations.

Customization Options

Electronic insurance empowers policyholders with customization options, allowing them to tailor policies according to their specific requirements. Additionally, individuals can opt for add-on benefits such as roadside assistance, travel insurance, or cyber protection for enhanced coverage.

Risk Management

Digitalization enhances risk management strategies for insurers and policyholders alike. By harnessing data-driven insights and analytics, insurers can assess risks more accurately and offer proactive solutions. Moreover, electronic platforms enable robust fraud detection mechanisms, safeguarding policyholders against potential threats.

Accessibility

Electronic insurance transcends geographical boundaries, offering accessibility to a broader demographic. Whether you're a frequent traveler or an expatriate, electronic platforms ensure global coverage, providing peace of mind wherever you go. Moreover, digital accessibility promotes financial inclusion by reaching underserved communities.

Security

Security is paramount in the realm of electronic insurance. Digital transactions are encrypted to ensure secure exchanges of sensitive information. Additionally, stringent privacy measures safeguard policyholders' personal data from unauthorized access, instilling confidence in the digital insurance ecosystem.

Environmental Impact

Electronic insurance champions eco-friendly initiatives by reducing paper consumption through paperless transactions. By embracing digital documentation and communication, insurers contribute to environmental conservation efforts while enhancing operational efficiency.

Customer Service

Exceptional customer service is a hallmark of electronic insurance. With round-the-clock support and online assistance, policyholders can address inquiries, file claims, or request assistance conveniently. Responsive customer service fosters trust and loyalty, ensuring a positive experience for policyholders.

Competitive Advantage

For insurers, embracing electronic insurance offers a competitive edge in a crowded marketplace. By differentiating themselves through digital innovation and enhanced customer experience, insurers can attract and retain customers effectively. Electronic insurance opens new avenues for growth and prosperity in the digital age.

Future Trends

The future of insurance lies in seamless integration with emerging technologies. Electronic insurance is poised to embrace advancements such as the Internet of Things (IoT) and artificial intelligence (AI) to offer personalized services and predictive analytics. As technology evolves, electronic insurance will continue to evolve, providing innovative solutions to meet evolving needs.

Conclusion

In conclusion, the Electronic Insurance are undeniable. From convenience and cost-effectiveness to enhanced security and environmental sustainability, electronic insurance offers a plethora of benefits for insurers and policyholders alike. Embracing electronic insurance paves the way for a digitally empowered future, where insurance becomes synonymous with efficiency, innovation, and peace of mind.

3 notes

·

View notes

Text

Smart contracts: Transformative applications of blockchain technology

Smart contracts are a key application of blockchain technology that utilizes programming code to automatically execute, control, and record contract terms without relying on traditional intermediaries. This technology is gradually transforming our understanding of contracts and transactions, bringing unprecedented efficiency and transparency to a wide range of industries. This article will delve into the benefits, application scenarios, and challenges of smart contracts.

Advantages of smart contracts

Automation: Once a smart contract is written and deployed on the blockchain, it can be automatically executed when preset conditions are met. This automation not only increases efficiency, but also reduces human error and latency.

Lower costs: Execution of smart contracts does not rely on third-party intermediaries such as lawyers, banks and other financial institutions, thus significantly reducing the cost of transaction and contract execution. This disintermediation not only reduces costs, but also simplifies the process.

Increase transparency: the terms of all smart contracts are open and transparent, and all interested parties can view the status and activity of the contract in real time. This transparency builds trust and reduces information asymmetries and misunderstandings.

Security and immutability: Blockchain technology ensures that once a contract is deployed, its contents and records cannot be modified, improving the security of contract execution. All transactions are transparent and cannot be changed once recorded, reducing the risk of fraud and malicious behavior.

Reduce the risk of fraud: Due to the transparency and immutability of contracts, smart contracts greatly reduce the possibility of fraud. All parties can view the transaction history and contract execution, ensuring that everything is fair and transparent.

Improve efficiency and speed: The automatic execution features of smart contracts greatly improve the efficiency of processing transactions and contracts. While traditional contracts can take days, weeks or even months to execute, smart contracts can be completed in minutes, dramatically increasing the speed of business operations.

Facilitate new business models and services: Smart contracts make it possible to create complex business models and automated services that are difficult to achieve in traditional contract frameworks. They open the way for the development of innovative financial instruments, decentralized applications (DApps) and automated systems.

Application scenarios of smart contracts

Smart contracts can be used in a wide range of scenarios, including but not limited to:

Financial services, such as creating decentralized finance (DeFi) applications that automatically execute contracts for lending, insurance, payments, and more.

Supply chain management, monitoring the flow of goods and automatically releasing payments when goods meet a certain condition or location.

Digital identity, manage and verify digital identification, and simplify the online authentication process.

Voting system, creating a transparent and immutable voting system to ensure the fairness of the voting process.

Copyright and Intellectual Property, automatically manage and enforce copyright payments and distribution to protect the interests of creators.

The challenges and limitations of smart contracts

While smart contracts offer many advantages, they also face some challenges and limitations, including:

Code security: The security of smart contracts depends on how their code is written, and the presence of vulnerabilities can lead to serious security issues.

Legal status and compliance: The legal status of smart contracts is unclear and there may be legal and regulatory uncertainties in different jurisdictions.

Dependence on external data: Many smart contracts need to rely on external data sources to trigger execution conditions, and if external data is inaccurate, it can affect the outcome of contract execution.

Technical barriers and complexity of use: Writing and deploying smart contracts requires specialized programming skills and can be a high technical barrier for the average user.

peroration

Smart contracts, a key application of blockchain technology, are opening up new areas of automated trading and application development. They have the advantages of increased transaction efficiency, reduced costs, increased transparency and security, but they also face some challenges, especially in terms of code security, legal status and dependence on external data. As technology advances and regulations improve, smart contracts are expected to continue to play an important role in various industries, driving the development of the digital economy.

#BitNest#BitNestLoop#BitNestPureContract#BitNestis the best project in the currency circle#BitNestSecurely#BitNestAutonomously#BitNestDecentralizedly#BitNestCryptographically

3 notes

·

View notes

Text

Smart contracts: Transformative applications of blockchain technology

Smart contracts are a key application of blockchain technology that utilizes programming code to automatically execute, control, and record contract terms without relying on traditional intermediaries. This technology is gradually transforming our understanding of contracts and transactions, bringing unprecedented efficiency and transparency to a wide range of industries. This article will delve into the benefits, application scenarios, and challenges of smart contracts.

Advantages of smart contracts

Automation: Once a smart contract is written and deployed on the blockchain, it can be automatically executed when preset conditions are met. This automation not only increases efficiency, but also reduces human error and latency.

Lower costs: Execution of smart contracts does not rely on third-party intermediaries such as lawyers, banks and other financial institutions, thus significantly reducing the cost of transaction and contract execution. This disintermediation not only reduces costs, but also simplifies the process.

Increase transparency: the terms of all smart contracts are open and transparent, and all interested parties can view the status and activity of the contract in real time. This transparency builds trust and reduces information asymmetries and misunderstandings.

Security and immutability: Blockchain technology ensures that once a contract is deployed, its contents and records cannot be modified, improving the security of contract execution. All transactions are transparent and cannot be changed once recorded, reducing the risk of fraud and malicious behavior.

Reduce the risk of fraud: Due to the transparency and immutability of contracts, smart contracts greatly reduce the possibility of fraud. All parties can view the transaction history and contract execution, ensuring that everything is fair and transparent.

Improve efficiency and speed: The automatic execution features of smart contracts greatly improve the efficiency of processing transactions and contracts. While traditional contracts can take days, weeks or even months to execute, smart contracts can be completed in minutes, dramatically increasing the speed of business operations.

Facilitate new business models and services: Smart contracts make it possible to create complex business models and automated services that are difficult to achieve in traditional contract frameworks. They open the way for the development of innovative financial instruments, decentralized applications (DApps) and automated systems.

Application scenarios of smart contracts

Smart contracts can be used in a wide range of scenarios, including but not limited to:

Financial services, such as creating decentralized finance (DeFi) applications that automatically execute contracts for lending, insurance, payments, and more.

Supply chain management, monitoring the flow of goods and automatically releasing payments when goods meet a certain condition or location.

Digital identity, manage and verify digital identification, and simplify the online authentication process.

Voting system, creating a transparent and immutable voting system to ensure the fairness of the voting process.

Copyright and Intellectual Property, automatically manage and enforce copyright payments and distribution to protect the interests of creators.

The challenges and limitations of smart contracts

While smart contracts offer many advantages, they also face some challenges and limitations, including:

Code security: The security of smart contracts depends on how their code is written, and the presence of vulnerabilities can lead to serious security issues.

Legal status and compliance: The legal status of smart contracts is unclear and there may be legal and regulatory uncertainties in different jurisdictions.

Dependence on external data: Many smart contracts need to rely on external data sources to trigger execution conditions, and if external data is inaccurate, it can affect the outcome of contract execution.

Technical barriers and complexity of use: Writing and deploying smart contracts requires specialized programming skills and can be a high technical barrier for the average user.

peroration

Smart contracts, a key application of blockchain technology, are opening up new areas of automated trading and application development. They have the advantages of increased transaction efficiency, reduced costs, increased transparency and security, but they also face some challenges, especially in terms of code security, legal status and dependence on external data. As technology advances and regulations improve, smart contracts are expected to continue to play an important role in various industries, driving the development of the digital economy.

#BitNest#BitNestLoop#BitNestPureContract#BitNestis the best project in the currency circle#BitNestSecurely#BitNestAutonomously#BitNestDecentralizedly#BitNestCryptographically

3 notes

·

View notes

Text

Smart contracts: Transformative applications of blockchain technology

Smart contracts are a key application of blockchain technology that utilizes programming code to automatically execute, control, and record contract terms without relying on traditional intermediaries. This technology is gradually transforming our understanding of contracts and transactions, bringing unprecedented efficiency and transparency to a wide range of industries. This article will delve into the benefits, application scenarios, and challenges of smart contracts.

Advantages of smart contracts

Automation: Once a smart contract is written and deployed on the blockchain, it can be automatically executed when preset conditions are met. This automation not only increases efficiency, but also reduces human error and latency.

Lower costs: Execution of smart contracts does not rely on third-party intermediaries such as lawyers, banks and other financial institutions, thus significantly reducing the cost of transaction and contract execution. This disintermediation not only reduces costs, but also simplifies the process.

Increase transparency: the terms of all smart contracts are open and transparent, and all interested parties can view the status and activity of the contract in real time. This transparency builds trust and reduces information asymmetries and misunderstandings.

Security and immutability: Blockchain technology ensures that once a contract is deployed, its contents and records cannot be modified, improving the security of contract execution. All transactions are transparent and cannot be changed once recorded, reducing the risk of fraud and malicious behavior.

Reduce the risk of fraud: Due to the transparency and immutability of contracts, smart contracts greatly reduce the possibility of fraud. All parties can view the transaction history and contract execution, ensuring that everything is fair and transparent.

Improve efficiency and speed: The automatic execution features of smart contracts greatly improve the efficiency of processing transactions and contracts. While traditional contracts can take days, weeks or even months to execute, smart contracts can be completed in minutes, dramatically increasing the speed of business operations.

Facilitate new business models and services: Smart contracts make it possible to create complex business models and automated services that are difficult to achieve in traditional contract frameworks. They open the way for the development of innovative financial instruments, decentralized applications (DApps) and automated systems.

Application scenarios of smart contracts

Smart contracts can be used in a wide range of scenarios, including but not limited to:

Financial services, such as creating decentralized finance (DeFi) applications that automatically execute contracts for lending, insurance, payments, and more.

Supply chain management, monitoring the flow of goods and automatically releasing payments when goods meet a certain condition or location.

Digital identity, manage and verify digital identification, and simplify the online authentication process.

Voting system, creating a transparent and immutable voting system to ensure the fairness of the voting process.

Copyright and Intellectual Property, automatically manage and enforce copyright payments and distribution to protect the interests of creators.

The challenges and limitations of smart contracts

While smart contracts offer many advantages, they also face some challenges and limitations, including:

Code security: The security of smart contracts depends on how their code is written, and the presence of vulnerabilities can lead to serious security issues.

Legal status and compliance: The legal status of smart contracts is unclear and there may be legal and regulatory uncertainties in different jurisdictions.

Dependence on external data: Many smart contracts need to rely on external data sources to trigger execution conditions, and if external data is inaccurate, it can affect the outcome of contract execution.

Technical barriers and complexity of use: Writing and deploying smart contracts requires specialized programming skills and can be a high technical barrier for the average user.

peroration

Smart contracts, a key application of blockchain technology, are opening up new areas of automated trading and application development. They have the advantages of increased transaction efficiency, reduced costs, increased transparency and security, but they also face some challenges, especially in terms of code security, legal status and dependence on external data. As technology advances and regulations improve, smart contracts are expected to continue to play an important role in various industries, driving the development of the digital economy.

#BitNest#BitNestLoop#BitNestPureContract#BitNestis the best project in the currency circle#BitNestSecurely#BitNestAutonomously#BitNestDecentralizedly#BitNestCryptographically

4 notes

·

View notes

Text

TikTok recently announced that its users in the European Union will soon be able to switch off its infamously engaging content-selection algorithm. The EU’s Digital Services Act (DSA) is driving this change as part of the region’s broader effort to regulate AI and digital services in accordance with human rights and values.

TikTok’s algorithm learns from users’ interactions—how long they watch, what they like, when they share a video—to create a highly tailored and immersive experience that can shape their mental states, preferences, and behaviors without their full awareness or consent. An opt-out feature is a great step toward protecting cognitive liberty, the fundamental right to self-determination over our brains and mental experiences. Rather than being confined to algorithmically curated For You pages and live feeds, users will be able to see trending videos in their region and language, or a “Following and Friends” feed that lists the creators they follow in chronological order. This prioritizes popular content in their region rather than content selected for its stickiness. The law also bans targeted advertisement to users between 13 and 17 years old, and provides more information and reporting options to flag illegal or harmful content.

In a world increasingly shaped by artificial intelligence, Big Data, and digital media, the urgent need to protect cognitive liberty is gaining attention. The proposed EU AI Act offers some safeguards against mental manipulation. UNESCO’s approach to AI centers human rights, the Biden Administration’s voluntary commitments from AI companies addresses deception and fraud, and the Organization for Economic Cooperation and Development has incorporated cognitive liberty into its principles for responsible governance of emerging technologies. But while laws and proposals like these are making strides, they often focus on subsets of the problem, such as privacy by design or data minimization, rather than mapping an explicit, comprehensive approach to protecting our ability to think freely. Without robust legal frameworks in place worldwide, the developers and providers of these technologies may escape accountability. This is why mere incremental changes won't suffice. Lawmakers and companies urgently need to reform the business models on which the tech ecosystem is predicated.

A well-structured plan requires a combination of regulations, incentives, and commercial redesigns focusing on cognitive liberty. Regulatory standards must govern user engagement models, information sharing, and data privacy. Strong legal safeguards must be in place against interfering with mental privacy and manipulation. Companies must be transparent about how the algorithms they’re deploying work, and have a duty to assess, disclose, and adopt safeguards against undue influence.

Much like corporate social responsibility guidelines, companies should also be legally required to assess their technology for its impact on cognitive liberty, providing transparency on algorithms, data use, content moderation practices, and cognitive shaping. Efforts at impact assessments are already integral to legislative proposals worldwide, including the EU’s Digital Services Act, the US's proposed Algorithmic Accountability Act and American Data Privacy and Protection Act, and voluntary mechanisms like the US National Institute of Standards and Technology’s 2023 Risk Management Framework. An impact assessment tool for cognitive liberty would specifically measure AI’s influence on self-determination, mental privacy, and freedom of thought and decisionmaking, focusing on transparency, data practices, and mental manipulation. The necessary data would encompass detailed descriptions of the algorithms, data sources and collection, and evidence of the technology's effects on user cognition.

Tax incentives and funding could also fuel innovation in business practices and products to bolster cognitive liberty. Leading AI ethics researchers emphasize that an organizational culture prioritizing safety is essential to counter the many risks posed by large language models. Governments can encourage this by offering tax breaks and funding opportunities, such as those included in the proposed Platform Accountability and Transparency Act, to companies that actively collaborate with educational institutions in order to create AI safety programs that foster self-determination and critical thinking skills. Tax incentives could also support research and innovation for tools and techniques that surface deception by AI models.

Technology companies should also adopt design principles embodying cognitive liberty. Options like adjustable settings on TikTok or greater control over notifications on Apple devices are steps in the right direction. Other features that enable self-determination—including labeling content with “badges” that specify content as human- or machine-generated, or asking users to engage critically with an article before resharing it—should become the norm across digital platforms.

The TikTok policy change in Europe is a win, but it’s not the endgame. We urgently need to update our digital rulebook, implementing new laws, regulations, and incentives that safeguard user’s rights and hold platforms accountable. Let’s not leave the control over our minds to technology companies alone; it’s time for global action to prioritize cognitive liberty in the digital age.

9 notes

·

View notes

Last Seen Blogs