#term insurance for 20 years

Text

How Does a 20 Year Term Insurance Plan Work?

A term insurance for 20 years works straightforwardly. Those who enroll in this scheme are granted protection throughout its term, which spans 20 years. If the policyholder passes away during the duration of a 20 year term insurance, their designated beneficiary would receive a death benefit. The policy remains in force as long as premiums are regularly paid. However, if the policyholder dies after the policy matures, no benefits would be disbursed. Also, if the policyholder survives the entire policy term, there would be no maturity benefits provided to them or their beneficiaries.

How to Calculate 20 Year Term Life Insurance Premiums?

Using a term insurance premium calculator enables you to determine the necessary insurance coverage to financially secure your family members, along with calculating the corresponding premium. Following a general guideline, the coverage amount should adequately meet your family’s financial requirements in unforeseen circumstances. Meanwhile, the premium for your selected term plan must fit comfortably within your monthly budget.

You can follow these steps to calculate your term insurance premium with an online calculator:

Step 1: Provide Your Details

Begin by inputting personal information such as your date of birth, gender, marital status, annual income, number of dependents, desired life cover, and any smoking habits into the term insurance calculator. It’s crucial to note that your annual income reflects your earning capacity, thus influencing the premium rates of the term insurance policy.

Step 2: Specify The Desired Sum Assured

Next, indicate the sum assured amount you require and the duration of coverage. Additionally, clarify whether you prefer your family to receive a lump sum payout or monthly income. Simply submit these details and await the results.

Step 3: Compare Available Plans

Upon completion, the online term insurance premium calculator will suggest suitable term insurance plans based on the provided information. Conduct a thorough comparison of the options presented, select the most suitable plan, and proceed with the purchase.

0 notes

Note

It makes me sad that Keith only performed one song yesterday. I believe it’s the first time he’s done this in over 40 years! I really do hope that this was just a one-off for opening night and not indicative of any serious issues within the band or with himself.

I’ve watched quite a bit of the footage from yesterday and I just don’t think Keith was up to doing two solo songs by himself. He messed up the opening riff to the first song, “Start Me Up”, and through the whole concert he wasn’t playing a lot of the time/was frequently pausing and sort of wiping his eyes or staring off into the middle distance. It may be that he’s exhausted from rehearsals and needs some time to recoup before he takes on his normal load, but I kind of doubt it.

Honestly, they sound worse than when I saw them in 2021. For all the ‘new energy’ talk, Keith has never kept up well with Steve in the Stones (he plays too forcefully and too fast, for a start) and the more severe his arthritis becomes the worse that dynamic gets. I was kind of shocked at the amount of negative comments on the videos I watched. There were the typical Boomers jumping in to defend this, but most of what they could scrape together was “how dare you judge 80 year olds like this!” and the like, which didn’t seem to be convincing anyone.

#I hold firm on the opinion that they made a mistake continuing after No Filter#but at this point I’m mostly just kind of disappointed and saddened by it#I don’t think Keith of 10 never mind 20 years ago would have been admiring of this#in personal or musical terms#but mick likes making money and keith feels like he needs it to keep going and ronnie will follow whatever they say#so I suppose it’s just bound to keep going until they can no longer get insurance anymore#or somebody can no longer play#(if that somebody is mick or keith. since they’ve established the grotesque precedent that everyone else can be replaced)#the rolling stones#keith richards#old married band#ask response#anonymous

9 notes

·

View notes

Text

My adult advice is if you do pursue something you're passionate in for a career (or really if you go about getting any job) that being treated like shit is not fair to you. Working over 40 hours for your dream job a week, working 60 hour crunch hours for months for your dream job, working with no health insurance for years, your dream job paying you a wage too low to live where you need to in order to do the job so you're financially getting worse, your job not hiring enough people because you care about the work too much to let it fail so they just overwork you and have you do 2-3 peoples jobs, your dream job does not protect you from work hazards and you feel you'll lose your job if you bring it up? You don't deserve any of that shit. You deserve better. Whether your job is some boring thing you don't care about, or your absolute favorite thing in the world that you care about deeply and find to be the meaning of your life, you deserve to be treated fairly. You deserve to not be overworked to the point of suicidal or sick, you deserve to be able to go to the doctor and take your kids to the doctor and know if your kid gets a long term illness you can get long term treatment, you deserve to not have the entire success of a company fall on your shoulders to do multiple jobs if you weren't the supervisor who decided Not to adequately hire, you deserve to be able to go pee when you need to, you deserve to have adequate protection from dangers to your life. Period. No matter what job. If you're being treated like shit, you don't deserve it. It's not a price you should be expected to endure, not even for your dream job. It's a fucked up situation that real people caused by deciding to treat their employees badly.

#rant#feel free to ignore#but like. if you never had a job yet or havent had many jobs yet or ur in college#its some food for thought.#i just like. when i was a child i didnt understand some choices my dad made.#now that im an adult? i do have a job i like and find meaningful.#but also like... i did WANT to do character concept art for video games. but i see employees in those companies now#workjng 60 hour crunch hours. short term contract work so no health insurance.#and its like... well i needed 4 surgeries in the last 4 years. i needed the ER like 20 times.#i needed 2 of those surgeries as a direct result of when i worked 60 hour weeks for a year#and it made me both mentally suicidal despite Liking the work. and physically damaged my health for life#and now i need medicine montjly that costs 600 or more if i didnt have insurance.#so its like... well. if i had tried to do character concept art for X companies games i played?#well id be dead right now. dead before age 28. because 60 hour workweeks over a year probably wouldve killed me#my life wouldnt have been worth drawing if yhat job turned my passion into my own hell and my own killet#you get me?#like. even if you pursue a dream job (or a hated job even)#know your limits. your life is most important. if a job says 60 hours ans you got 2 kids and need to work#until you can get another job to hire you? then you take the risk probably yeah#or youre healthy and willing to suffer for 4 months before ysing the experience to apply for a job that is 40 hours a#week and pays more. but if a job is demanding inhumane bullshit it IS a horrible thing#and its something you deserve better than.

1 note

·

View note

Link

Your project deserves excellence. Trust our dedication to delivering quality and satisfaction. Faulkner Surety & Insurance LLC provides a wide range of insurance services to meet your needs. Whether you're looking for term life insurance, fixed or variable annuities, or affordable Business insurance in St. Petersburg FL, we're here to help. We specialize in both personal and commercial insurance, offering everything from general liability insurance to commercial and business surety bonds. With reliable life insurance services in St. Petersburg, FL and trusted surety bond services near you, we are committed to protecting what matters most. For outstanding insurance services in your area, call Faulkner Surety & Insurance LLC today and let us guide you through your insurance needs.

0 notes

Text

autism awareness & autism acceptance not either or. not mutually exclusive. can coexist. need coexist.

“there enough awareness for autism already 🙄 we need acceptance”

ok. you aware of high support needs autism? aware what that even means? not “need reminder take meds need remind take shower” “high” support needs autism, but “need full physical help do bADLs lack danger awareness may accidentally hurt self or even kill self without support” high support needs autism? not just higher support needs people who can be independently online do advocacy, but those who need help from others even be online, or those who cannot be online at. all.?

aware of nonverbal nonspeaking people? not just nonverbal nonspeaking people who can write grammatically correct cannot tell apart base on writing. not just nonverbal nonspeaking people who can be online who can advocate online.

aware of nonverbal nonspeaking people who cannot communicate in way that easily understood, either for now, or ever? aware of nonverbal nonspeaking people without functional communication, aware of how without functional communication, how that drastically limit communication, even though behaviors are valid communication? aware of nonverbal nonspeaking people who may never use AAC fluently even with best support?

aware of technically verbal but very limited verbal autistics who may only able say wants & needs but not other things and certainly not online advocacy, “despite being verbal”?

aware of just how much our life depends on caregiver/carer/PCA/etc? aware how vulnerable that make us? aware of abuse from caregivers? aware of caregiver burnout from lack of support for caregivers, & how that impact our care we receive? have you even heard of term respite care? aware of those of us who cannot separate ourselves from caregiver? aware of those of us who cannot participate in autism community without caregiver?

aware of visibly autistic people? aware how we not automatically believed? aware how we often bear blunt of violence because we most easily identified target because we visible? aware visible =/= get support, aware that many those diagnosed severe who now adult so no longer qualify for services under 21 year old, languish in hospitals because nowhere to go? aware how long life saving necessary waitlists are? aware that even to this day parents have to fight school fight day service fight government fight insurance for them give their nonverbal nonspeaking child AAC & be properly taught how use it? actually, are you aware of how properly teach AAC to nonverbal nonspeaking, developmentally delayed child who may or may not have intellectual disability?

actually, aware of autistics with (correctly diagnosed) intellectual disability & how they make up big amount of autistic? aware of institutional systemic & legal impact of mental [r word] right & the human rights abuse justified using r word right? wait, you aware that r word come from old term for intellectual disability, that, actually, still in many laws because no one bothered updating, right? aware of what severe profound ID look like? and aware they real and they still human deserve education deserve life deserve care, yes?

aware of early diagnosis 20 30 or even 10 years ago, not same as now, even less resources & knowledge about autism now? aware that while gender race class 1000% impacted diagnoses, a lot of early diagnosed people early diagnosed because… they die without support unlocked by diagnosis, right? but also, aware that in old times, early diagnosis often did mean doom, not because autism bad or anything, but because severe lack of support & diagnosis can literally bar you from so many things including basic education?

aware that for many people in special education, which impact specific group of autistic people, they not get degree when graduate high school, they just get certificate, which limit their educational & employment opportunities & others?

aware of life saving importance and necessity of masking for autistic of color especially Black autistic people, despite stress inducing traumatic? aware that live in broken system be victim of hate crime & police brutality just as traumatic often even more traumatic than masking? aware that many Black & other parents of color forced to teach their child masking because of this?

are you aware of most marginalized autistic people? aware of leadership of most impacted?

aware you can and need to care about autistic experiences & form of autism you not experience? aware that you can and need to do that without try twist your experience into our experience into our words our community?

aware that advocacy goes beyond about you?

aware that you can’t speak for all autistic? aware that you shouldn’t speak for all autistic?

are you aware of when you need to stop talking & listen & amplify others? aware of when and how to decenter self?

aware that even this long post, barely scratch surface? still so much to say?

[better worded version of original post]

#loaf screm#actually autistic#autism acceptence month#autism awareness#autism awareness month#high support needs#long post#nonverbal#nonspeaking#autism#autistic#autism acceptance

1K notes

·

View notes

Text

If I could give one piece of life advice to my fellow humans, it would be this highly specific little chestnut: "If you ever sprain your ankle, get medical care."

One of the most common things I've heard from older people than myself is, "Oh yeah, I twisted my ankle in (insert grade of school here) and it's never been the same." Or, "I have a bad ankle. I can't tell you how many times I've sprained it." And one of the most common things I've heard from younger people is some variation on, "Yeah, I think I just twisted my ankle. I think I have some old crutches from high school at my parents' house. I'll just use those for a few days."

I didn't learn this until after I sprained my ankle last year, but 20% of ankle sprains lead to chronic ankle instability, which was grimly defined by my doctor as, "an unending cycle of ankle sprains."

Another thing I didn't fully understand is that "sprain" is an umbrella term for any of those ligament injuries. Yeah, you could simply stretch the ligament-- twist it. Or you could tear it. Or you could completely sever it, and those are all sprains. If you're not a doctor, it's likely hard to tell what degree of sprain you have. The worse the sprain, the higher the chance of it healing weird and becoming unstable. If you are having trouble putting weight on your ankle and it's not feeling better the next day, please get it checked out!

I know medical care is expensive and many of us don't have health insurance, but it might cost you more in the long run if you don't get care for a hurt ankle. Otherwise you might spend a lifetime of having to get MORE ankle injuries checked out, missing work or social opportunities due to ankle injury, having to limit exercise, surgeries later in life, and more.

When I hurt my ankle and foot last year, I assumed the broken foot bone would be the bigger concern, but my treatment plan was almost entirely centered around the ankle ligament tear. My doctor said that was the more serious injury and the more finicky bit to heal. I worry when I hear a friend mention they sprained their ankle and were just treating it at home, 'trying to stay off it as much as I can.' That usually means a few days, but I had to stay completely off mine for 4 weeks, followed by a walking boot, a brace, and months of physical therapy. It was intense!

Ankles are annoying because they support your entire darn body and you don't realize how much you need them until you hurt one. So that is the one nugget of wisdom I hope to leave all of you with!

14K notes

·

View notes

Text

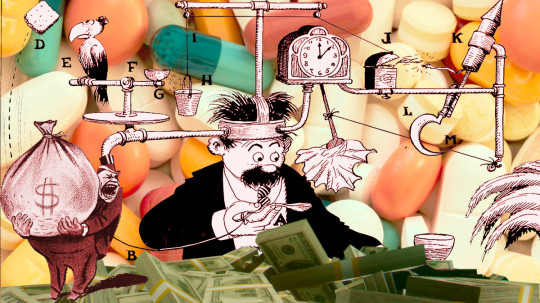

What the fuck is a PBM?

TOMORROW (Sept 24), I'll be speaking IN PERSON at the BOSTON PUBLIC LIBRARY!

Terminal-stage capitalism owes its long senescence to its many defensive mechanisms, and it's only by defeating these that we can put it out of its misery. "The Shield of Boringness" is one of the necrocapitalist's most effective defenses, so it behooves us to attack it head-on.

The Shield of Boringness is Dana Claire's extremely useful term for anything so dull that you simply can't hold any conception of it in your mind for any length of time. In the finance sector, they call this "MEGO," which stands for "My Eyes Glaze Over," a term of art for financial arrangements made so performatively complex that only the most exquisitely melted brain-geniuses can hope to unravel their spaghetti logic. The rest of us are meant to simply heft those thick, dense prospectuses in two hands, shrug, and assume, "a pile of shit this big must have a pony under it."

MEGO and its Shield of Boringness are key to all of terminal-stage capitalism's stupidest scams. Cloaking obvious swindles in a lot of complex language and Byzantine payment schemes can make them seem respectable just long enough for the scammers to relieve you of all your inconvenient cash and assets, though, eventually, you're bound to notice that something is missing.

If you spent the years leading up to the Great Financial Crisis baffled by "CDOs," "synthetic CDOs," "ARMs" and other swindler nonsense, you experienced the Shield of Boringness. If you bet your house and/or your retirement savings on these things, you experienced MEGO. If, after the bubble popped, you finally came to understand that these "exotic financial instruments" were just scams, you experienced Stein's Law ("anything that can't go forever eventually stops"). If today you no longer remember what a CDO is, you are once again experiencing the Shield of Boringness.

As bad as 2008 was, it wasn't even close to the end of terminal stage capitalism. The market has soldiered on, with complex swindles like carbon offset trading, metaverse, cryptocurrency, financialized solar installation, and (of course) AI. In addition to these new swindles, we're still playing the hits, finding new ways to make the worst scams of the 2000s even worse.

That brings me to the American health industry, and the absurdly complex, ridiculously corrupt Pharmacy Benefit Managers (PBMs), a pathology that has only metastasized since 2008.

On at least 20 separate occasions, I have taken it upon myself to figure out how the PBM swindle works, and nevertheless, every time they come up, I have to go back and figure it out again, because PBMs have the most powerful Shield of Boringness out of the whole Monster Manual of terminal-stage capitalism's trash mobs.

PBMs are back in the news because the FTC is now suing the largest of these for their role in ripping off diabetics with sky-high insulin prices. This has kicked off a fresh round of "what the fuck is a PBM, anyway?" explainers of extremely variable quality. Unsurprisingly, the best of these comes from Matt Stoller:

https://www.thebignewsletter.com/p/monopoly-round-up-lina-khan-pharma

Stoller starts by pointing out that Americans have a proud tradition of getting phucked by pharma companies. As far back as the 1950s, Tennessee Senator Estes Kefauver was holding hearings on the scams that pharma companies were using to ensure that Americans paid more for their pills than virtually anyone else in the world.

But since the 2010s, Americans have found themselves paying eye-popping, sky-high, ridiculous drug prices. Eli Lilly's Humolog insulin sold for $21 in 1999; by 2017, the price was $274 – a 1,200% increase! This isn't your grampa's price gouging!

Where do these absurd prices come from? The story starts in the 2000s, when the GW Bush administration encouraged health insurers to create "high deductible" plans, where patients were expected to pay out of pocket for receiving care, until they hit a multi-thousand-dollar threshold, and then their insurance would kick in. Along with "co-pays" and other junk fees, these deductibles were called "cost sharing," and they were sold as a way to prevent the "abuse" of the health care system.

The economists who crafted terminal-stage capitalism's intellectual rationalizations claimed the reason Americans paid so much more for health care than their socialized-medicine using cousins in the rest of the world had nothing to do with the fact that America treats health as a source of profits, while the rest of the world treats health as a human right.

No, the actual root of America's health industry's problems was the moral defects of Americans. Because insured Americans could just go see the doctor whenever they felt like it, they had no incentive to minimize their use of the system. Any time one of these unhinged hypochondriacs got a little sniffle, they could treat themselves to a doctor's visit, enjoying those waiting-room magazines and the pleasure of arranging a sick day with HR, without bearing any of the true costs:

https://pluralistic.net/2021/06/27/the-doctrine-of-moral-hazard/

"Cost sharing" was supposed to create "skin in the game" for every insured American, creating a little pain-point that stung you every time you thought about treating yourself to a luxurious doctor's visit. Now, these payments bit hardest on the poorest workers, because if you're making minimum wage, at $10 co-pay hurts a lot more than it does if you're making six figures. What's more, VPs and the C-suite were offered "gold-plated" plans with low/no deductibles or co-pays, because executives understand the value of a dollar in the way that mere working slobs can't ever hope to comprehend. They can be trusted to only use the doctor when it's truly warranted.

So now you have these high-deductible plans creeping into every workplace. Then along comes Obama and the Affordable Care Act, a compromise that maintains health care as a for-profit enterprise (still not a human right!) but seeks to create universal coverage by requiring every American to buy a plan, requiring insurers to offer plans to every American, and uses public money to subsidize the for-profit health industry to glue it together.

Predictably, the cheapest insurance offered on the Obamacare exchanges – and ultimately, by employers – had sky-high deductibles and co-pays. That way, insurers could pocket a fat public subsidy, offer an "insurance" plan that was cheap enough for even the most marginally employed people to afford, but still offer no coverage until their customers had spent thousands of dollars out-of-pocket in a given year.

That's the background: GWB created high-deductible plans, Obama supercharged them. Keep that in your mind as we go through the MEGO procedures of the PBM sector.

Your insurer has a list of drugs they'll cover, called the "formulary." The formulary also specifies how much the insurance company is willing to pay your pharmacist for these drugs. Creating the formulary and paying pharmacies for dispensing drugs is a lot of tedious work, and insurance outsources this to third parties, called – wait for it – Pharmacy Benefits Managers.

The prices in the formulary the PBM prepares for your insurance company are called the "list prices." These are meant to represent the "sticker price" of the drug, what a pharmacist would charge you if you wandered in off the street with no insurance, but somehow in possession of a valid prescription.

But, as Stoller writes, these "list prices" aren't actually ever charged to anyone. The list price is like the "full price" on the pricetags at a discount furniture place where everything is always "on sale" at 50% off – and whose semi-disposable sofas and balsa-wood dining room chairs are never actually sold at full price.

One theoretical advantage of a PBM is that it can get lower prices because it bargains for all the people in a given insurer's plan. If you're the pharma giant Sanofi and you want your Lantus insulin to be available to any of the people who must use OptumRX's formulary, you have to convince OptumRX to include you in that formulary.

OptumRX – like all PBMs – demands "rebates" from pharma companies if they want to be included in the formulary. On its face, this is similar to the practices of, say, NICE – the UK agency that bargains for medicine on behalf of the NHS, which also bargains with pharma companies for access to everyone in the UK and gets very good deals as a result.

But OptumRX doesn't bargain for a lower list price. They bargain for a bigger rebate. That means that the "price" is still very high, but OptumRX ends up paying a tiny fraction of it, thanks to that rebate. In the OptumRX formulary, Lantus insulin lists for $403. But Sanofi, who make Lantus, rebate $339 of that to OptumRX, leaving just $64 for Lantus.

Here's where the scam hits. Your insurer charges you a deductible based on the list price – $404 – not on the $64 that OptumRX actually pays for your insulin. If you're in a high-deductible plan and you haven't met your cap yet, you're going to pay $404 for your insulin, even though the actual price for it is $64.

Now, you'd think that your insurer would put a stop to this. They chose the PBM, the PBM is ripping off their customers, so it's their job to smack the PBM around and make it cut this shit out. So why would the insurers tolerate this nonsense?

Here's why: the PBMs are divisions of the big health insurance companies. Unitedhealth owns OptumRx; Aetna owns Caremark, and Cigna owns Expressscripts. So it's not the PBM that's ripping you off, it's your own insurance company. They're not just making you pay for drugs that you're supposedly covered for – they're pocketing the deductible you pay for those drugs.

Now, there's one more entity with power over the PBM that you'd hope would step in on your behalf: your boss. After all, your employer is the entity that actually chooses the insurer and negotiates with them on your behalf. Your boss is in the driver's seat; you're just along for the ride.

It would be pretty funny if the answer to this was that the health insurance company bought your employer, too, and so your boss, the PBM and the insurer were all the same guy, busily swapping hats, paying for a call center full of tormented drones who each have three phones on their desks: one labeled "insurer"; the second, "PBM" and the final one "HR."

But no, the insurers haven't bought out the company you work for (yet). Rather, they've bought off your boss – they're sharing kickbacks with your employer for all the deductibles and co-pays you're being suckered into paying. There's so much money (your money) sloshing around in the PBM scamoverse that anytime someone might get in the way of you being ripped off, they just get cut in for a share of the loot.

That is how the PBM scam works: they're fronts for health insurers who exploit the existence of high-deductible plans in order to get huge kickbacks from pharma makers, and massive fees from you. They split the loot with your boss, whose payout goes up when you get screwed harder.

But wait, there's more! After all, Big Pharma isn't some kind of easily pushed-around weakling. They're big. Why don't they push back against these massive rebates? Because they can afford to pay bribes and smaller companies making cheaper drugs can't. Whether it's a little biotech upstart with a cheaper molecule, or a generics maker who's producing drugs at a fraction of the list price, they just don't have the giant cash reserves it takes to buy their way into the PBMs' formularies. Doubtless, the Big Pharma companies would prefer to pay smaller kickbacks, but from Big Pharma's perspective, the optimum amount of bribes extracted by a PBM isn't zero – far from it. For Big Pharma, the optimal number is one cent higher than "the maximum amount of bribes that a smaller company can afford."

The purpose of a system is what it does. The PBM system makes sure that Americans only have access to the most expensive drugs, and that they pay the highest possible prices for them, and this enriches both insurance companies and employers, while protecting the Big Pharma cartel from upstarts.

Which is why the FTC is suing the PBMs for price-fixing. As Stoller points out, they're using their powers under Section 5 of the FTC Act here, which allows them to shut down "unfair methods of competition":

https://pluralistic.net/2023/01/10/the-courage-to-govern/#whos-in-charge

The case will be adjudicated by an administrative law judge, in a process that's much faster than a federal court case. Once the FTC proves that the PBM scam is illegal when applied to insulin, they'll have a much easier time attacking the scam when it comes to every other drug (the insulin scam has just about run its course, with federally mandated $35 insulin coming online, just as a generation of post-insulin diabetes treatments hit the market).

Obviously the PBMs aren't taking this lying down. Cigna/Expressscripts has actually sued the FTC for libel over the market study it conducted, in which the agency described in pitiless, factual detail how Cigna was ripping us all off. The case is being fought by a low-level Reagan-era monster named Rick Rule, whom Stoller characterizes as a guy who "hangs around in bars and picks up lonely multi-national corporations" (!!).

The libel claim is a nonstarter, but it's still wild. It's like one of those movies where they want to show you how bad the cockroaches are, so there's a bit where the exterminator shows up and the roaches form a chorus line and do a kind of Busby Berkeley number:

https://www.46brooklyn.com/news/2024-09-20-the-carlton-report

So here we are: the FTC has set out to euthanize some rentiers, ridding the world of a layer of useless economic middlemen whose sole reason for existing is to make pharmaceuticals as expensive as possible, by colluding with the pharma cartel, the insurance cartel and your boss. This conspiracy exists in plain sight, hidden by the Shield of Boringness. If I've done my job, you now understand how this MEGO scam works – and if you forget all that ten minutes later (as is likely, given the nature of MEGO), that's OK: just remember that this thing is a giant fucking scam, and if you ever need to refresh yourself on the details, you can always re-read this post.

The paperback edition of The Lost Cause, my nationally bestselling, hopeful solarpunk novel is out this month!

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/09/23/shield-of-boringness/#some-men-rob-you-with-a-fountain-pen

Image:

Flying Logos (modified)

https://commons.wikimedia.org/wiki/File:Over_$1,000,000_dollars_in_USD_$100_bill_stacks.png

CC BY-SA 4.0

https://creativecommons.org/licenses/by-sa/4.0/deed.en

#pluralistic#matthew stoller#pbms#pharmacy benefit managers#cigna#ftc#antitrust#intermediaries#bribery#corruption#pharma#monopolies#shield of boringness#Caremark#Express Scripts#OptumRx#insulin#gbw#george w bush#co-pays#obamacare#aca#rick rules#guillotine watch#euthanize rentiers#mego

401 notes

·

View notes

Text

things to remember in 2023

goodbye emo era, goodbye empath era, goodbye all you eras that have been putting others + emotions at the center of everything. hello self-serving era. self-serving, not selfish. see, more accurate vocabulary can make all the difference.

choose people who choose you. bare minimum is not impressive. it’s only an indicator that hmmm maybe I can explore what something with this person could lead to. it’s the basic eligibility criteria for opening up your time/schedule to someone, not heart. only time.

new people don’t need to know life stories and trauma from before 2018. if you want to talk about it just write about it, write it into your book.

do not listen to your parents. I mean this in the most respectful possible way. you are an adult now, you make your own decisions. because 20 years from now if you are sad and miserable and hating your life and you tell them hey it’s because you made me la la la chances are they are going to turn around and be like nobody forced you, you were an adult, you made your own decisions. so just make your own decisions. and they would be right. like just dodge the emotional manipulation and the drama and the guilt and lack of validation from them for a bit and go ahead and do things you want to in your life. and you already have daddy issues, right? pacify them in bed or something idk. just make your own bloody decisions independent of what your family/others expect of you.

explore more Hindi music.

channelize certain things you’ve seen in most men around you. channelize compartmentalization. channelize binary problem solving. channelize cutting your losses and exiting at the right time from romantic situations that do not have any future no matter how much you feel for them in the present.

do not force yourself to write fiction. maybe you don’t want to create stories. maybe you just want to write down what you already know. maybe you just want to write creative non-fiction. why is that a bad thing? don’t you think it’s time to let go of the ideas you have hyper-romanticized and see things for what they really are and then work with them?

dating apps are not where you will find love. hook-ups, maybe. but drama-free hook-ups? yeah, not quite sure about that either. let’s just go back to how we were before? let’s just focus on our life and believe that love will happen if and when it’s supposed to?

self-dates must make a return. you found that amazing second-hand bookseller next to your home and your favourite cafe from Bangalore is now in Mumbai and so many new art galleries are opening up around and when was the last time you went to Marine Drive and maybe it’s time to sneak into your college to go have your favourite food again from the canteen and maybe after work you can stay around and explore the popular bars and maybe you can find a post office next to your new apartment so you can start sending letters and packages to your best friend again. I know, I know 2022 was a year of such dramatic highs that gave you such adrenaline rush that coming back to things that were more grounded and brought you joy seems difficult but baby please. you cannot run towards psychosis so soon, okay? come back.

on that note, let’s find a yoga class around your apartment and also a gurudwara.

sign up for experiences and invest for the long term but do not invest in material things like furniture. at this point you are the typical mid-20s person who is free to up and leave whenever and wherever and you haven’t found a place you want to call home yet anyway. so keep your money liquid, don’t lock it up in stupid things, but invest for the long-term in equity assets to create wealth. also, go meet your accountant please. and get life insurance.

do not let family stuff get to you emotionally. deal with it in a logistic, functional, and objective way. as much as possible.

you really don’t have to respond to people within 24 hours, 48 hours, or even a week. I mean other than very few selected people (family, best friend, and your partner), nobody is owed your immediate attention. and even these inner circle people are owed your immediate attention only in a way where you keep them in the loop to let them know you are alive and doing okay.

you are a warm person and it’s easy for people to like you wherever you go. but you have such limited time, energy, and brain cells. you cannot scale yourself like a company. which means if you more people want to get to know you, talk to you, etc., you can’t supply them with that because you are not a scalable product. okay? okay.

earning more money will help only in a limited manner if you do not budget and control your spending. it’s not the person who earns more that is rich but the person who saves and invests and doesn’t take debt for consumption purposes. you can no longer be the ironic financial writer like in the confessions of a shopaholic. you are no longer a kid, you are an adult who has to take care of yourself and soon your dependents and so you cannot keep ranting on about capitalism while falling constant prey to it. instead you have to benefit from it.

figure out what is your choice of poison. for when you wanna just vibe, for when you want to get drunk drunk, for when you wanna be bhand. figure it out.

think of studying Korean as doing an undergrad degree. so you know you have to stick with this for the next three years. this way you don’t see it as a short-term fancy but as a longer term commitment and reach level 6 of fluency in the language. this way, by the time you are in your late 20s, you will actually be able to read Korean books in Hangul and not the English translation. that’s your goal, isn’t it? and writing poetry in Korean too.

your high school friend answered the question no doctor was. when you drink alcohol, make sure there is a 3-hour gap between that and your medication. but also keep the drinking in check. I mean honestly, iced coffee and fresh fruit juices for the win.

you go through people like you go through books. but people are not books. time to pick up actual books again and press pause on people.

do not commit anything to anybody because you have no sense of stability or certainty in your life right now. that doesn’t make you flighty. that doesn’t make you irresponsible. in fact, it makes you responsible because you aren’t making promises you aren’t sure you are capable of keeping even if you want to keep them. actions > intentions.

time to have a skincare routine. your sister has written you a whole blog on it - just follow that.

also oh my god. being twenty five/twenty six does not make you old. you don’t have to look at the younger people you interact with and feel uncool or outdated because then that’s how you’ll always feel. like when you were younger, you would look at the older people and think they are so cool, graceful, smart, and badass. divine, even. then that’s what you are becoming now. not knowing what certain emojis and slang means really has no bearing on how relevant you are.

this isn’t an exhaustive list, so come back. don’t just write this and forget all about it. come back, review, revise, add. but most importantly, remember. remember this is for you. so that you minimise pain and failure and shitty feelings and maximise peace and success and joy. and you do like optimum utilisation of resources, don’t you? so do that. apply yourself for yourself. that’s where the returns are the highest.

#2023#happy new year#writerscreed#poeticstories#poetryportal#twc poetry#notes to self#things to look forward to#things to remember#things to remind myself#happy 2023#new year#New Year Resolutions#goals#self development#healing#mental health#lists#desiblr#investing#economics#writers on tumblr#poets on tumblr#january 2023#creatingnikki

995 notes

·

View notes

Text

Femme Fatale Guide: How To Master Your Money & Tips On Financial Literacy

Understanding and taking control of your finances improves your quality of life in many ways. Making strides toward better financial literacy can save you a lot of stress, unnecessary fees and helps you play a more active role in taking control over this aspect of adulthood. Once you understand the game of money, saving, and investing, it becomes infinitely simpler to devise a plan to set yourself up for a more financially-free future. Here are some practical tips to keep your finances streamlined, secure, and systemized to help you gain more financial literacy and win in this area of life.

Overview:

Track Your Income & Expenses

Set Financial Goals & Realistic Limitations

Invest Higher-Quality Items To Save Later

Educate Yourself On Different Types of Banking & Investment Accounts

Establish Credit, But Know Yourself

Create An Emergency Fund

Leverage Credit Card Benefits

Understand The Power of A Roth IRA (or Backdoor Roth IRA) & HSA

Automate Whenever Possible

Get Familiar With Taxes & Write-offs

Stay Informed About Employer Benefits

Purchase Seasonally & With Discount Codes (When Available)

Protect Yourself

Read Books

Seek Expert Advice

TIPS ON MASTERING FINANCIAL LITERACY:

Track Your Income & Expenses: Always have a record of all of the money going in and out of your accounts. Use the tool on your banking account app(s) to confirm your monthly income and expenses. Tools like Mint also are great to track your spending to see where every dollar is going all in one place. Aside from personal use, for small business owners, Quickbooks is my favorite invoicing and expense-tracking option.

Set Financial Goals & Realistic Limitations: Once you know your exact monthly income, budget your essentials, savings, investments, and fun money accordingly. Make sure necessities like rent, food, health insurance, electricity, WiFi, toiletries, etc. are accounted for before anything else. Depending on your financial situation, experts (not me – I try to educate myself as best as I can, but am no expert!) recommend trying to save and invest between 15-30% of your pre-tax income. Give yourself the liberty to spend the rest (say 15-20%) of your income, so you don’t feel deprived and stay on track with your goals.

Invest Higher-Quality Items To Save Later: Initially purchasing a higher-quality item often cuts your overall expenses in a certain area over the long run. (Ex: Well-made clothing, shoes, furniture, kitchen appliances, coffee maker, hair dryer, etc.). If you invest upfront on an item you regularly use, there’s a lower chance that it will deteriorate, rip, break, or otherwise become unusable for the next few years. When you opt for the cheaper option, this practice might save you a few bucks in the short term, but you will probably end up having to replace it a few times over time and spend more in the long run. This tip might seem counterintuitive to some, but it truly does save you a lot of money (and frustration). However, I will place a caveat here and say that this advice comes from a place of privilege. Never purchase something you can’t afford. If you have the means, spend a bit more upfront - it is better for your future wallet, allows you to indulge in a better quality of life, and helps you let go of any scarcity mindset/financial limiting beliefs.

Educate Yourself On The Different Types of Banking & Investment Accounts: Know the differences between and the use purpose of different accounts: Checking, Savings, CDs, 401K, Roth IRA, HSA, etc. Always opt for a high-yield savings account option to help preserve your money’s value over time with rising living costs and inflation.

Establish Credit, But Know Yourself: Your credit score is like your adult report card. It’s essential for so many aspects of life, like renting or buying a home, insurance, cell phone plans, etc., so it’s important to start building your credit as early as you can. However, if you know you’re the type of person to overspend with a credit card, look into secured credit card options (you deposit the money that acts as a credit limit, so it’s like a debit card with credit-building benefits).

Create An Emergency Fund: Pay yourself first. Have between 3-12 months of expenses available in a high-yield savings account at all times. If you have a family or are self-employed, aim for 6-12 months of necessary savings to stay sane. Saving this amount of money takes time. Be patient, and cut back on frivolous expenses if needed for the short term.

Leverage Credit Card Benefits: If you have enough self-control, always use a credit card instead of a debit card – but spend in the same way you would as though the money is coming directly out of your bank account. This gives you additional flight and other purchasing perks, such as cashback and exclusive discounts. Using a credit card provides additional security, too.

Understand The Power of A Roth IRA (or Backdoor Roth IRA, depending on your income) & HSA: Compound interest is your best friend financially. Depending on your income, invest as much as you can into a Roth IRA account or set up a backdoor Roth IRA through your brokerage firm (I use Vanguard!). HSA (Health Saving Accounts) accounts offer so many benefits – they can serve as a tax write-off, lower your overall healthcare costs, and be leveraged to use as an additional retirement investment account, too (I use Fidelity).

Automate Whenever Possible: Automate a portion of your paycheck to savings and your investments, so you never see this money. Pay yourself first before spending (on anything but necessities).

Get Familiar With Taxes & Write-offs: This mainly applies to anyone self-employed or a small business owner (been in the game for 5 years!). However, this point can also potentially be beneficial for students who can leverage an education credit for tax purposes. Explore all of your options to see what write-offs are available in your specific situation. Understand how your income and expenses influence your tax bracket. Investing in a CPA can save you a considerable amount of money and all of your sanity if you’re not a salaried employee. Look over the standardized section C document, and speak with a professional to help maximize your write-off potential (legally and honestly, of course). My CPA is my lifeline!

Stay Informed About Employer Benefits: Always maximize your 401K match (whatever percentage that is at your company), any wellness perks (like a gym membership or massage credit), or any meals and car services credits for late nights/work trips.

Purchase Seasonally & With Discount Codes (When Available): Try to purchase items off-season when you can (e.g. purchase classic winter closet staples in the summer when they’re on sale). Utilize plug-ins like Honey or Cently on your browser to have discount codes for any site readily available.

Protect Yourself: Stay on top of fraud alerts. Freeze your credit bureau accounts if necessary.

Read Books: Educate yourself on saving, investing, budgeting, building a business, etc. See the ‘Finance’ section of my Femme Fatale Booklist for some recommendations. I also love Graham Stephan’s Youtube channel – his videos are highly useful and practical for beginners in this life arena!

Seek Expert Advice: Use licensed professionals (CPAs, brokerage firms, your bank, etc.) as a resource, too, for your personal goals.

This is a lot to take in, so try to implement one action item (or a few) at a time, so you can work towards your goals without getting overwhelmed. Also, for reference, I’m in the United States, so all of these tips are focused on how the system works in my country - if you know of any international equivalents, feel free to drop them in the comments to guide others.

Hope this helps xx

#life advice#finance#adulting#femme fatale#dark femininity#dark feminine energy#it girl#hypergamy#high value woman#divine feminine#high value mindset#hypergamous#the feminine urge#success mindset#productivity#spending habits#entreprenuership#level up#self improvement#ideal self#female power#female excellence#personal growth#investing#girl advice#that girl#femmefatalevibe

1K notes

·

View notes

Text

Hello So yesterday I broke my wheelchair when head and home from therapy and I need a new one so I made this go fund me so please check it out. If you don't know, wheelchairs cost a lot of money on the cheap end for a decent one It's like 500$ and for 1 I could actually use long term. Wood cost me a little over a 1000. I don't have Insurance. And I am not able to get a doctor to give me a note if I could my lawyer would cover the cost. But I no longer have a family doctor and walking doctors won't do it. This is the link, please consider checking it out or at least sharing.

317 notes

·

View notes

Text

Ko-Fi prompt from Isabelo:

Hi! I'm new to the workforce and now that I have some money I'm worried it's losing its value to inflation just sitting in my bank. I wanted to ask if you have ideas on how to counteract inflation, maybe through investing?

I've been putting this off for a long time because...

I am not a finance person. I am not an investments person. I actually kinda turned and ran from that whole sector of the business world, at first because I didn't understand it, and then once I did understand it, because I disagreed with much of it on a fundamental level.

But... I can describe some factors and options, and hope to get you started.

I AM NOT LEGALLY QUALIFIED TO GIVE FINANCIAL ADVICE. THIS IS NOT FINANCIAL ADVICE.

What is inflation, and what impacts it?

Inflation is the rate at which money loses value over time. It's the reason something that cost 50 cents in the 1840s costs $50 now.

A lot of things do impact inflation, like housing costs and wage increases and supply chains, but the big one that is relevant here is federal interest rates. The short version: if you borrow money from the government, you have to pay it back. The higher the interest rates on those loans, the lower inflation is. This is for... a lot of reasons that are complicated. The reason I bring it up is less so:

The government offers investments:

So yeah, the feds can impact inflation, but they also offer investment opportunities. There are three common types available to the average person: Bonds, Bills, and Notes. I'll link to an article on Investopedia again, but the summary is as follows: You buy a bill, bond, or note from the government. You have loaned them money, as if you are the bank. Then, they give it back, with interest.

Treasury Bills: shortest timeframe (four weeks to a year), and lowest return on investment. You buy it at a discount (let's say $475), and then the government returns the "full value" that the bond is, nominally (let's say $500). You don't earn twice-yearly interest, but you did earn $25 on the basis of Loaning The Government Some Cash.

Treasury Notes: 2-10 year timeframe. Very popular, very stable. Banks watch it to see how they should plan the interest rates for mortgages and other large loans. Also pretty high liquidity, which means you can sell it to someone else if you suddenly need the cash before your ten-year waiting period is up. You get interest payments twice a year.

Treasury Bonds: 20-30 years. This is like... the inverse of a house mortgage. It takes forever, but it does have the highest yield. You get interest payments twice a year.

Why invest money into the US Treasury department, whether through the above or a different government paper? (Savings bonds aren't on sold the set schedule that treasury bonds are, but they only come in 30-year terms.)

It is very, very low risk. It is pretty much the lowest risk investment a person can make, at least in the US. (I'm afraid I don't know if you're American, but if you're not, your country probably has something similar.)

Interest rates do change, often in reaction or in relation to inflation. If your primary concern is inflation, not getting a high return on investment, I would look into government papers as a way to ensure your money is not losing value on you.

This is the website that tells you the government's own data for current yield and sales, etc. You can find a schedule for upcoming auctions, as well.

High-yield bank accounts:

Savings accounts can come with a pretty unremarkable but steady return on investment; you just need to make sure you find one that suits you. Some of the higher-yield accounts require a minimum balance or a yearly fee... but if you've got a good enough chunk of cash to start with, that might be worth it for you.

They are almost as reliable as government bonds, and are insured by the government up to $250,000. Right now, they come with a lower ROI than most bonds/bills/notes (federal interest rates are pretty high at the moment, to combat inflation). Unlike government papers, though, you can deposit and withdraw money from a savings account pretty much any time.

Certificates of Deposit:

Okay, imagine you are loaning money to your bank, with the fixed term of "I will get this money back with interest, but only in ten years when the contract is up" like the Treasury Notes.

That's what this is.

Also, Investopedia updates near-daily with the highest rates of the moment, which is pretty cool.

Property:

Honestly, if you're coming to me for advice, you almost definitely cannot afford to treat real estate as an investment thing. You would be going to an actual financial professional. As such... IDK, people definitely do it, and it's a standby for a reason, but it's not... you don't want to be a victim of the housing bubble, you know? And me giving advice would probably make you one. So. Talk to a professional if this is the route you want to take.

Retirement accounts:

Pension accounts are a kind of savings account. You've heard of a 401(k)? It's that. Basically, you put your money in a savings account with a company that specializes in pensions, and they invest it in a variety of different fields and markets (you can generally choose some of this) in order to ensure that the money grows enough that you can hopefully retire on it in fifty years. The ROI is usually higher than inflation.

These kinds of accounts have a higher potential for returns than bonds or treasury notes, buuuuut they're less reliable and more sensitive to market fluctuations.

However, your employer may pay into it, matching your contribution. If they agree to match up to 4%, and you pay 4% of your paycheck into an pension fund, then they will pay that same amount and you are functionally getting 8% of your paycheck put into retirement while only paying for half of it yourself.

Mutual Funds:

I've definitely linked this article before, but the short version is:

An investment company buys 100 shares of stock: 10 shares each in 10 different "general" companies. You, who cannot afford a share of each of these companies, buy 1 singular share of that investment company. That share is then treated as one-tenth of a share of each of those 10 "general" companies. You are one of 100 people who has each bought "one stock" that is actually one tenth of ten different stocks.

Most retirement funds are actually a form of mutual fund that includes employer contributions.

Pros: It's more stable than investing directly in the stock market, because you can diversify without having to pay the full price of a share in each company you invest in.

Cons: The investment company does get a cut, and they are... often not great influences on the economy at large. Mutual funds are technically supposed to be more regulated than hedge funds (which are, you know, often venture capital/private equity), but a lot of mutual funds like insurance companies and pension funds will invest a portion of their own money into hedge funds, which is... technically their job. But, you know, capitalism.

Directly investing in the stock market:

Follow people who actually know what they're doing and are not Evil Finance Bros who only care about the bottom line. I haven't watched more than a few videos yet, but The Financial Diet has had good energy on this topic from what I've seen so far, and I enjoy the very general trends I hear about on Morning Brew.

That said, we are not talking about speculative capital gains. We are talking about making sure inflation doesn't screw with you.

DIVIDENDS are profit that the company shares to investors every quarter. Did the company make $2 billion after paying its mortgages, employees, energy bill, etc? Great, that $2 billion will be shared out among the hundreds of thousands of stocks. You'll probably only get a few cents back per stock (e.g. Walmart has been trading at $50-$60 for the past six months, and their dividends have been 57 cents and then 20.75 cents), but it adds up... sort of. The Walmart example is listed as having dividends that are lower than inflation, so you're actually losing money. It's part of why people rely on capital gains so much, rather than dividends, when it comes to building wealth.

Blue Chip Stocks: These are old, stable companies that you can expect to return on your investment at a steady rate. You probably aren't going to see your share jump from $5 to $50 in a year, but you also probably won't see it do the reverse. You will most likely get reliable, if not amazing, dividends.

Preferred Stocks: These are stock shares that have more reliable dividends, but no voting rights. Since you are, presumably, not a billionaire that can theoretically gain a controlling share, I can't imagine the voting rights in a given company are all that important anyway.

Anyway, hope this much-delayed Intro To Investing was, if not worth the wait, at least, a bit longer than you expected.

Hey! You got interest on the word count! It's topical! Ish.

#economics#capitalism#phoenix talks#ko fi#ko fi prompts#research#business#investment#finance#treasury bonds#savings bonds#certificate of deposit#united states treasury#stocks#stock market#mutual funds#pension funds

65 notes

·

View notes

Text

How I Built an Emergency Fund, inspiration I deeply hope is helpful

As the blog URL says, this is not financial advice. This is how I did this thing, and I am posting it here, publicly, in hopes that it helps you should you need this information.

In short: Remix this advice to what fits your life + do not sue me if this goes poorly for you. This is for Americans, if you do not live in America and/or your money is not in America, I hope this is a useful base.

None of these links are affiliate links.

I write these things as a mental shift. I like to ramble and I wish I had someone tell me this stuff 20+ years ago. I'm hoping this helps you.

This is an incredibly long post so I'm putting it under a KEEP READING.

This post goes over two stages: "short term + not life-or-death" and "long term + actual life or death"

Part 01: SHORT TERM + NOT LIFE-OR-DEATH FUND

You need to find a high yield savings account that is FDIC insured. Ally is a popular bank for this.

Functionally, the only difference between a "high yield savings account" and "savings account" from the giant conglomerate bank down the street is the interest rate.

I do not know why non-high-yield savings accounts exist. I'm guessing because legally they can, and I hate it.

Moving away from my personal socioeconomic views to return to advice.

"FDIC insured" is not something you pay for. It is nearly universal on savings accounts. If a savings account, or a checking account, does NOT have it, then you should not put your money there. Something is wrong with that bank.

FDIC means if your bank goes out of business, your account is insured up to $250,000, per account, by the government. So if your bank goes out of business, the government makes sure you still have your cash (up to $250k).

A high-yield savings account means your cash is available whenever you need it.

Other products, like CDs, exist, but this ramble is designed to be as simple and starter as possible. Begin with a high yield savings account, build up from there as you do your own research + compare this to your needs.

Do not accept an account that has minimum balances. Do not open an account with monthly fees.

Touch this account as little as possible.

For every $1 you put in, every month, a few pennies will materialize. It's not much, but the main point is at every level, your money works for you.

Rich people do this. You can too.

Touch this account as little as possible.

You can have multiple savings accounts.

I personally have a savings account in the above structure designed for "oh hell I am kinda screwed, but will be okay, just need a buffer."

"How much should I have in there?" you might ask. Common advice says "3-6 months expenses" which is a lot. I say "start with literally $1 and continue as you can until comfortable with what is possible, for you, at this time."

Will $1 make you rich? No.

Will it save your life in a bad situation? Probably not.

Does this $1 essentially become a tiny robot that is making you money for as long as it is docked into its cargo bay? ...weird metaphor but we'll go with it, sure.

Ultimately is it a start? Yes.

You can have multiple savings accounts. You can have a savings account "this is for short term emergencies" and "this is for... slightly less short term" etc.

It costs you nothing to have multiple. They all operate in the same way. It's handy to have them all at the same bank because it can make transferring cash easier.

Part 02: LONG TERM + ACTUAL LIFE-OR-DEATH FUND WITH RISK SO BE CAREFUL

Once you have your savings account set up, and it's being funded on a regular basis (every week, every paycheck, every month, every quarter -- whatever works for you), look into creating a second, bigger, more dangerous-term cash reserve.

I like my Roth IRA. This is a link to a proper finance blog that has a lot of details. I am trying to make this handy/simple to get started.

401ks and (non-Roth) IRAs are funded with pre-tax dollars, frequently in conjunction with your job.

Normally, cash goes from job -> government takes a slice -> you.

Pre-tax retirement accounts, cash goes from job -> retirement takes the percentage you decide -> government takes a slice of what is left -> you

Roth IRAs, job -> government takes a slice -> you -> Roth IRA

The benefit to pre-tax retirement accounts being, because the cash going in is pre-tax, there is more of it.

It can grow faster in the stock market or other places your particular fund allows you to put cash into.

The taxes come out when you withdraw -- usually retirement -- because if you withdraw before you retire, you are heavily penalized with extra fees.

That's why Part 02 is a ROTH IRA. Your money has already been taxed -- job -> government's slice -> you -> Roth IRA.

This means the money is yours, already taxed. If you withdraw the gains, those get taxed, but the base, that's yours.

If you invest $100 and it grows to $105, you can withdraw $100 without paying fees or taxes. If you withdraw that extra $5, that is when taxes start to come into play. If you withdraw $100, and leave the $5, the $5 continues to grow, and that extra growth is taxed if withdrawn. So try not to touch it (ideally you leave all of it until retirement).

This is why this is an emergency, life-or-death only, account. You tap it only when you need to when all other choices are wretched and ruinous.

There is an annual limit as to how much money you can put into a Roth IRA (several thousand bucks).

You can start them very small. Like $20 or maybe less.

Look for a bank or institution that does not charge fees to open and maintain one.

AT EVERY STEP YOU SHOULD BE AVOIDING FEES

Here are smart people talking about ideas on how to get started.

Okay, so, what do we do now with this fancy roth thing.

Here is where things get... uncomfortable.

A Roth IRA is an account type.

You need to do something with your money.

The reason you have this in addition to, and secondary to, your high-yield savings account is because this is an investment vehicle, the balance is going to go up and down, and may reach $0.00.

For my Roth IRA, I like "exchange traded funds" -- ETFs.

There are a lot of options -- you can invest in most anything

Because my Roth IRA is built for "help me I'm dying" emergencies, I invest in a mix of S&P 500 index funds and small-cap funds.

SO MANY WORDS.

Let's break this down what this means.

S&P 500 index funds: This is an index fund of giant, giant, giant companies.

An index fund is like a stock. But instead of a single company, it tracks (owns shares of) an index -- like the DOW or Nasdaq. Or countries. Or... the entire market for oil. Etc.

The metaphor isn't completely accurate, but I like to think of it as "an index fund is a company that owns tiny bits of other companies."

Like, okay, say you have SlimeIndexFund and a share price is $40.

In this example, SlimeIndexFund owns $10 worth of "BardCo" and $10 of "ThiefCo" and $10 of "MermaidCo" and $10 of "EvilCo".

Let's say EvilCo does a lot of evil and is now worth $15, and MermaidCo does a lot of mermaid stuff and is now worth $15, and BardCo sings out of tune so is now worth $5. ThiefCo is oddly at the same $10 but we're scared so we're leaving ThiefCo to stay at $10.

A share in SlimeIndexFund is now worth $45. ($5 BardCo + $10 ThiefCo + $15 EvilCo + $15 MermaidCo)

This is diversification

Because I bought an index fund, instead of just buying BardCo, my risk is less.

Had I bought all MermaidCo, my return would be higher -- but this is a much bigger risk.

The entire purpose of this set up of a Roth IRA is TO MINIMIZE RISK.

Your Roth IRA should allow you to buy "fractional shares" and if it doesn't fuck that bank, go somewhere that does.

In the above example, SlimeIndexFund is $40/share and at that price you are getting the full benefit of 1 share.

Let's say you have $10.

You buy a fractional share of SlimeIndexFund for $10, which is 25% of 1 share.

So when SlimeIndexFund shares raise from $40 -> $45, your fractional share goes from $10 -> $12.50.

Not all funds and stock shares (etc) have fractional shares, most do.

It's a great way to start and build.

Small-cap funds: These operate in literally the same way. The difference is the companies are (in comparison) much smaller. They tend to be more nimble.

So I am diversifying between "here is a fund, it has a lot of large companies" and "here is a fund, it has a lot of small companies."

Let's say Big Office Building real estate goes down, but the sale of Small Company Making waffles goes up. This mixes together and I'm less in danger of losing money, or losing much money.

You can pick individual stocks.

The reason it is not recommended, by nearly everyone, is because the market has incredible tools and power over individual stocks.

By using any kind of fund that bundles things together, you are thereby automatically using these tools by proxy

It is critical to understand this is the stock market. Your account will go up and down. It may go down A LOT, like 25%, and take years to recover. Maybe it goes down 100% to literally $0.00.

That's why this is the LAST RESORT EMERGENCY FUND.

So why are we doing this.

This feels... wrong?

The potential for growth is significantly higher than a savings account. Adjusted for inflation, somewhere in between 6-7%.

At this rate, if you can leave your initial deposit alone for somewhere between 10 - 13 years, it has doubled.

This equation recalculates every time you make a deposit. So if you can deposit $20 every pay check, it has the potential to grow very quickly.

As above, this is the stock market, so it can also get wiped out.

But given the stock market has historically always recovered, though it may take several years, the risk is worth it to me + a lot of other people.

The reason this is built as a last-resort cash bucket is because of this risk. Before moving into this arena, you should have other cash buckets as a buffer.

Your RISK is it goes down. Which it will frequently.

Your REWARD is if it goes up. Which historically it has far more than it went down.

The PURPOSE of using funds as described above is so you don't have try to guess who the next Amazon is and wind up picking the next Pets.com (which went out of business, like, a long... long time ago).

The people making the funds figure out who is Amazon and who is Pets.com and work, day and night, to make your money grow and/or protect it when outside influences are hurting the market.

They are incredibly equipped to do this and their literal livelihood is on the line when they do it poorly.

Which is a polite way of saying, they are continuously incentivized above all else to work for the fund you're investing in.

The reason you're doing this in a Roth IRA specifically is you're hoping to keep as much of it intact, as possible, until you retire, at which point -- if you've followed fairly simple rules -- you withdraw the base and gains tax-free.

Whereas money in a normal stock account? Those gains are taxable every year.

"I have literally $20 I can save per pay check! Can I put in $15 into a high-yield savings account and $5 into a Roth IRA to get started?!"

Yes!

Also, congrats! You're diversifying already!

Your Roth IRA broker should allow you to invest a minimum of $1 at a time, and buy fractional shares. If they don't, don't sign up with them!

Lean heavily into your high-yield savings account until that is very comfortable and thick, then push money into the Roth IRA.

Your goal is to build a system that works for you -- both literally (money working for you) and emotionally ("this is comfortable")

"Should I pay off debt before proceeding? A lot of people say to pay off excess debt first."

This is up to you.

Most financial blogs etc. do say "focus on paying off debt first" -- it's good advice, your returns are risk-free and permanent, since the lower your debt is, the less you have to pay over time.

Interest -- working for you or against you -- is continuous and eternal.

Personally, I like to diversify everything, so I not-financial-advice ramble "do all three -- pay down debt, throw a little cash into a high-yield savings, throw a little cash into a Roth IRA"

The problem with "pay off debt first" is that it misses out any occasional giant gains the stock market makes (Roth IRA) and introduces the risk of "I have paid this credit card on time for 5 years, I'm short on change for 3 months due to a situation that gets resolved quickly, and now I have a late payment fee, and a higher interest rate."

Look at your life, finances, and potential future and make decisions!

And also:

Always be on the look out for deals with banks. Sign up bonuses, referral links from friends, etc. Think of it as a money sale.

If you are not comfortable with the idea of a Roth IRA hitting $0.00 potentially, do not do step 02. These are ideas, not directives.

All financial tools can be used for different purposes. All of them. Thus -- these are ideas, not directives.

I am listing a few examples of banks, funds, etc. These are not recommendations nor are they affiliate links. They are listed because I want to maximize your start on this path, but caution, in strongest possible terms, you must do your own research and figure out what makes sense for you.

There are a lot of nuances I am paving over for the sake of simplicity, which is why I am continually saying...

...c'mon say it with me...

...you must do your own research before continuing

Smart, free sites that cover this + a lot of other stuff:

NerdWallet

Bank Rate

One final note about Roth IRAs:

Robinhood currently is offering a 1% match on an IRA. Considering the strict limits of how much an IRA can intake per year, it's not much, but it doesn't cost you anything. Money on sale!

As a final note -- always feel comfortable asking people handling your money for help. They are working for you. Your money works FOR YOU.

If you are uncomfortable, leave, immediately, without concern.

At the retail level, there are hundreds of banks and financial institutions clamoring for your business. If someone makes you uncomfortable for not knowing something, or getting a term wrong, or asking "too many" questions -- go somewhere else.

It doesn't matter if your account is literally worth $20.

They are working for you.

This is a business transaction, and if they make you feel like your time isn't worth their business, I promise you there is someone else who will gladly take care of you.

I end with -- whenever someone is giving you financial advice, always ask why. It helps ensure they aren't scamming you, it's just a good business practice.

I like to ramble, it helps me mentally

I like to be useful, I want the world to be significantly more balanced in terms of who is doing okay

I like to write, this is all good practice for me in doing Various Other Things I do

I fucking hate predatory financial practices. I was gatekept out of financial literacy for decades and so every time I help someone else figure out how to set up their own life and protect themselves it is a giant "fuck you" to the systems and directly to the people who stood in my way.

567 notes

·

View notes

Text

NEW POST!

Short-Term Disability Insurance Is a Waste of Money… With Two Very Specific Exceptions

Here's an excerpt:

"In preparation for this article, I read a lot of stories from people who filed short-term disability insurance claims. I was dismayed but not surprised to see just how many people experience claim rejections.

As this ProPublica report explains, the claims rejection process is so murky it could easily be mistaken for a Rainbow Brite villain. On average, 20% of claims are rejected. But it’s often wildly erratic. One company rejected 66% of claims in one year, and 7% the next. And the sole arbiter of the claim is, of course, the insurance company itself. You know: the entity that has vast resources and a compelling financial interest in denying those claims?

HI, I DON’T LIKE THIS."

Keep reading.

#disability insurance#disability pride month#disability rights#employer#income insurance#insurance#short-term disability insurance#workplace benefits#disability

38 notes

·

View notes

Text

Coronavirus vaccines, once free, are now pricey for uninsured people - Published Sept 3, 2024

As updated coronavirus vaccines hit U.S. pharmacy shelves, adults without health insurance are discovering the shots are no longer free, instead costing up to $200.

The federal Bridge Access Program covering the cost of coronavirus vaccines for uninsured and underinsured people ran out of funding. Now, Americans with low incomes are weighing whether they can afford to shore up immunity against an unpredictable virus that is no longer a public health emergency but continues to cause long-term complications and hospitalizations and kill tens of thousands of people a year.

The program’s elimination marks the latest tear in a safety net that once ensured people could protect themselves against the coronavirus regardless of their financial situation. Health experts worry that the paltry 22 percent rate of adults staying up-to-date on vaccines will erode further. And they fear that the roughly 25 million people without health insurance in the nation will be especially vulnerable to covid because they tend to be in poorer health and avoid medical care when sick.

Nicole Savant, a 33-year-old part-time paralegal and dog walker, lost her Medicaid benefits last year when her income rose. She wants the latest shot because she knows people who died of covid before the vaccines became available and because she faces a higher risk of severe disease being overweight.

She was floored when she was quoted $201.99 at an appointment to receive the vaccine at a St. Louis-area CVS. She wasn’t sure if she even had that much money in her bank account.

“I have so little money, and I have other needs as well, like monthly medications,” said Savant, who doubts she will get the vaccine if she has to pay out of pocket. “I would hope for the best, which I really don’t want to do.”

At least 34 million doses of last year’s vaccine were administered to adults, according to the Centers for Disease Control and Prevention. Of those, 1.5 million were funded through the Bridge Access Program, which was originally set to end this December, allowing vaccinations ahead of the usual winter wave.

But it expired ahead of schedule because Congress rescinded $6.1 billion in coronavirus emergency spending authority as part of a deal to avert a government shutdown. Congress also declined to fund the Biden administration’s proposal for a Vaccines for Adults program that could provide routine immunizations, including for the coronavirus, for free, similar to an existing Vaccines for Children program.

Private insurers, along with the Medicare and Medicaid government programs, are required to pay for coronavirus vaccines. The Bridge Access Program offered a backup option for people encountering insurance snags.

The CDC said it identified an additional $62 million to buy coronavirus vaccines targeting the latest variants for distribution through state and local health agencies — which local officials say is a sliver of the overall need. CDC spokeswoman Jasmine Reed said the partnership with state and local officials can provide shots to 1 million insured and underinsured Americans.

Raynard Washington, who leads the Mecklenburg County health department in North Carolina, said it’s difficult for financially strapped health agencies to tap their own funds for coronavirus vaccines. Under CDC contracts, health officials spend $78 a dose for the vaccine from the drug company Moderna and pay $100 for the version from Pfizer-BioNTech, compared with $15 to $20 for flu shots.

Washington, who also leads the Big Cities Health Coalition, an organization representing metropolitan health departments, said vaccine manufacturers should charge health departments less to help vaccinate more people without insurance.

“What’s at stake is we are reverting back to a system where a person’s financial ability to be able to pay will determine their ability to be healthy,” Washington said.